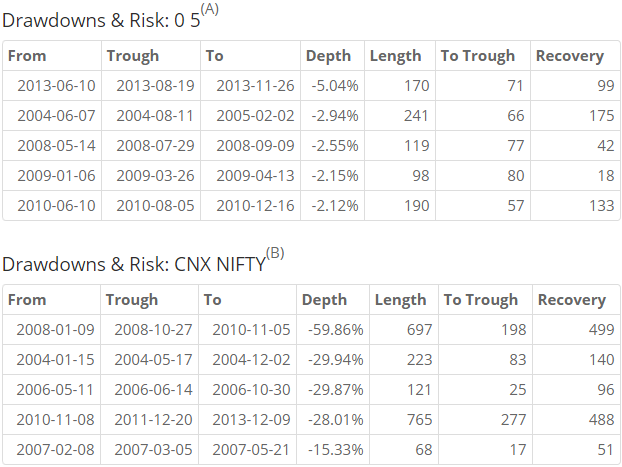

More is less

According to SEBI regulations, mutual funds should disclose their portfolios at the end of every month. Typically, by the 10th of every month, the previous month’s portfolio is made publicly available. Investors and analysts use these disclosures to guide their allocation strategies. But should they?

First, these disclosures are mere snapshots of an actively managed portfolio. A fund’s performance could have nothing to do with the portfolio disclosed at the end of the month. The portfolio hides trading gains (or losses) and this skews the correlation between NAV returns and portfolio returns.

Second, since the fund manager knows that investors will be scrutinizing the disclosures, he may engage in window-dressing. He might temporarily swap out securities that are perceived as “risky” by investors with “good-looking” alternatives.

Third, the source of returns may not be the visible portfolio. For example, if the fund holds hedges or has holdings in foreign stocks, then NAV returns could be driven by deltas or currency depreciation rather than the visible part of the portfolio.

Portfolio Trajectory

With the above caveats in mind, we present the ability to browse through historical portfolios through our FundCompare tool. We have uploaded portfolios of over 200 equity funds for the last two years and given you easy access to all of them.

Collecting this information was a painstaking process. Every fund has its own format of disclosing this information – some in excel sheets, some in pdfs, etc. And none of them give you the ticker, we had to use Natural Language Processing (NLP) techniques to map the names of every line-item to an NSE/BSE ticker. If you find any bugs or you want us to add a fund to our coverage, please mention them in the comments section of the FundCompare tool.