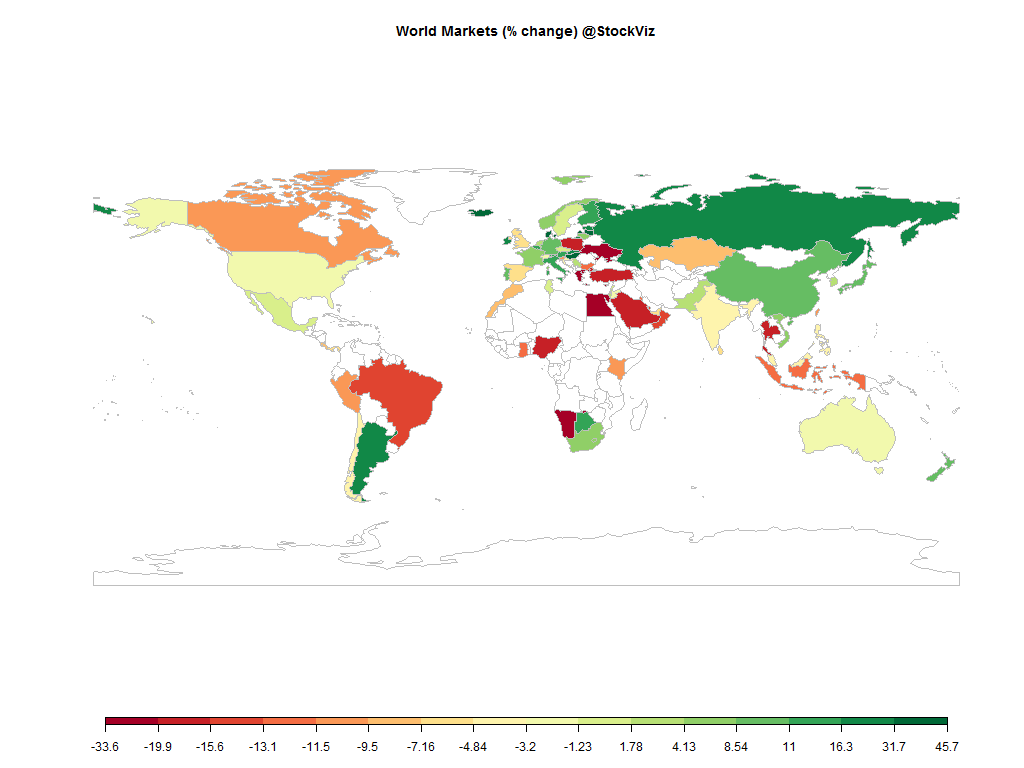

Equities

| MINTs | |

|---|---|

| JCI(IDN) | -12.13% |

| INMEX(MEX) | -1.18% |

| NGSEINDX(NGA) | -17.36% |

| XU030(TUR) | -17.64% |

| BRICS | |

|---|---|

| IBOV(BRA) | -13.31% |

| SHCOMP(CHN) | +9.41% |

| NIFTY(IND) | -4.06% |

| INDEXCF(RUS) | +26.12% |

| TOP40(ZAF) | +4.16% |

Commodities

| Energy | |

|---|---|

| Ethanol | -13.17% |

| Brent Crude Oil | -33.76% |

| Heating Oil | -39.27% |

| Natural Gas | -20.45% |

| RBOB Gasoline | -11.49% |

| WTI Crude Oil | -29.88% |

| Metals | |

|---|---|

| Silver 5000oz | -12.10% |

| Platinum | -26.40% |

| Gold 100oz | -10.86% |

| Copper | -25.00% |

| Palladium | -29.43% |

Currencies

| MINTs | |

|---|---|

| USDIDR(IDN) | +11.64% |

| USDMXN(MEX) | +17.00% |

| USDNGN(NGA) | +8.49% |

| USDTRY(TUR) | +24.88% |

| BRICS | |

|---|---|

| USDBRL(BRA) | +49.03% |

| USDCNY(CHN) | +4.64% |

| USDINR(IND) | +4.93% |

| USDRUB(RUS) | +24.64% |

| USDZAR(ZAF) | +34.63% |

| Agricultural | |

|---|---|

| Lean Hogs | -26.84% |

| Sugar #11 | +4.32% |

| Cattle | -18.04% |

| Coffee (Arabica) | -25.53% |

| Cotton | +4.21% |

| Lumber | -21.95% |

| White Sugar | +7.86% |

| Cocoa | +14.74% |

| Corn | -10.56% |

| Feeder Cattle | -23.82% |

| Orange Juice | -0.04% |

| Soybeans | -14.65% |

| Wheat | -20.25% |

| Coffee (Robusta) | -21.25% |

| Soybean Meal | -27.19% |

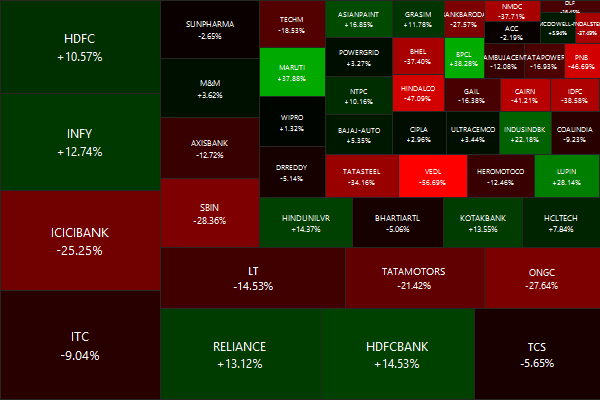

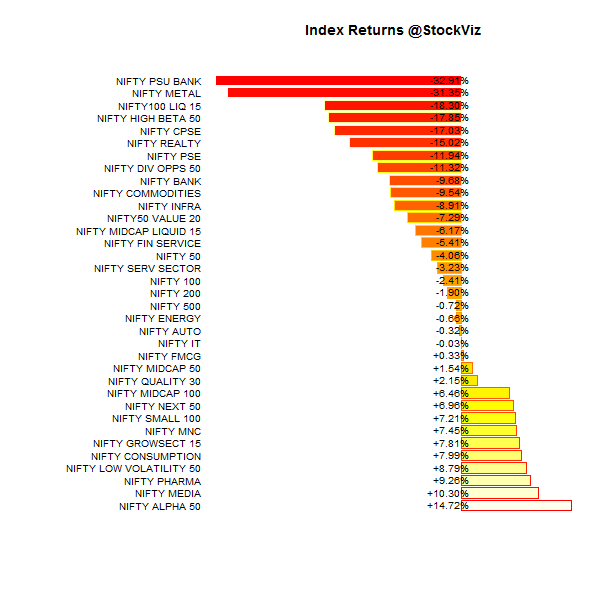

Nifty Heatmap

Index Returns

Market Cap Decile Performance

| Decile | Mkt. Cap. | Adv/Decl |

|---|---|---|

| 1 (micro) | +83.07% | 95/39 |

| 2 | +64.59% | 104/29 |

| 3 | +40.56% | 91/42 |

| 4 | +31.75% | 80/53 |

| 5 | +28.26% | 82/51 |

| 6 | +27.95% | 85/48 |

| 7 | +14.75% | 76/57 |

| 8 | +19.85% | 75/58 |

| 9 | +5.53% | 68/65 |

| 10 (mega) | +0.91% | 68/66 |

It was the year of the small-caps – vastly out-performing the NIFTY 50.

Top Winners and Losers

Commodities and public sector bank stocks got pummeled…

ETF Performance

| JUNIORBEES | +7.87% |

| NIFTYBEES | -4.26% |

| GOLDBEES | -7.50% |

| INFRABEES | -9.11% |

| BANKBEES | -10.32% |

| CPSEETF | -14.07% |

| PSUBNKBEES | -31.65% |

Broad-based indices had very little to offer…

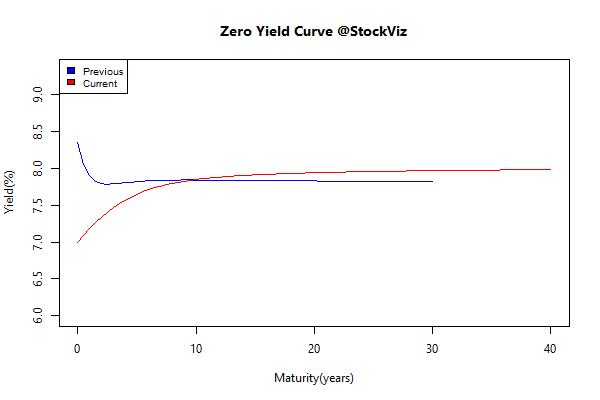

Yield Curve

Bond Indices

| Sub Index | Change in YTM | Total Return(%) |

|---|---|---|

| 0 5 | -0.50 | +9.21% |

| 5 10 | -0.14 | +8.78% |

| 10 15 | +0.01 | +7.83% |

| 15 20 | +0.09 | +7.02% |

| 20 30 | +0.13 | +6.10% |

On a total return basis, the long-bonds barely kept up with inflation.

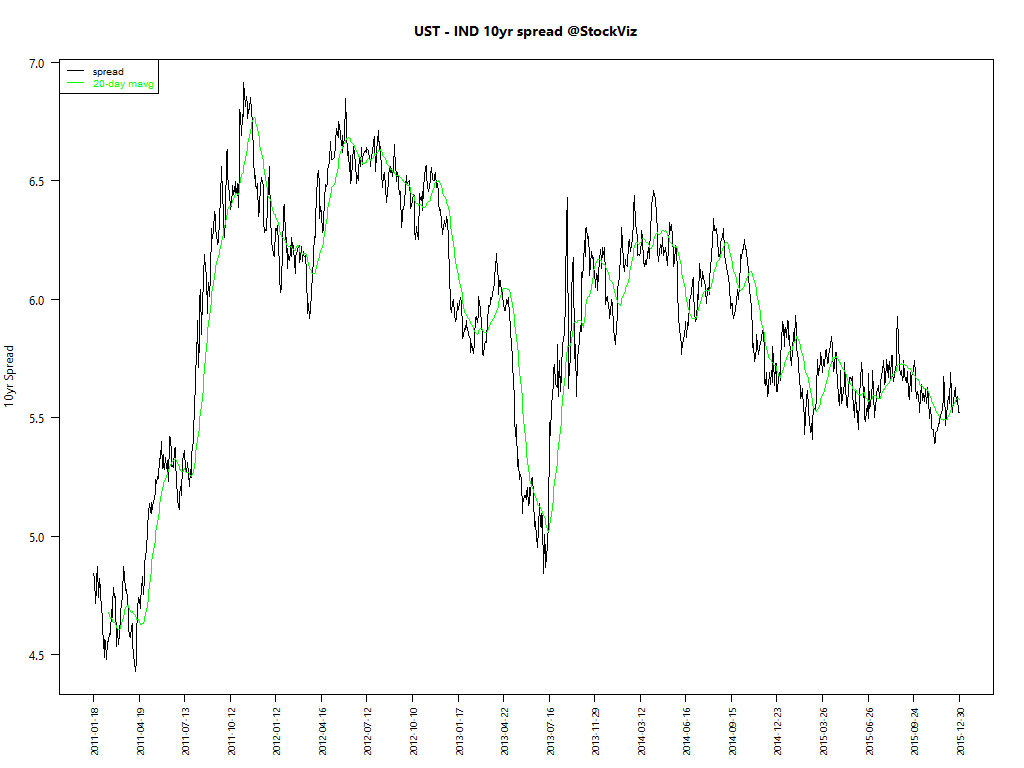

Spread between US Treasuries and Indian Gilts

Investment Theme Performance

| Momentum | +45.89% |

| Financial Strength Value | +43.02% |

| Quality to Price | +35.28% |

| Magic Formula | +16.15% |

| Low Volatility | +6.41% |

| Enterprise Yield | +6.06% |

| Balance Sheet Strength | +4.59% |

| Tactical CNX 100 | -1.10% |

| High Beta | -30.34% |

Most investment strategies came out ahead…

Equity Mutual Funds

Bond Mutual Funds

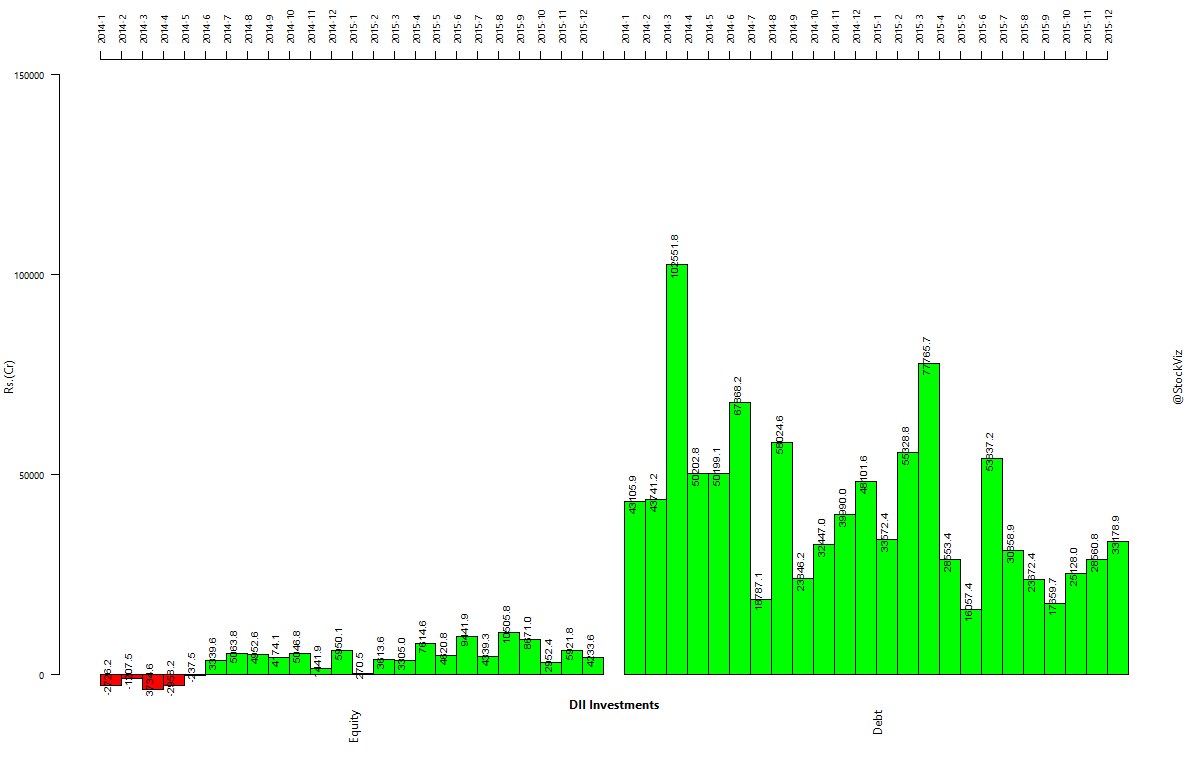

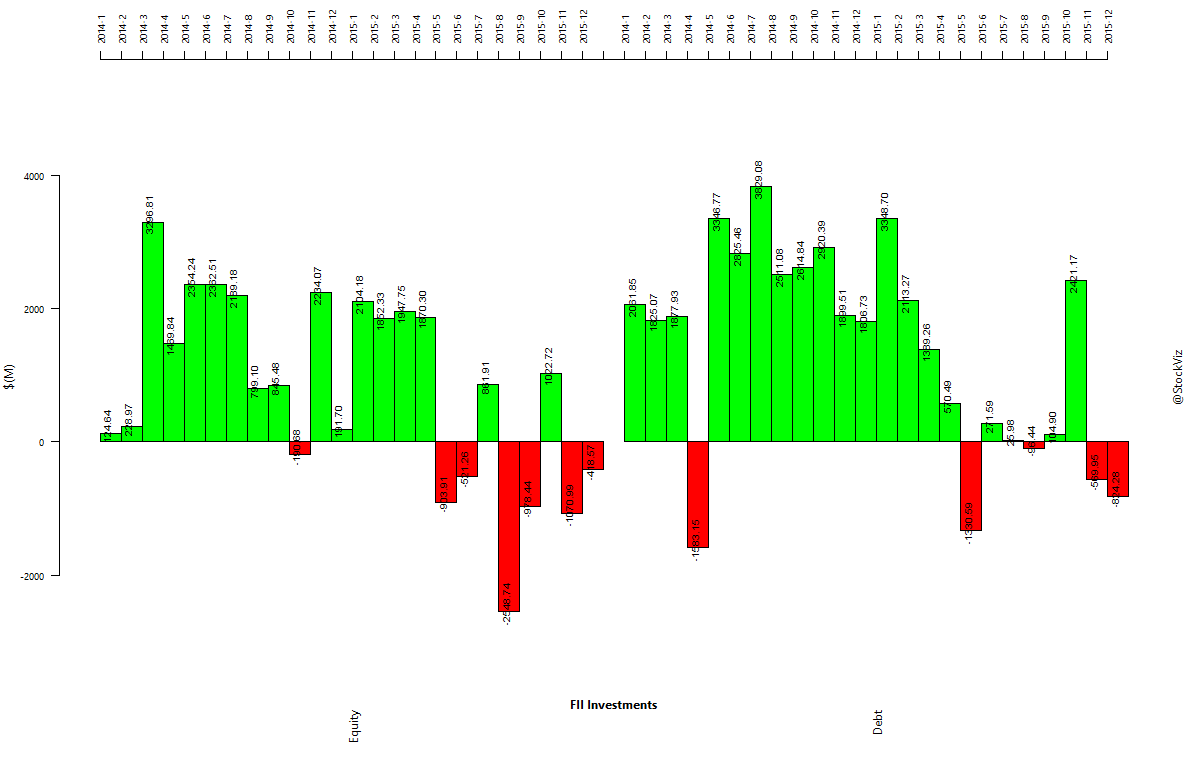

Institutional fund flows

Commentary

It was a year that saw record inflows of retail money into mutual funds and record outflow of foreign investors out of Indian markets. There were taper tantrums, Greece, GST #fail and so many worries. But the systematic and patient investor was rewarded for keeping a cool head.