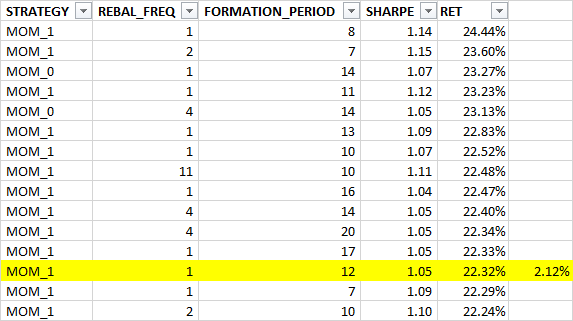

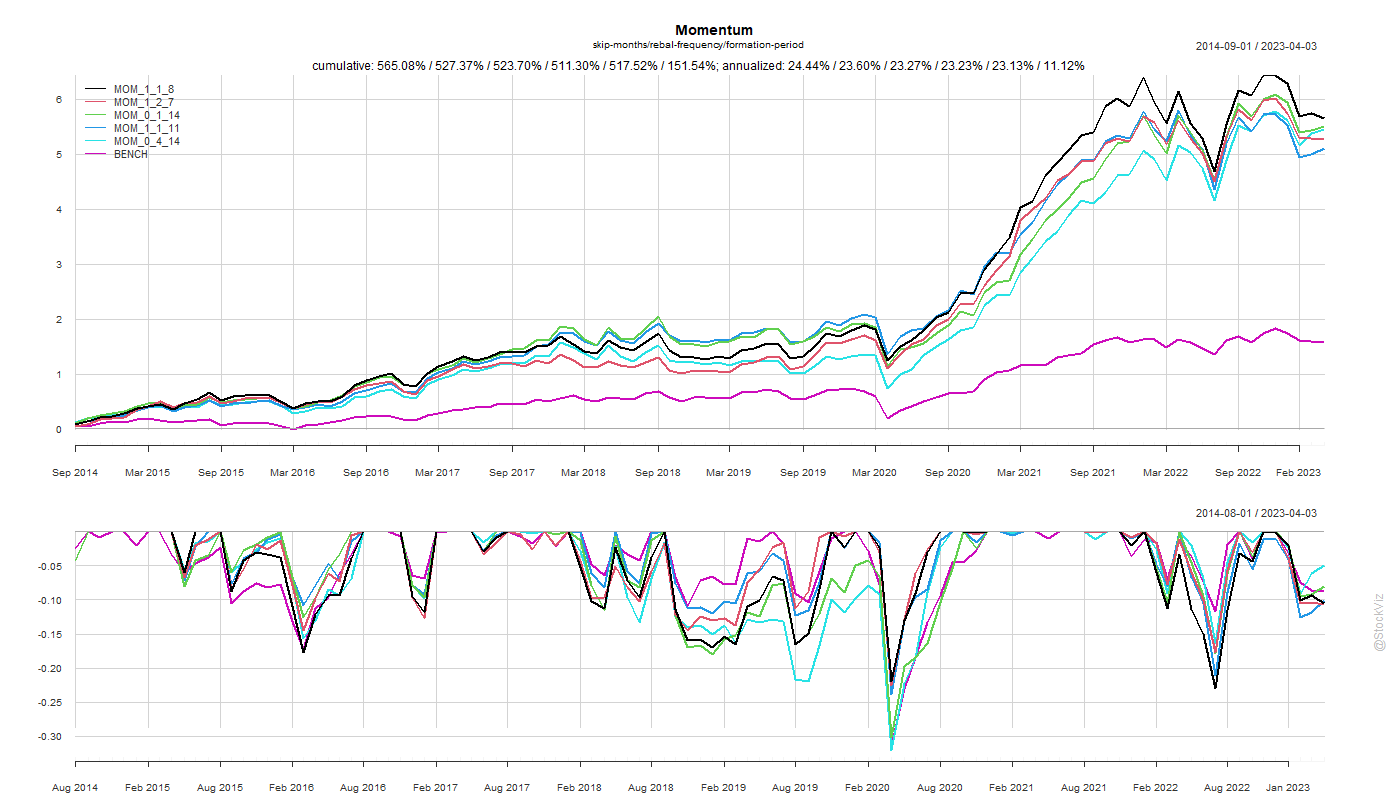

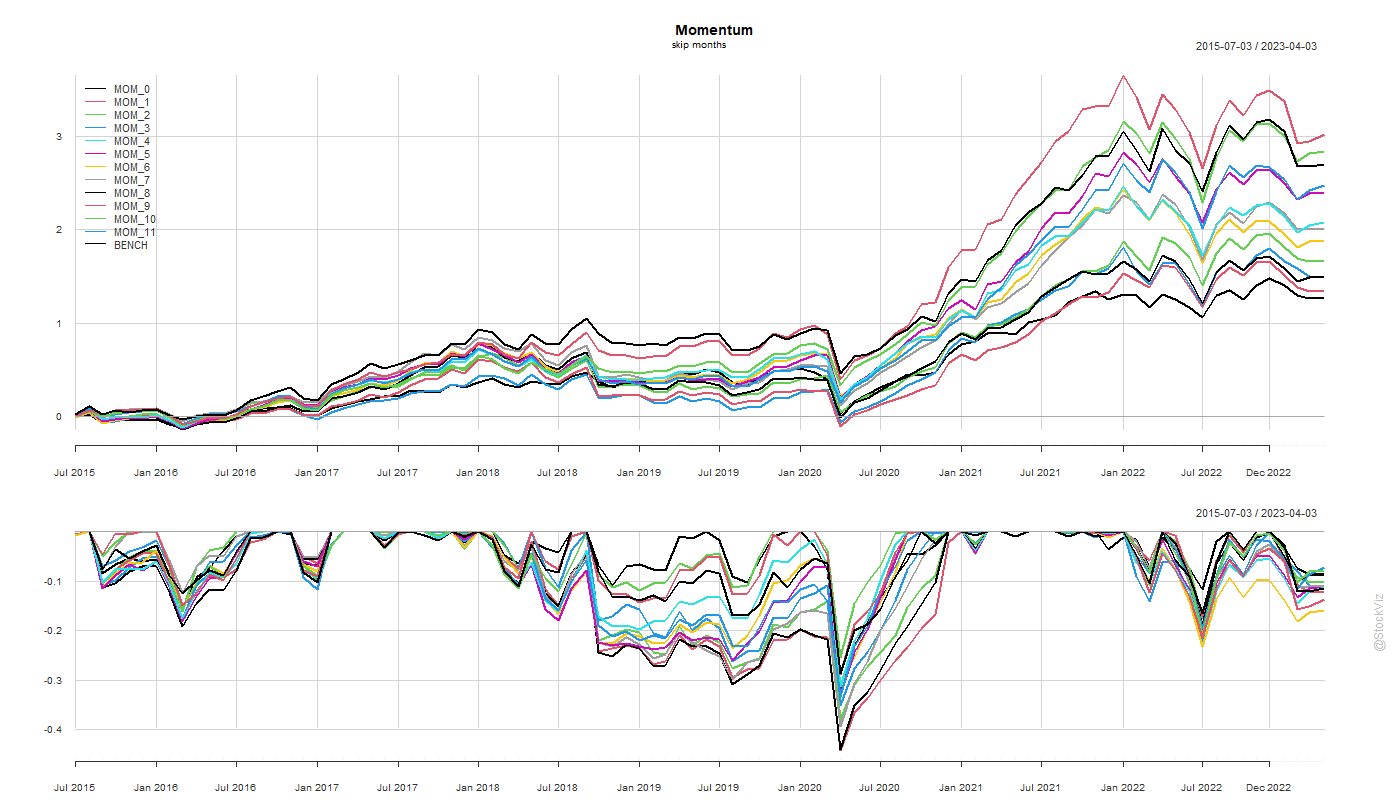

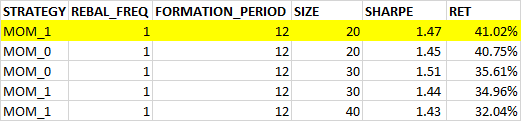

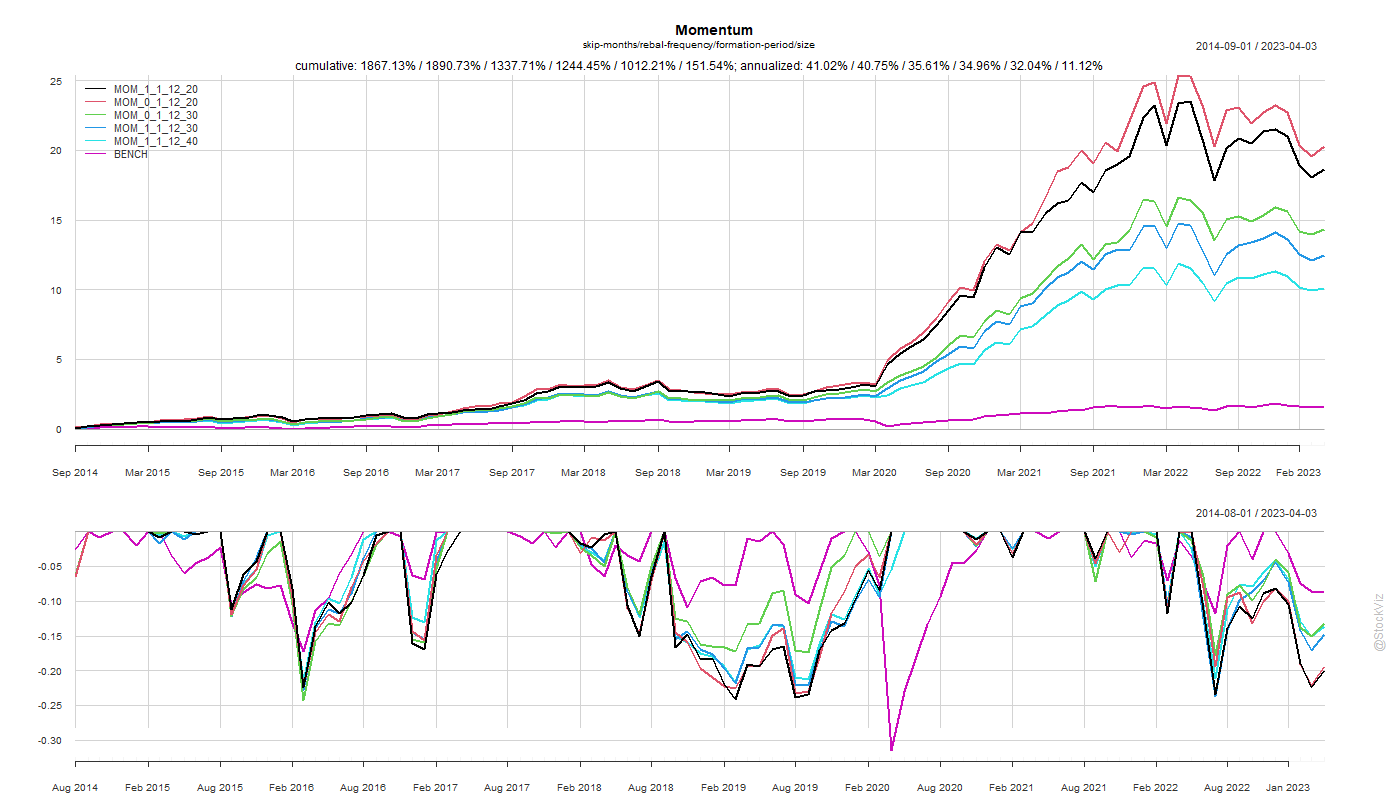

Previously, we looked at skip-months, rebalance frequencies and formation periods for momentum portfolios. A 1-month skip & monthly rebalance turned out to be ideal. However, the most popular 12-month formation period is “magic” – not a terrible choice but not super scientific either. The only thing left to toggle is the portfolio size.

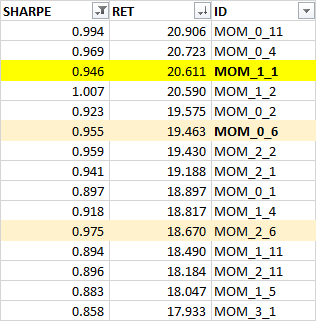

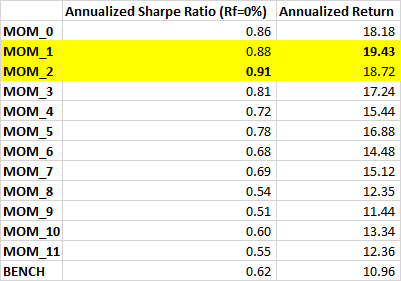

A 20-stock momentum portfolio seems to be the ideal config.

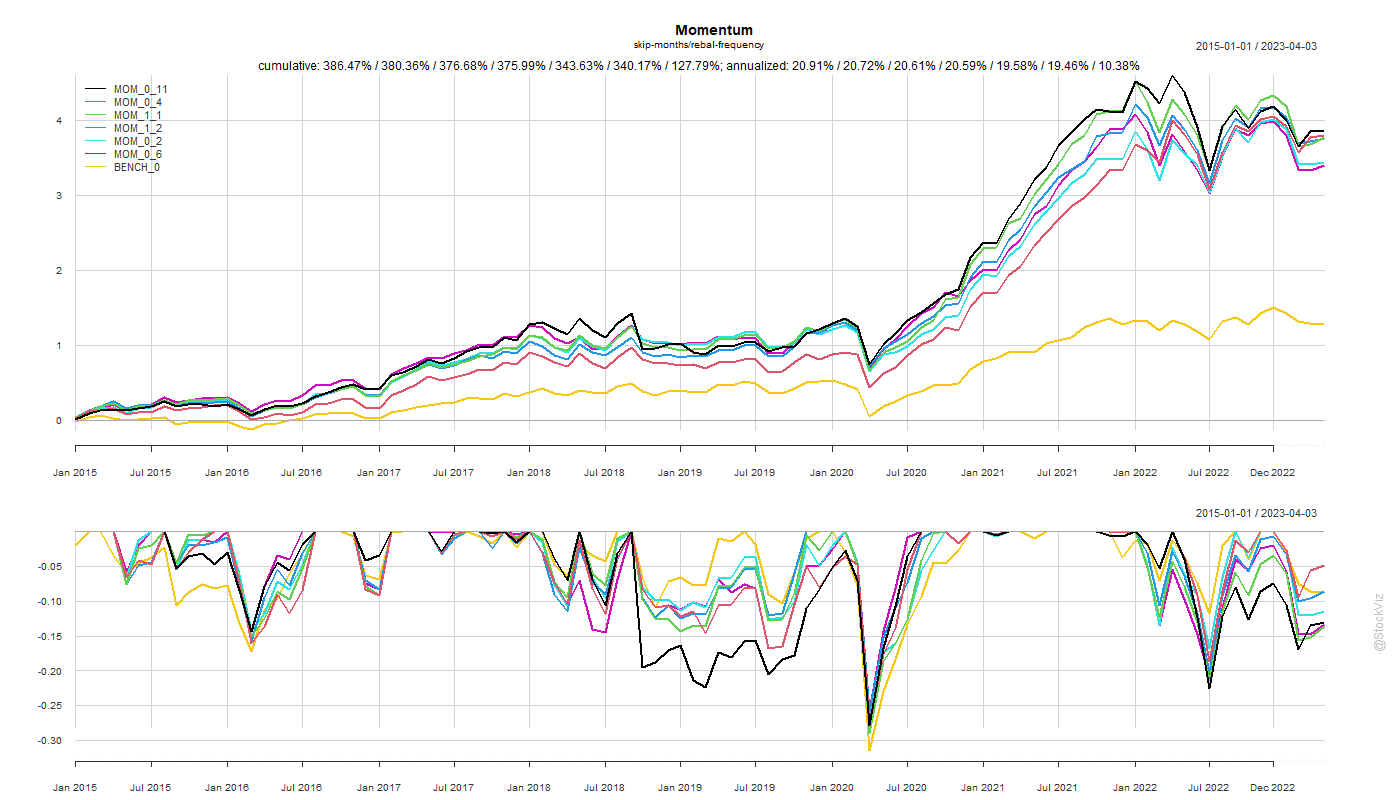

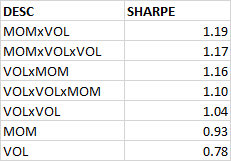

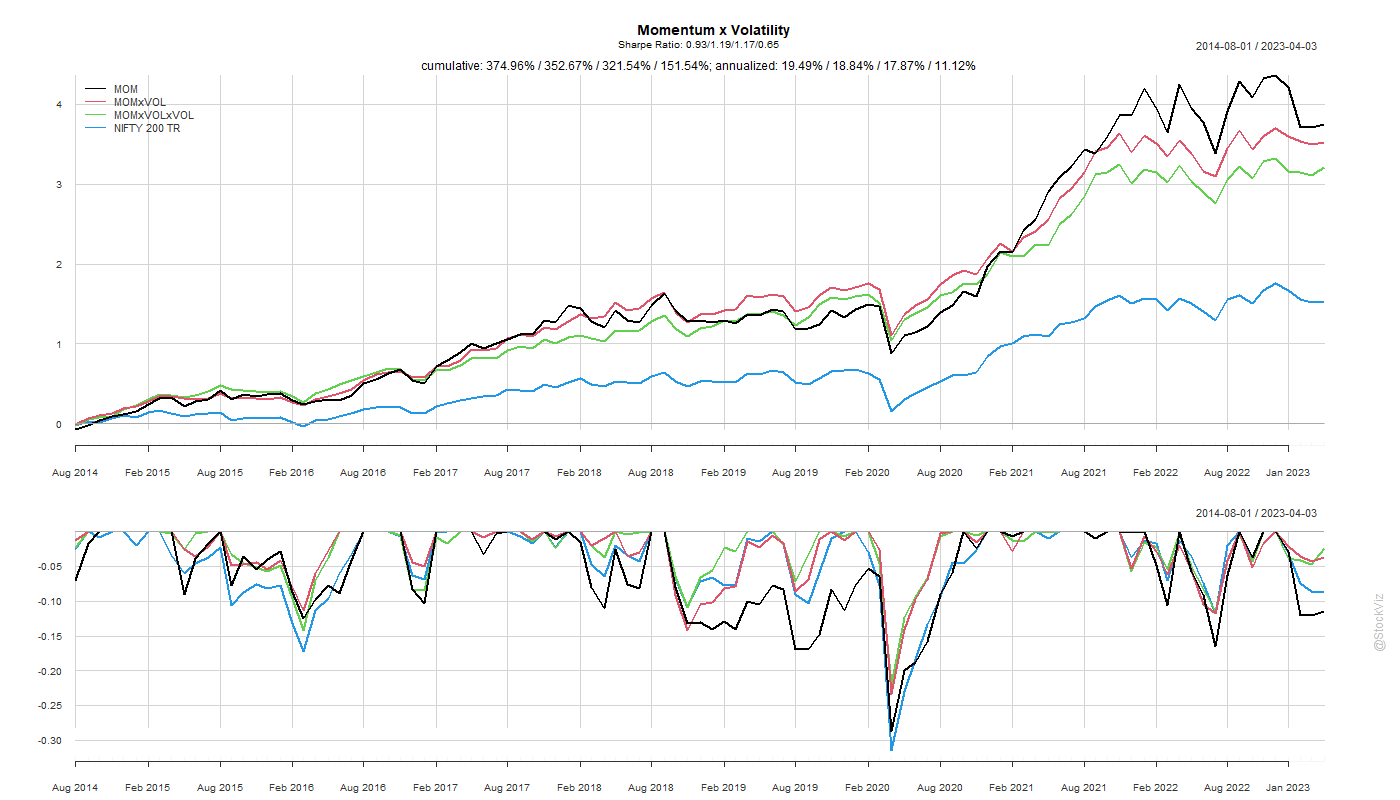

This is pretty much the standard direct-equity momentum portfolio: 12-month formation, 1-month skip, 20-stocks with a monthly rebalance.

Code and chart on github.