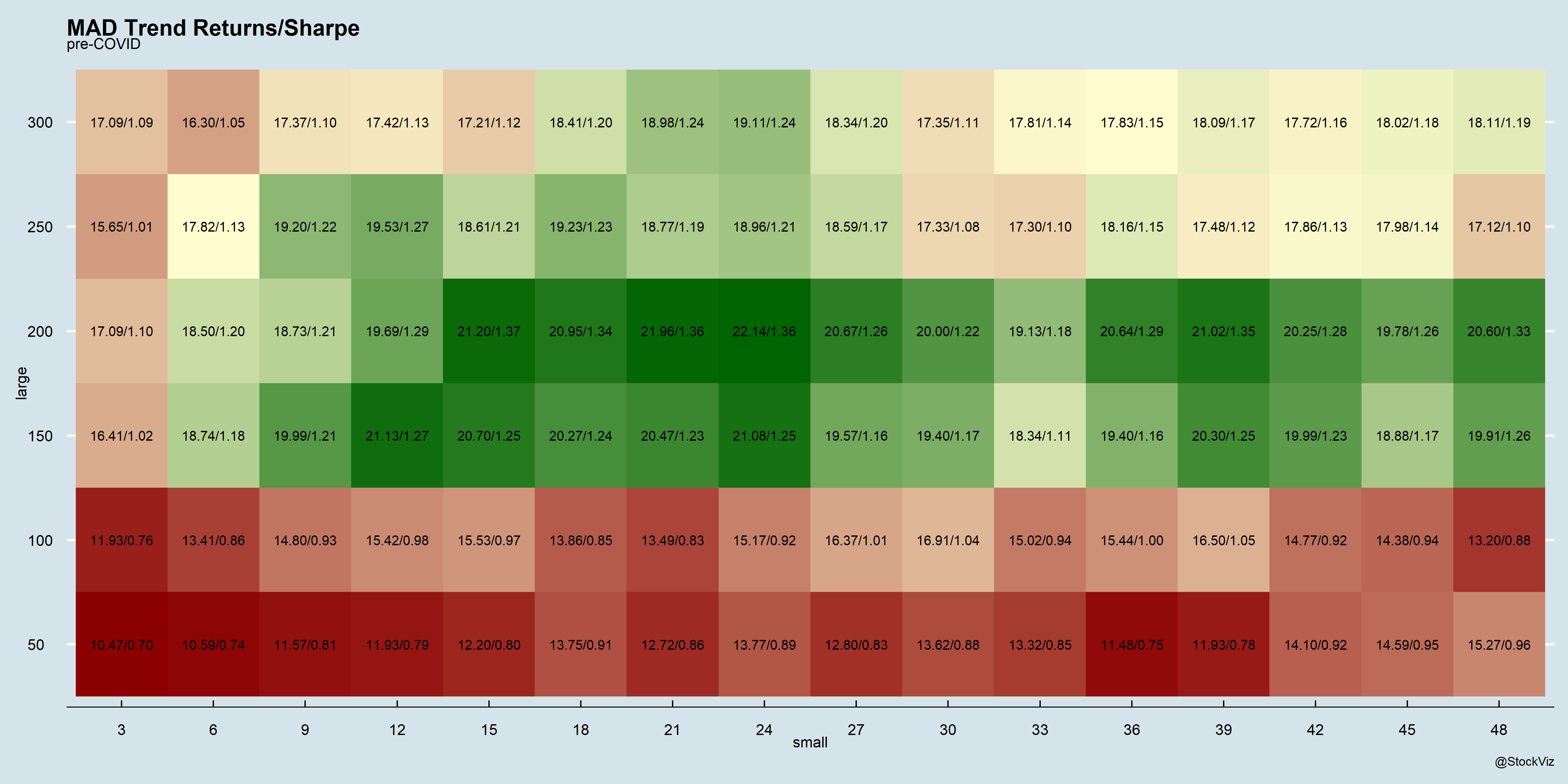

Our previous posts introduced portfolios based on Moving Average Distance (Part 1, Part 2). To answer questions regarding the stability of the moving average lookbacks, we ran a rolling window, picked the “best” MA lookbacks and walked the portfolio forward by a month. We expanded the window through 12 to 60 months in 12 month increments.

Turns out, most of them fall within the 20/200 region.

The data-mined parameters create portfolios that perform on par with the 21/200 used in the paper. While we are always skeptical about magical parameters that make the research work, at least in this case, the magic is not too far fetched.

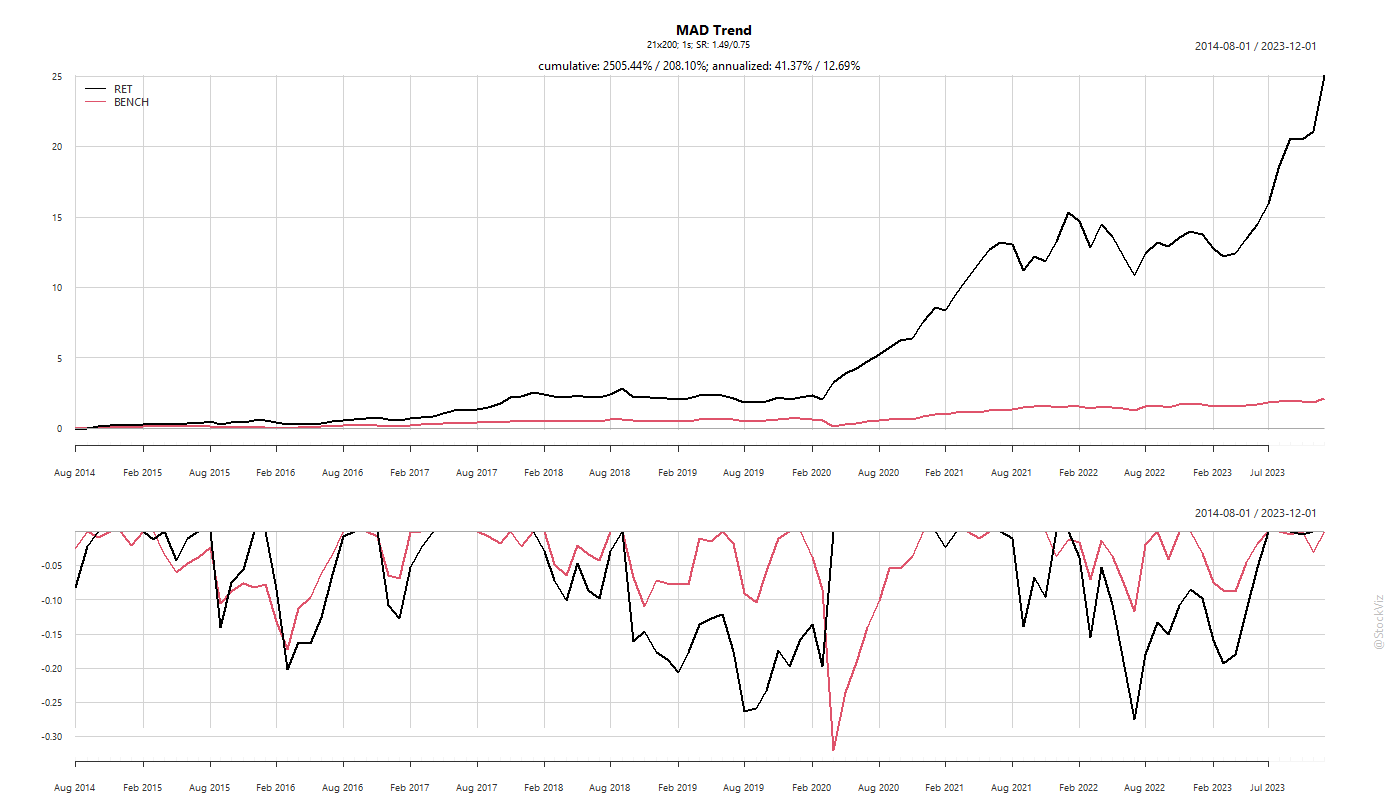

You can follow along the live version of the original strategy here: MAD 21/200