The Parag Parikh stable of funds attract a lot of attention because they are good story-tellers. In their Flexi-cap Fund, they are simultaneously placing concentrated bets on US and Indian equities, hedging, arbitraging, selling cover-calls, making cash allocation calls, and so on. And they talk about it a lot.

All this activity should surely result in superior performance?

We had written a couple of notes around this back in 2015 and 2019. Our concern revolved around return-attribution. When you are doing so many things, how do we know if you are actually good at any one of them?

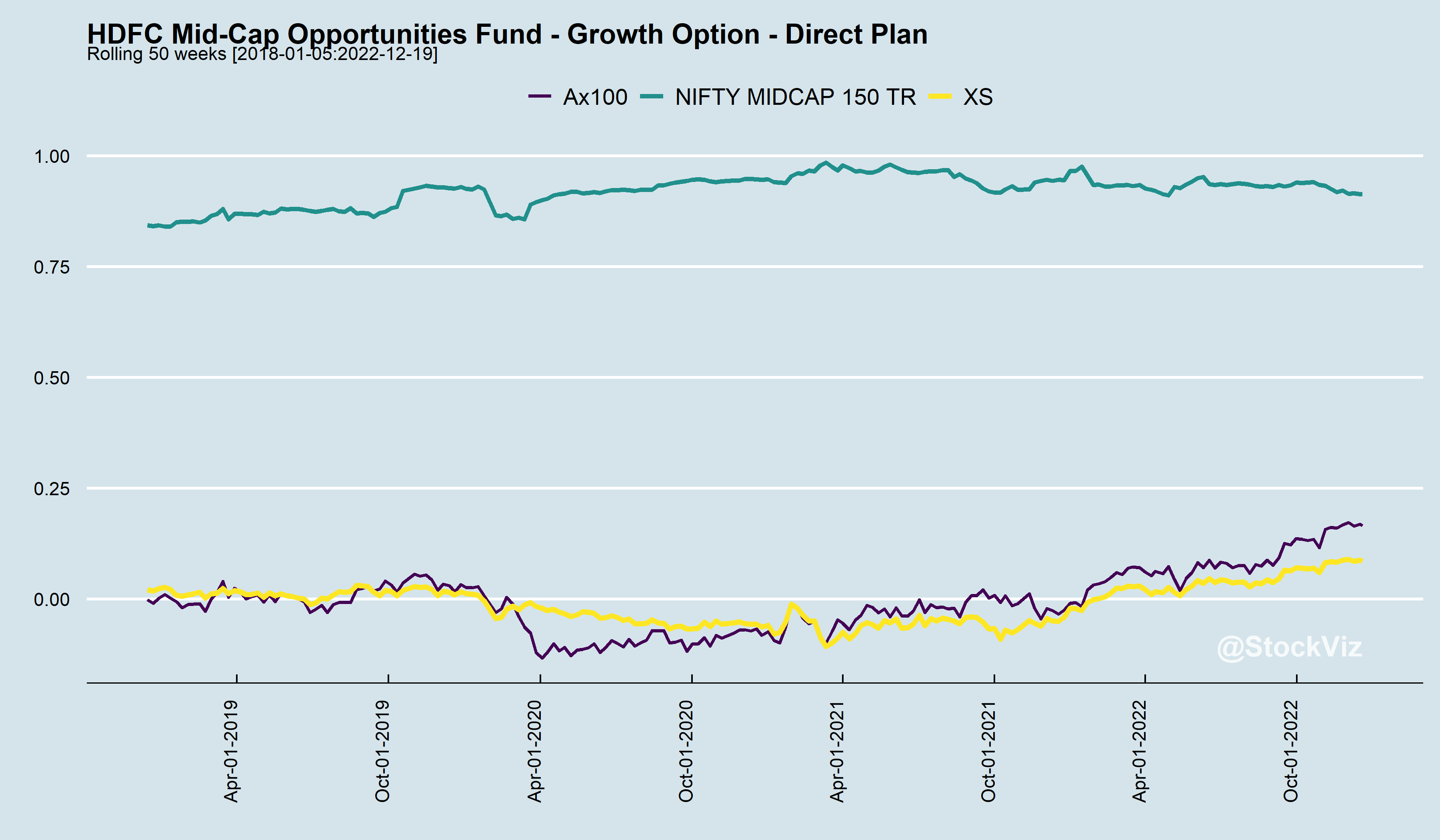

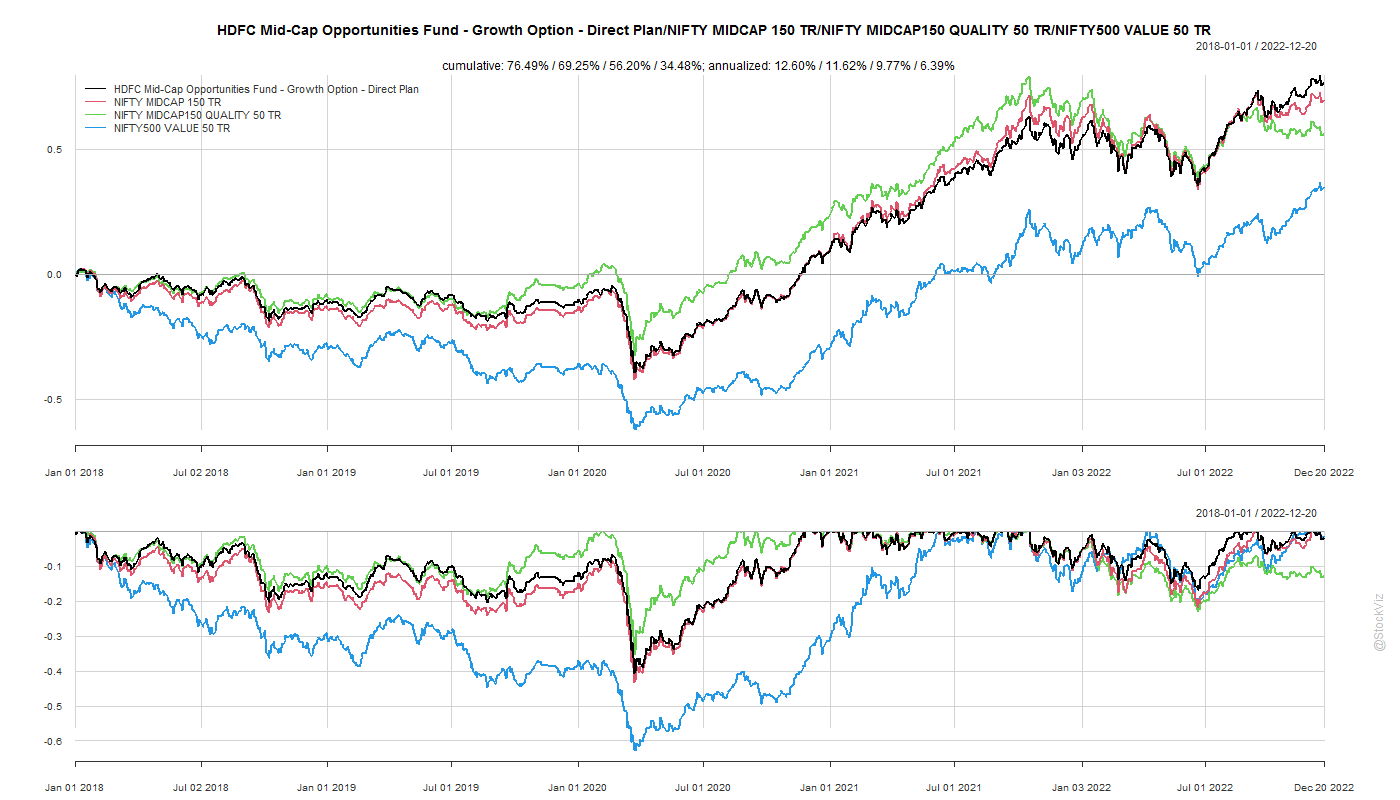

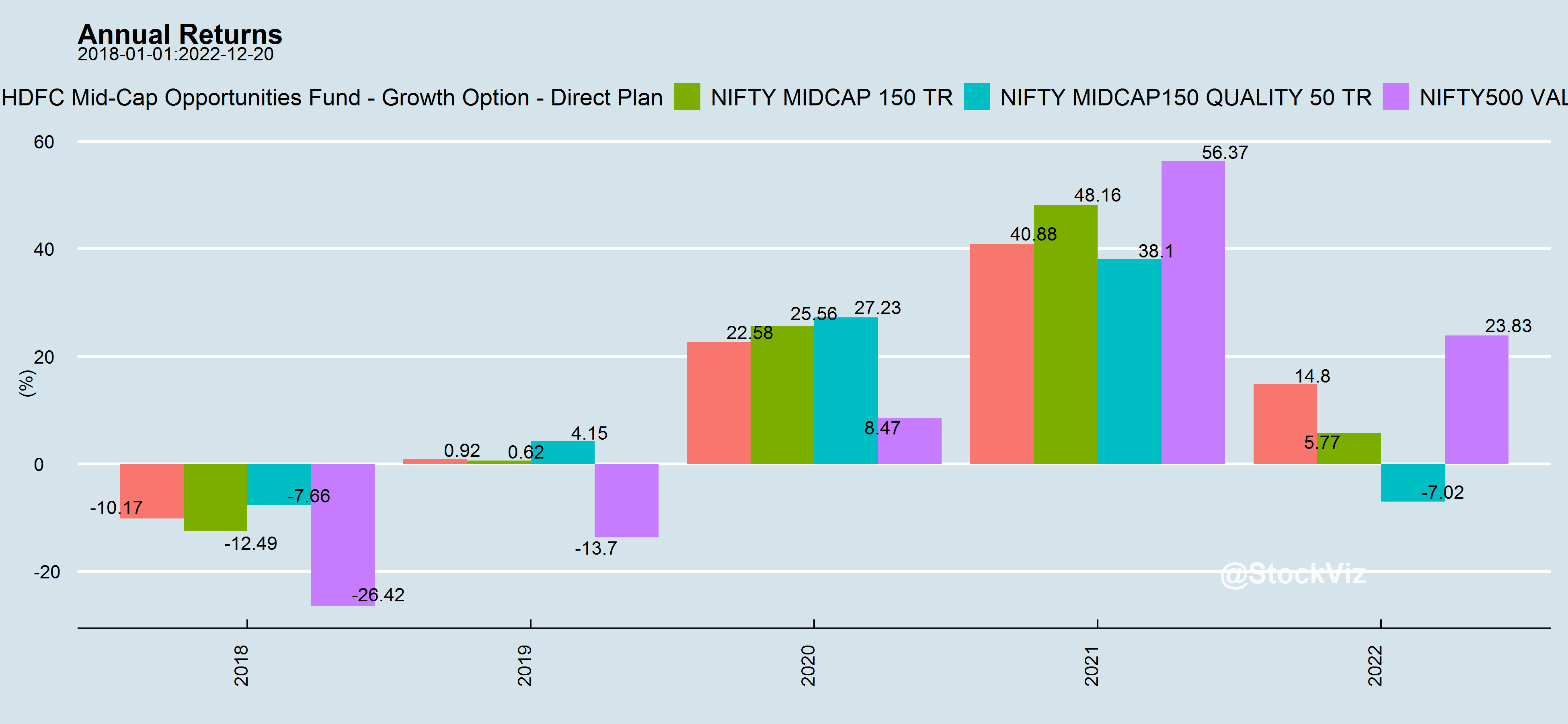

If you look at returns since the first note came out, they under-perform the MIDCAP 150 index.

Not that there weren’t years where they out-performed. However, given all that activity, is this all they could do?

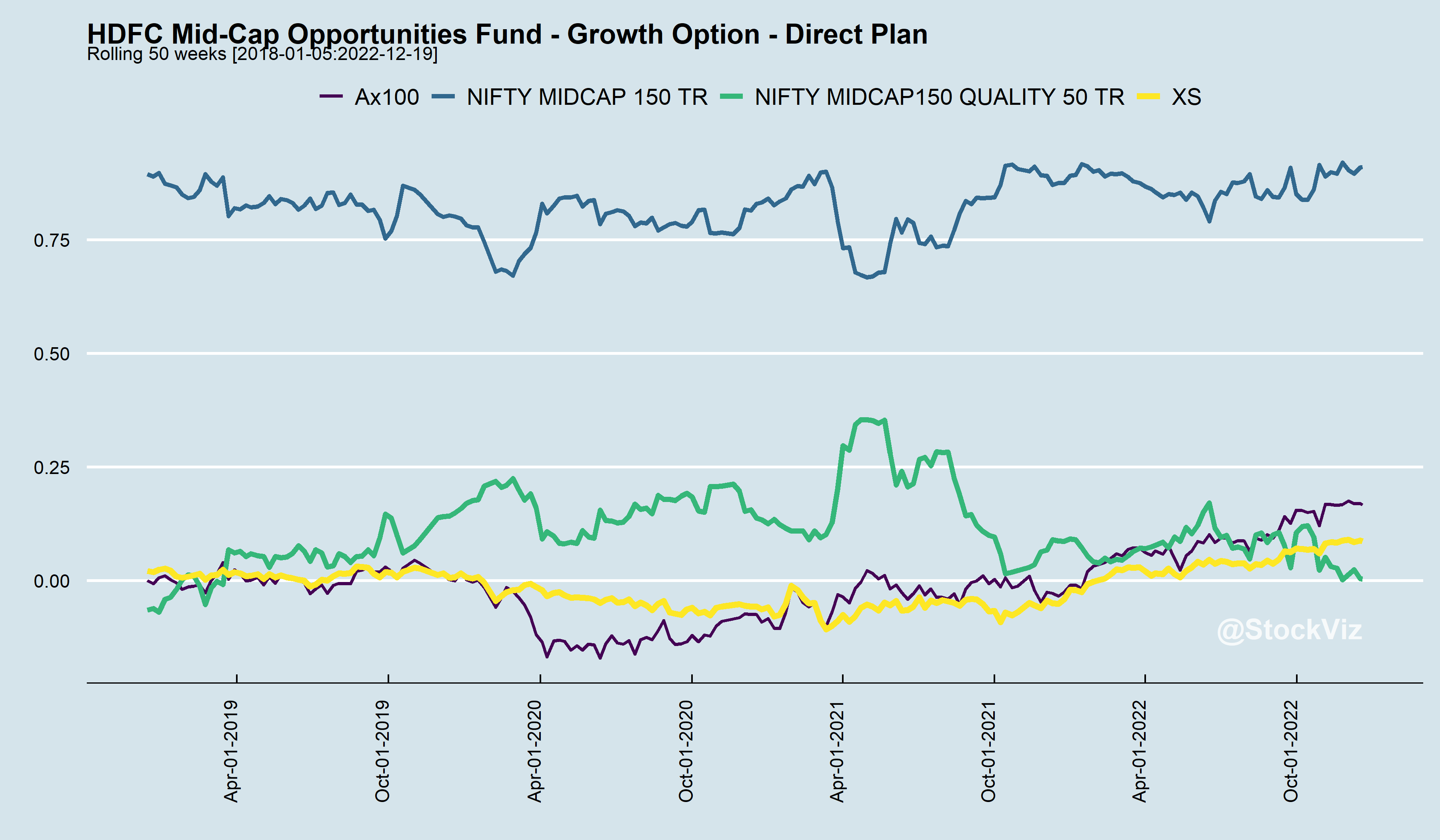

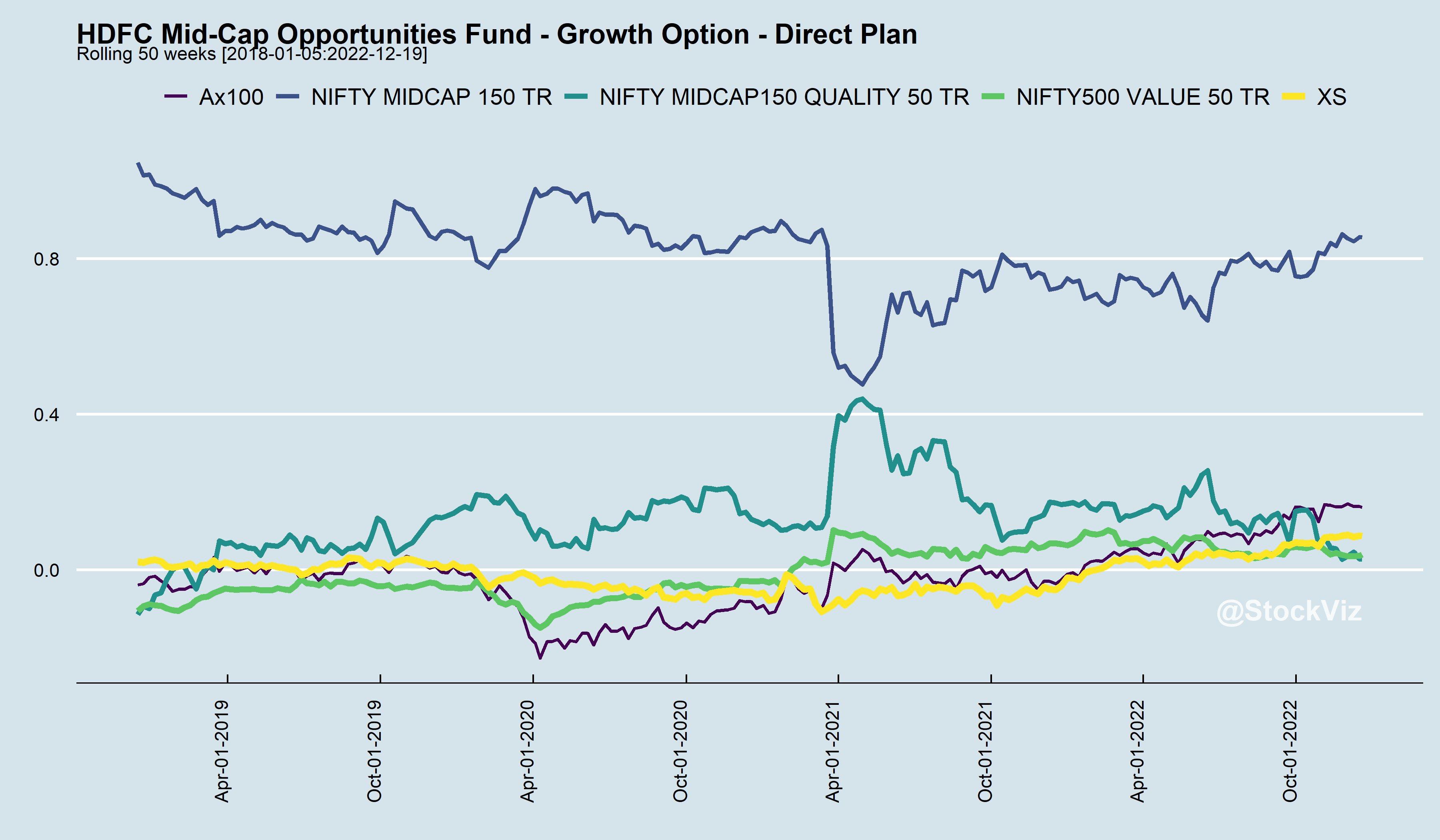

In our second note, we had mentioned that you could, technically, replace the fund with a midcap and S&P 500 index ETF in a 65-35 ratio. So, from that point on, if you were to construct such a portfolio, it would beat the fund as well.

It is not that their stock picks are bad. If you analyze the Indian equity portion of their portfolio over time, their stock picks, on average, has delivered 2% over the midcap index during the holding period.

And while digging through this, we noticed that there is alpha in keeping track of stocks that they have exited.

There is a decent skew in favor of entries but not as much as exits.

It is often said that exiting a position is tougher than entering it. In that sense, the fund managers have displayed good skill.

Tracking the current portfolio may not yield much. For example, if you look at positions held for more than 12 months, excess returns are distributed across the spectrum.

Our suggestion is that you can treat the fund as a research project for your own edification, but when it comes to deploying your own capital, you can stick with market-cap ETFs and index funds.

Code and charts on github.