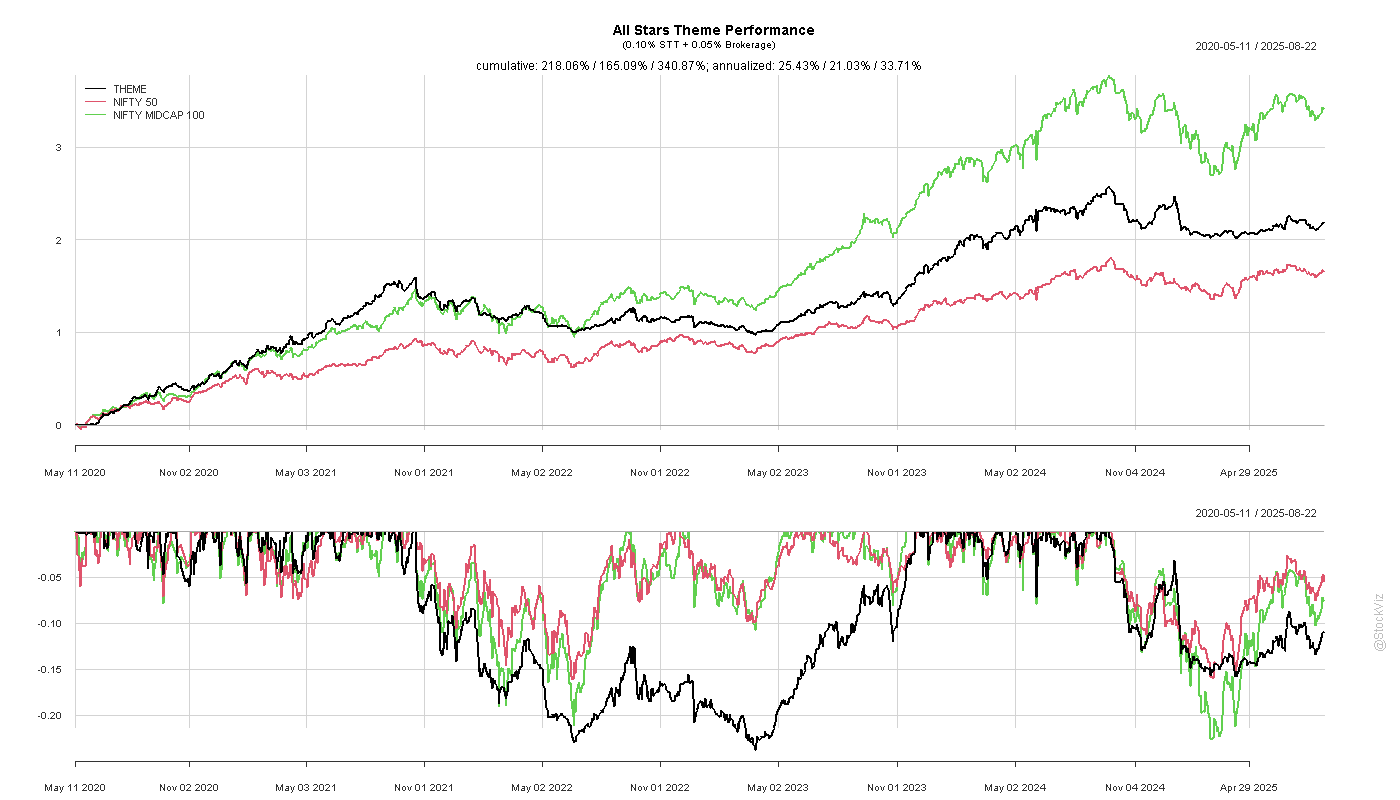

Previously, we ran Carver’s Strategy 9 with Crypto listed before 2019. However, there was a ton of new coins listed in the early 2020’s and incorporating them in the backtest meant taking a walk-forward approach to universe selection.

Here’s what we did: at the end of every month, we looked at all coins that had at least 500 days of history and had a positive Sharpe Ratio when Strategy 9 was applied to it. We then applied Strategy 9 on those coins for the following month. The technical details can be found here.

The results were underwhelming, to say the least.

There is some literature on using the Hurst Exponent to filter for trending instruments, so we tried that out as well. However, using Hurst didn’t really make a big difference.

Code and charts on github.