Popular indices, like NIFTY 50 & MIDCAP 150, are useful if you are benchmarking long-only portfolios. However, if you have a long-short portfolio, then you need a long-short benchmark.

When Are Contrarian Profits Due To Stock Market Overreaction? (Lo, MacKinlay, 1990) describes a naïve portfolio construction process that is fit for purpose.

For momentum, portfolio weights are in proportion of excess returns over an equal-weighted index and for mean-reversion, they are the inverse.

For example, if you subtract the returns of each of the components of the NIFTY 50 index with the returns of NIFTY 50 EQUAL-WEIGHT index and divide by 50, you end up with the portfolio weights for the next day. Each look-back period used to calculate returns will produce a different set of weights (and a different synthetic index.)

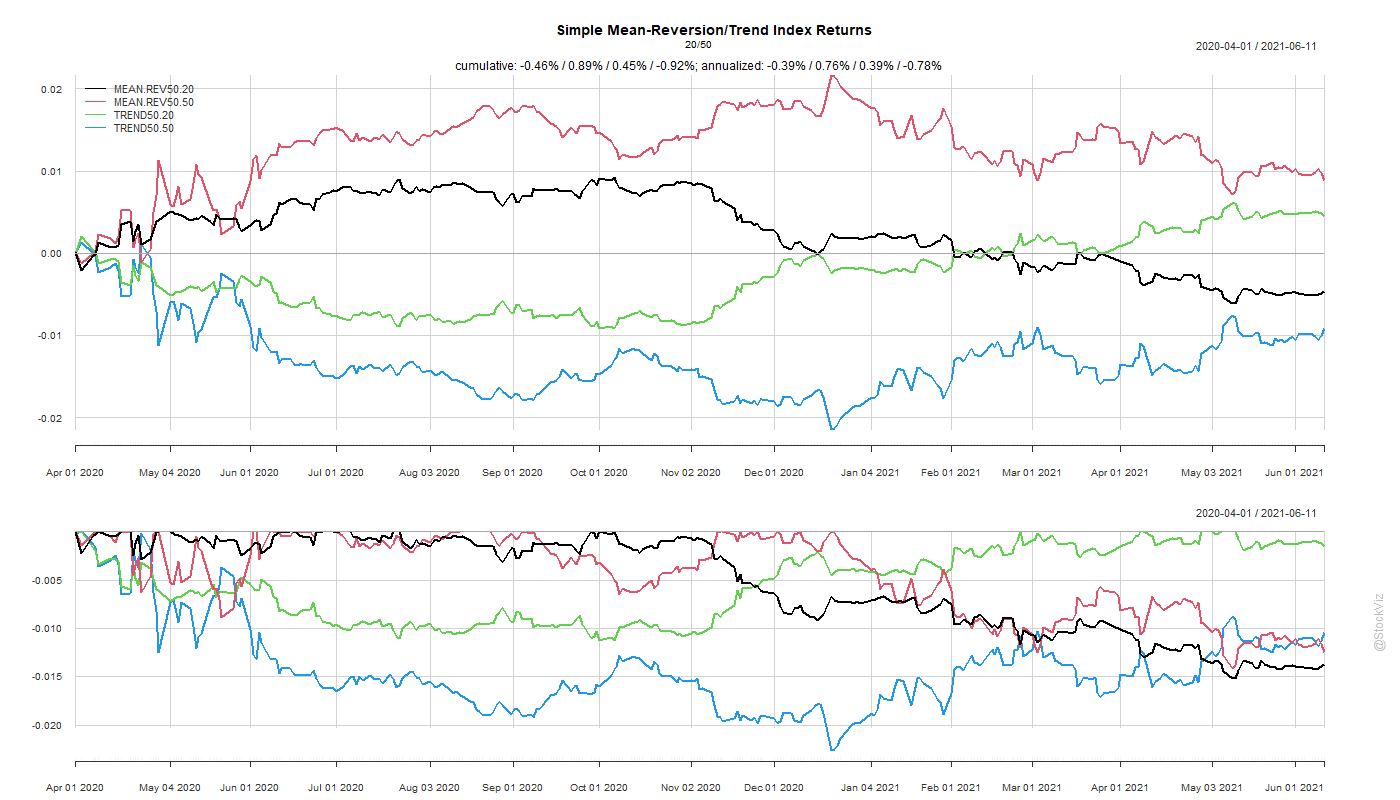

As impractical as constructing such a portfolio may seem, they are useful as a benchmark for long-short mean-reversion/momentum portfolios. Here are index returns since April 2020 with 20- and 50-day look-backs.

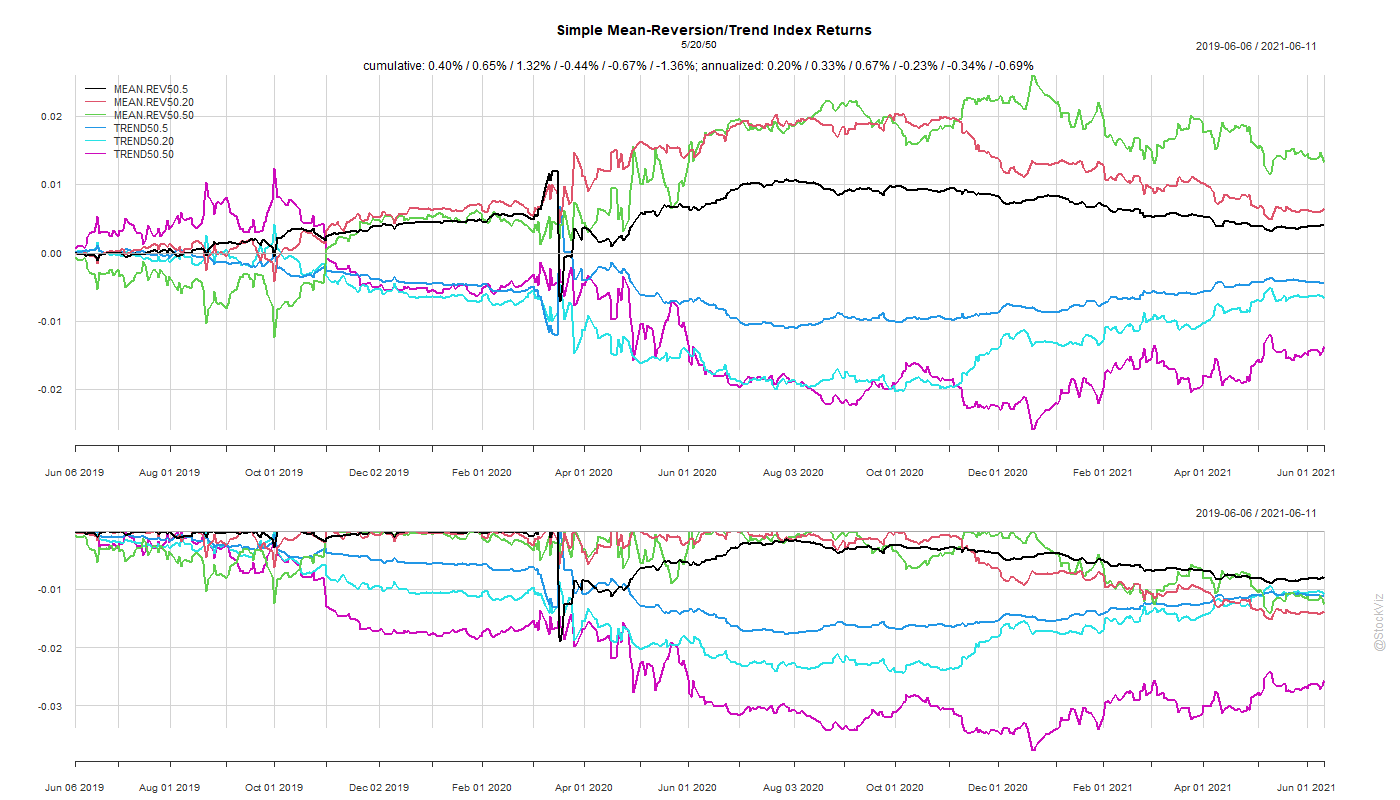

This is especially interesting if you are looking at market dislocations and subsequent recoveries. Here are indices since June 2019 with 5-, 20- and 50-day look-backs.

Counter-intuitively, naïve mean-reverting long-short seems to out-perform momentum.

In investing, we are always trying to find the relationship between two entities. For example, to hedge a long portfolio, we typically calculate the “beta” with respect to an index and use that to go short the index. Here, the biggest assumption is that the relationship is linear (or at least, piecewise linear.)

However, relationships in finance are typically non-linear. Using the math behind calculating entropy is one way to overcome the “beta” problem.

Introduction

From Wikipedia: Transfer entropy is a non-parametric statistic measuring the amount of directed (time-asymmetric) transfer of information between two random processes.

It tries to answer a simple question: what the effect of one entity over another, given a lag?

From StackExchange: TE(X↦Y)=0.624 means that the history of the X process has 0.624 bits of additional information for predicting the next value of Y. (i.e., it provides information about the future of Y, in addition to what we know from the history of Y). Since it is non-zero, you can conclude that X influences Y in some way.

Quick Look

Luckily, both R and python have libraries that help calculate transfer entropies between two variables.

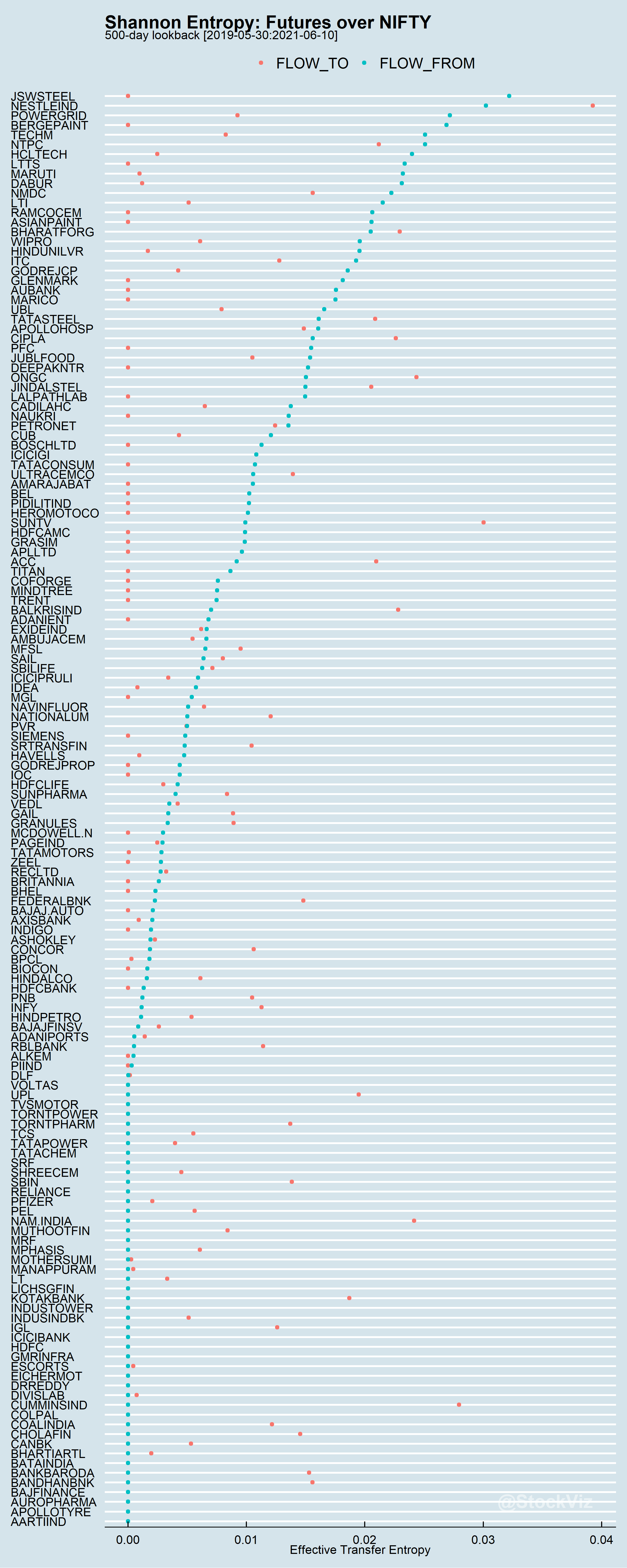

Here’s the TE between Stock Futures and the NIFTY with a 500 day lookback and a single-day lag. FLOW_TO is a measure of information flow from the stock to the index and FLOW_FROM is the opposite direction.

Next Steps

This has interesting applications in portfolio risk management. Instead of calculating beta and hoping for the best, we could use TE to get a better understanding of how the individual constituents are affected by the index and hedge only those that have large values.

Most of us have learnt how to calculate the distance between 2 points on a plane in high school. The simplest one is called the Euclidean Distance – a pretty basic application of the Pythagorean Theorem. The concept can be extended to calculate the distance between to vectors. This is where it gets interesting.

Suppose you want to match a price series with another, ranking a rolling window by its Euclidean Distance is the fastest and simplest way of pattern matching.

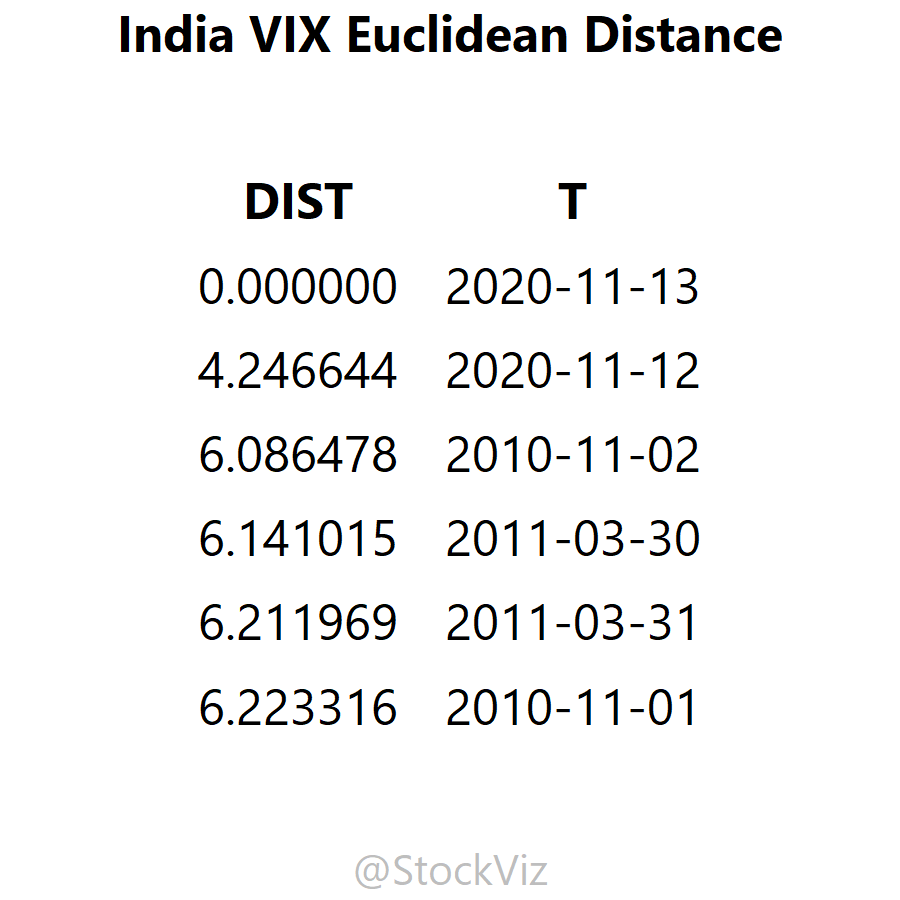

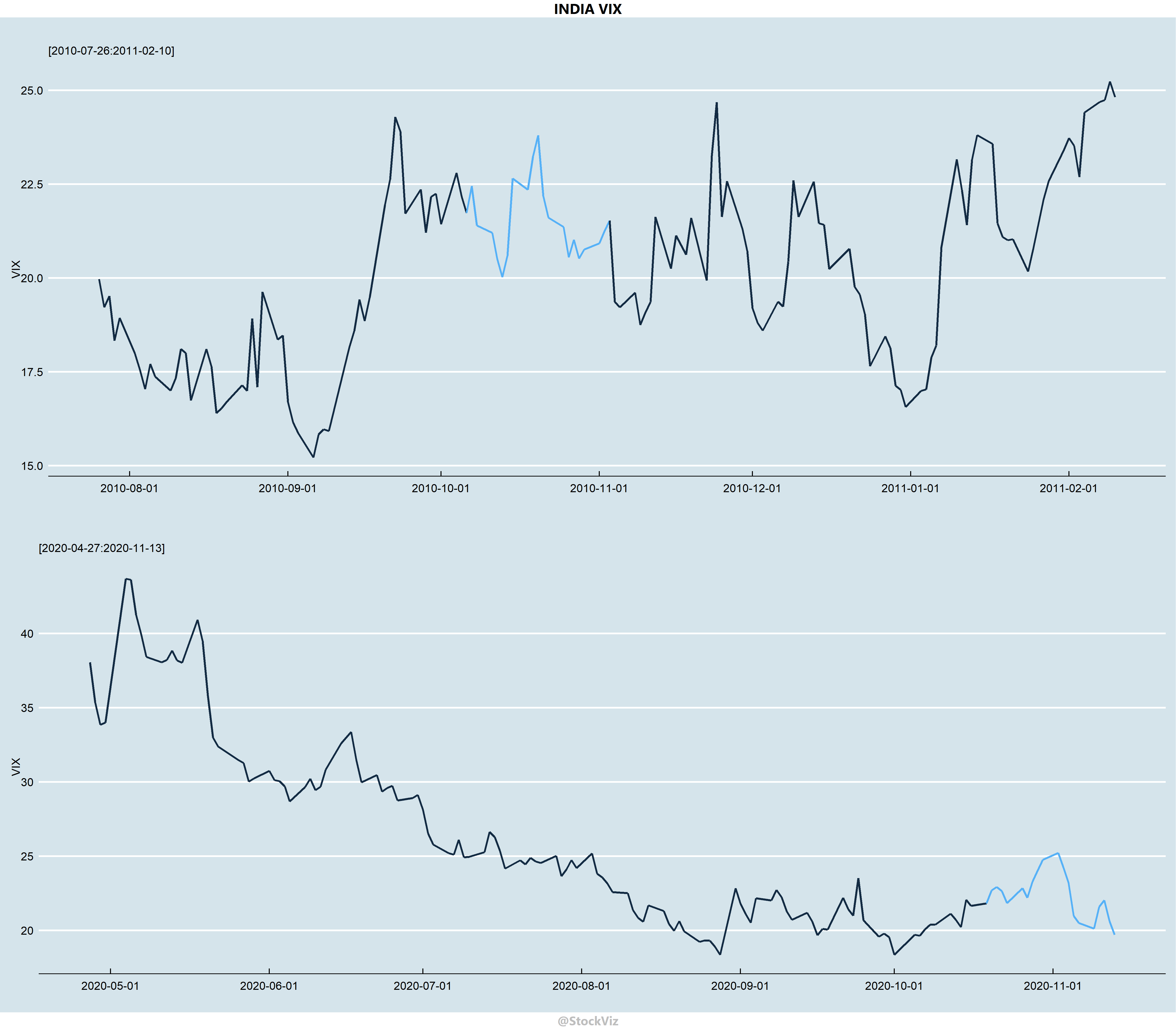

For example, take the most recent 20-day VIX time-series and “match” it with a rolling window of historical 20-day VIX segments and sort it by its Euclidean Distance (ED.)

Here, the ED has dug up a segment from November-2010 as one of the top 5 matches. Take a closer look:

While not a perfect match, it “sort of” comes close.

Sometimes, a simple tool is good enough to get you 80% of the way. This is one of them.

Can’t decide between quality, low-volatility, high-alpha? Why not buy all of them?

Our previous post discussed how you can use the historical performance of different factors to avoid falling into a factor-trap. However, can factor investing be further simplified?

The NSE Strategy Indices

The NSE has published a whole library of factor indices. Some of them are pure factors – like quality, low-volatility, etc – and some are hybrids – like alpha-quality-low-volatility (sort of like a shampoo-conditioner-face-wash 3-in-1.) You can explore their website if your curious.

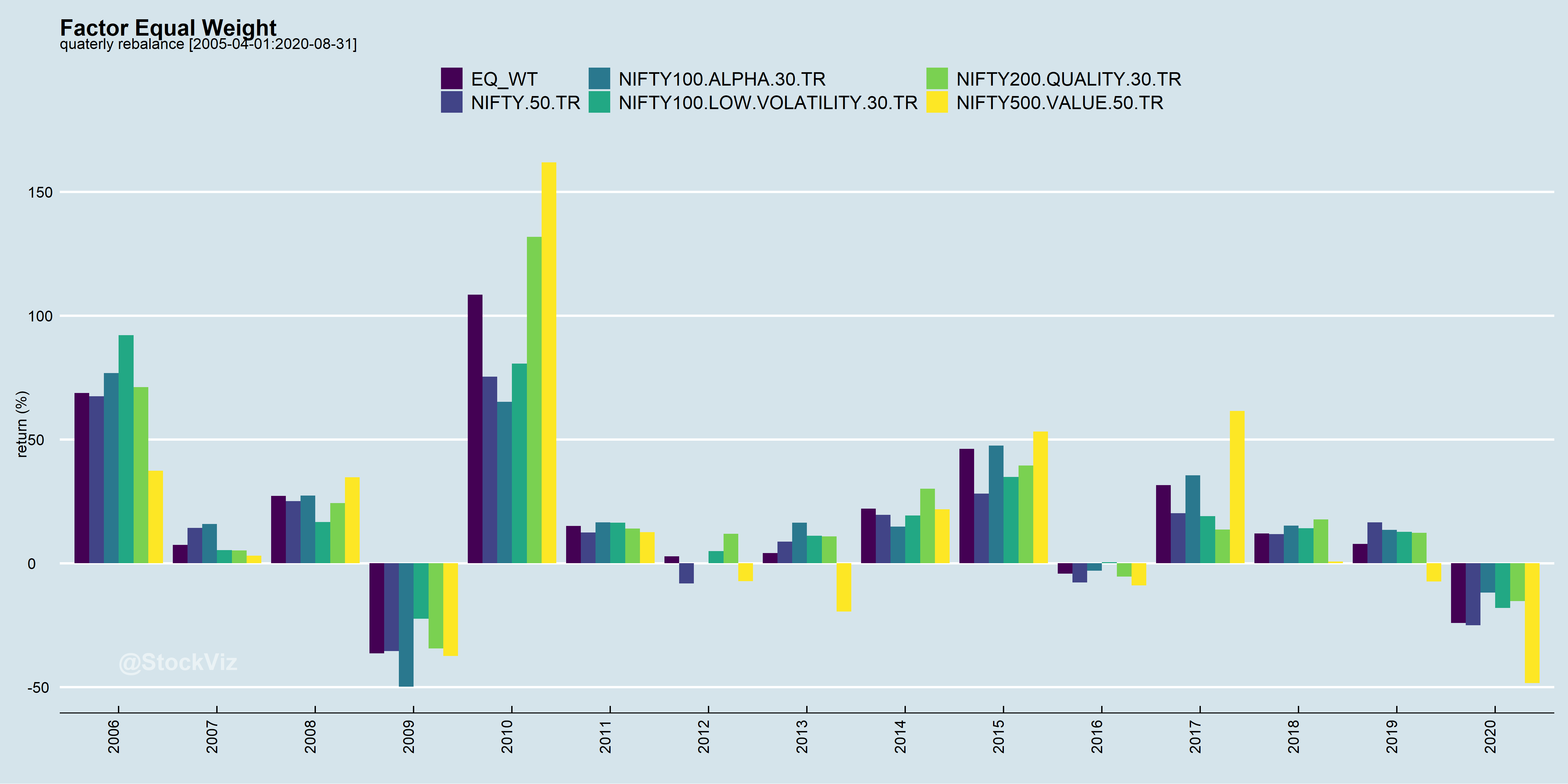

The question is, what if you just took quality, low-volatility and high-alpha (a proxy for momentum) and just equal weighted it? Why choose when you can have all? This is the essence of the Multi-Factor approach to factor investing.

Equal-weighted Factor Portfolio

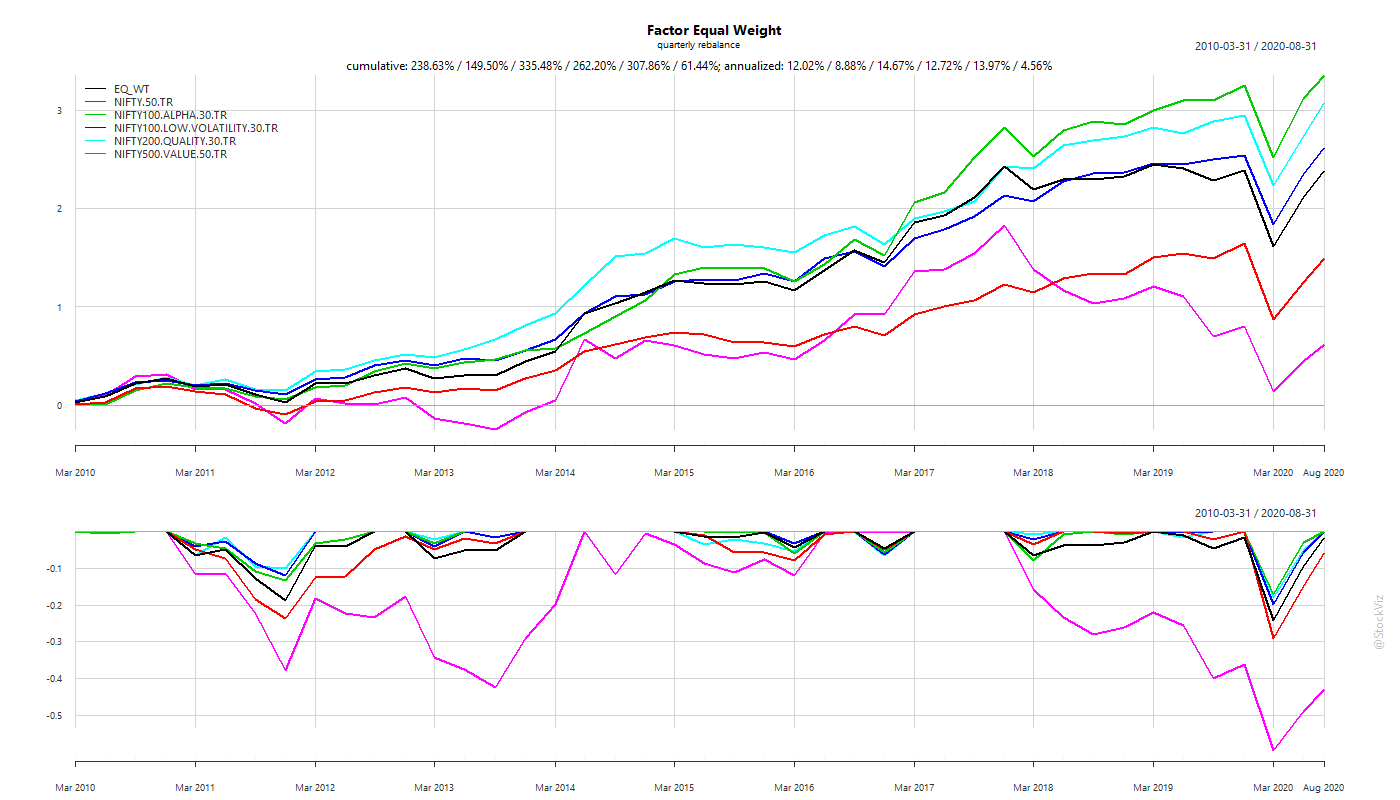

Even if you did a quarterly rebalance, you did better than NIFTY 50.

Since 2010, an equal-weight alpha/low-vol/quality/value factor portfolio gave an annualized return of 12% vs. NIFTY 50’s 8.88%.

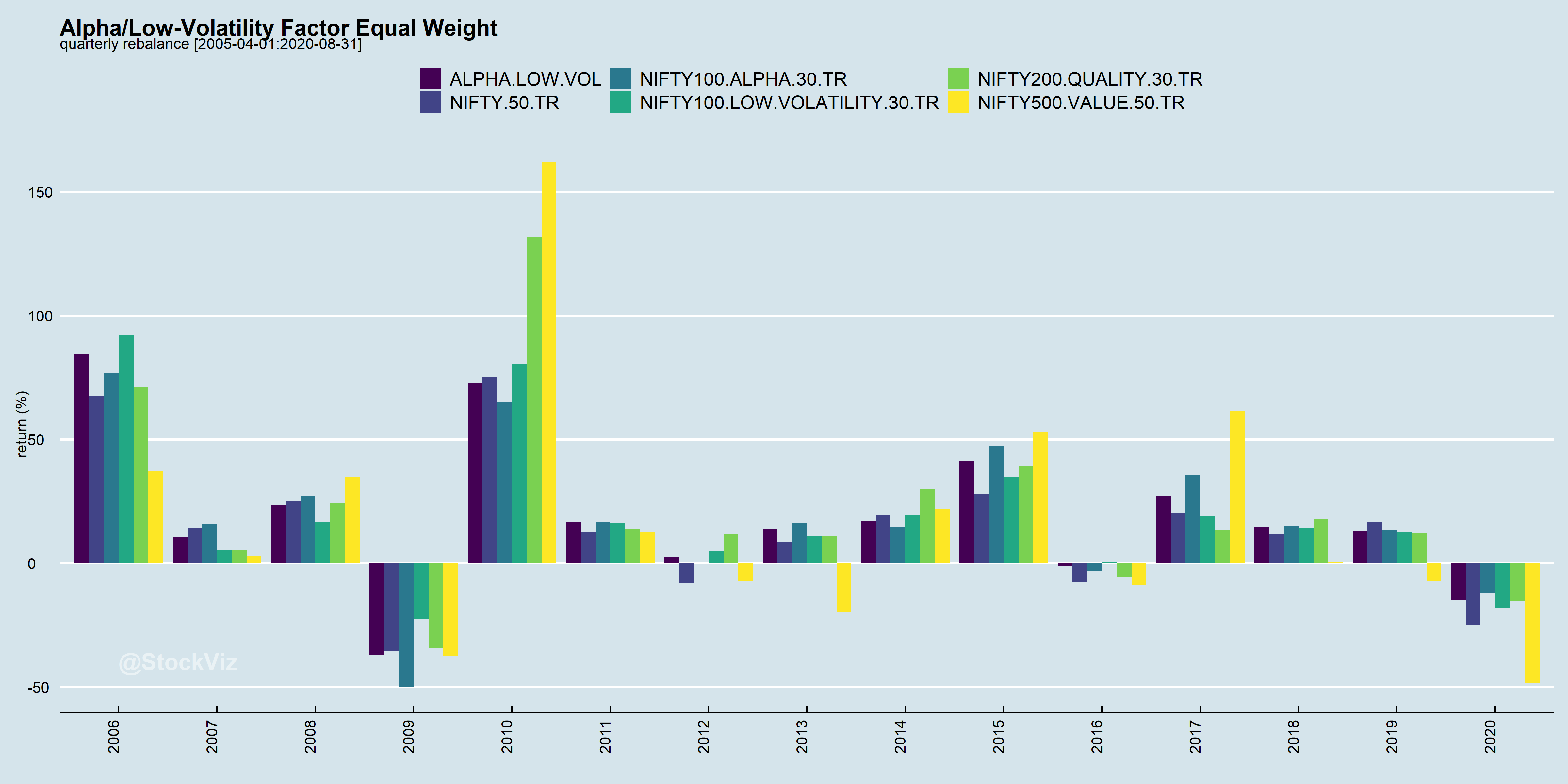

While alpha and low-vol are price-based factors, quality and value are based on company fundamentals. What if, we just equal weighted the price-based factors?

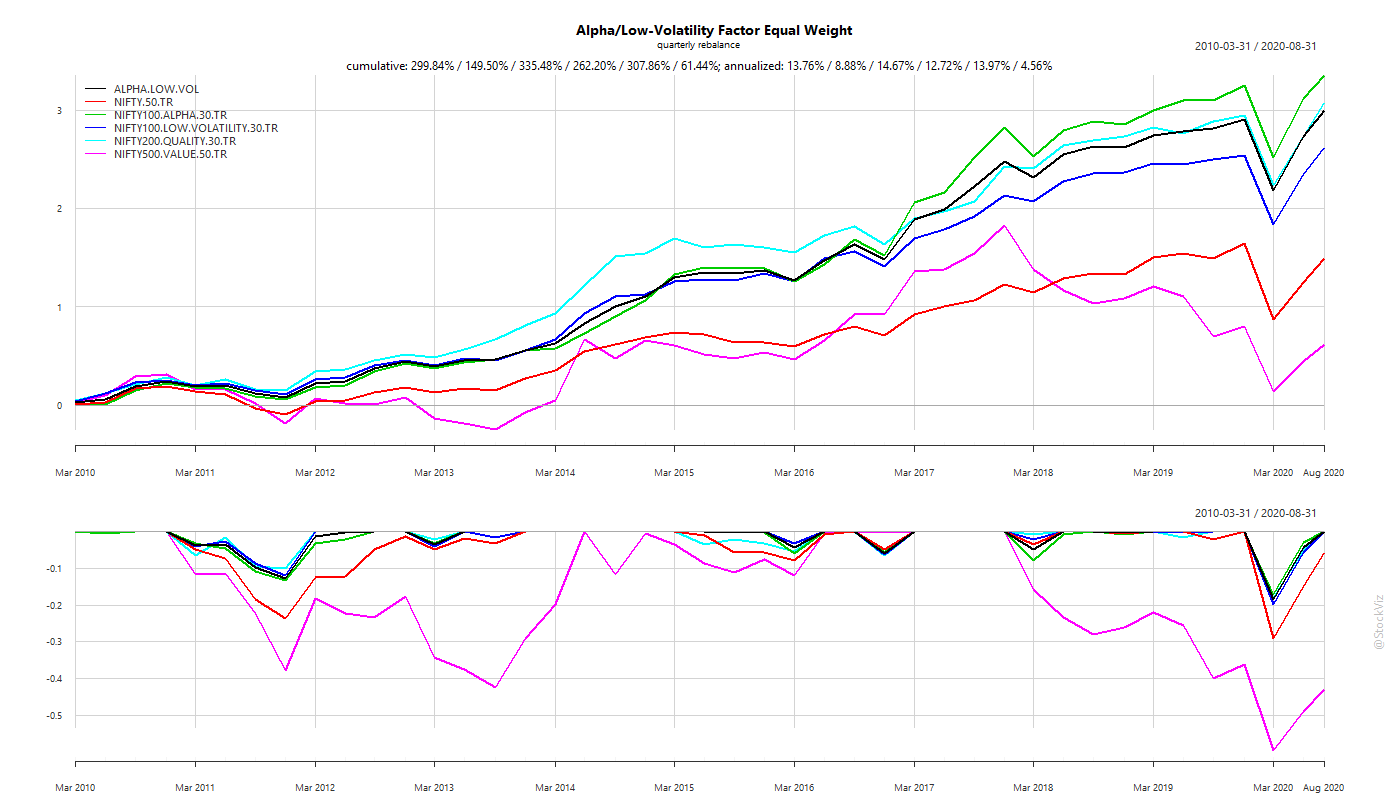

Equal-weighted Alpha and Low-Volatility Factor Portfolio

Given the out-performance of the low-volatility factor, we see a significant boost to an equal weighted alpha/low-vol portfolio compared to equal weighting all the factors.

To summarize returns since 2010,

equal-weight all factors: 12.02%

equal-weight only alpha and low-vol: 13.76%

NIFTY 50: 8.88%

Caveats

Before transaction costs, we see that factor indices have beaten the NIFTY 50, historically. However, investors should bear these points in mind while looking at index back-tests:

Index Inception – the date from which the index was constructed (since 2005.)

Launch – the date on which the index was launched (in 2018.)

Invested – the date from which a significant amount of money gets invested in the index (in 2019.)

Re-balance frequency – how often does the index rebalance?

At launch, these indices have incorporated over 13 years of historical data. One can’t discount the possibility that there might be some over-fitting to increase their marketability.

Typically, index performance dips once the AUM crosses a tipping point. And given that India has a 0.1% STT (Securities Transaction Tax,) the higher the re-balance frequency, the worse the performance.

The true test of these indices will occur when real money is invested in them over two or three complete cycles.

Conclusion

Both Factor Rotation and Multi-Factor approaches have their pros and cons. However, the one thing that remains common is that these take time to play-out. There are huge year-over-year variances in performance and investors need to stick to an approach long enough for alpha to emerge.

Factor investing is the process of constructing portfolios of stocks by isolating certain statistical properties that have shown to out-perform over the long term. For example, investing in stocks that rank high in the “Quality” factor. Here are some factors that were discussed previously on FreeFloat:

While factor portfolios are expected to out-perform over the long-term (say, 30 years,) there is a strong chance that they under-perform over an individual’s holding period (5-10 years.) This leads to sub-par investment returns due to out-of-favor factors.

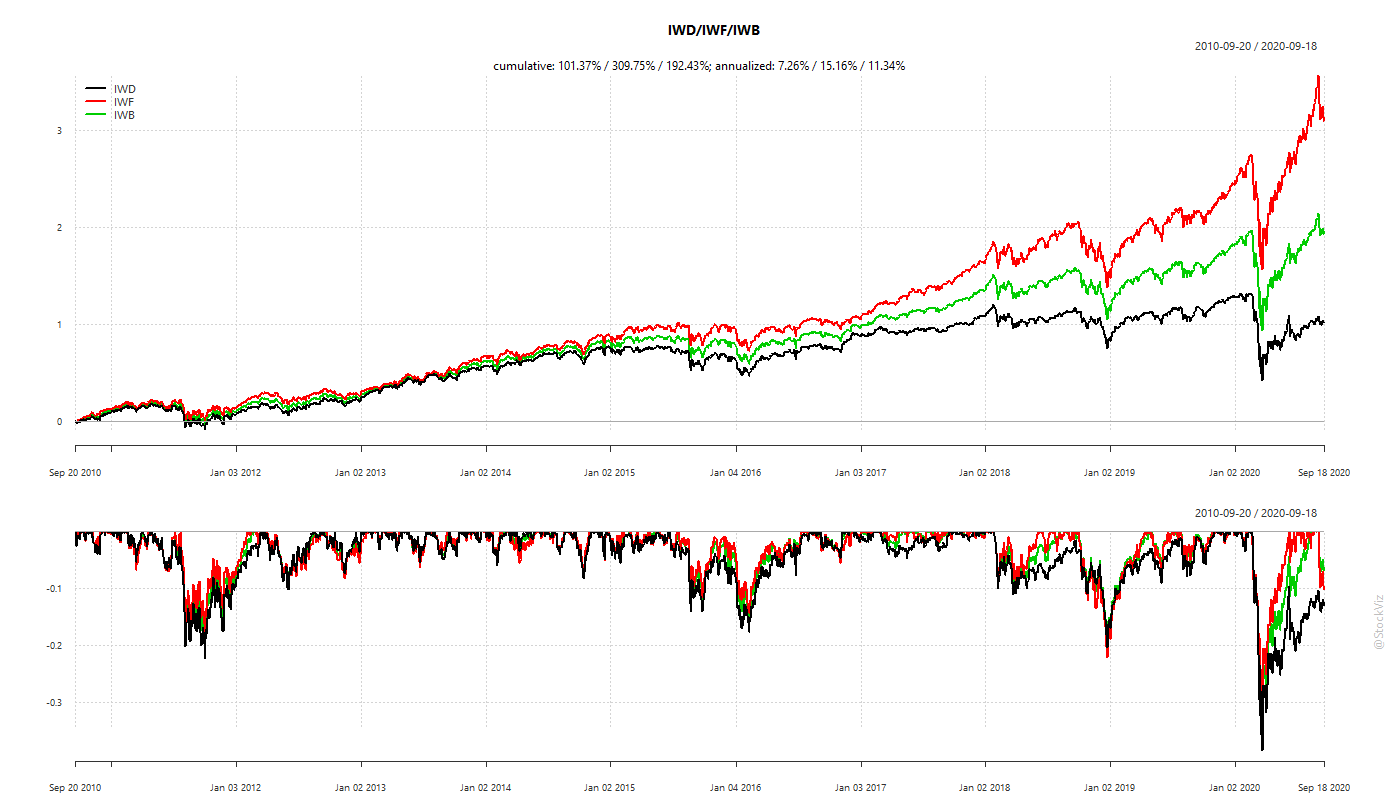

For example, Value vs. Growth.

Is Value/Growth Dead?

Consider IWD, the iShares Russell 1000 Value ETF, IWF, the iShares Russell 1000 Growth ETF and IWB, iShares Russell 1000 ETF.

2000 through 2010, value out-performed.

2010 through 2020, growth out-performed.

Whether you were a “Value” investor or a “Growth” investor, you saw 10-years (!) of under-performance.

Persistence of Out-performance

To avoid under-performing, an investor can:

Market-cap index (avoid choosing.)

Predict (good luck with that.)

Follow the herd (FOMO.)

Turns out, option #3 works pretty well and is robust.

Individual factors can be reliably timed based on their own recent performance.

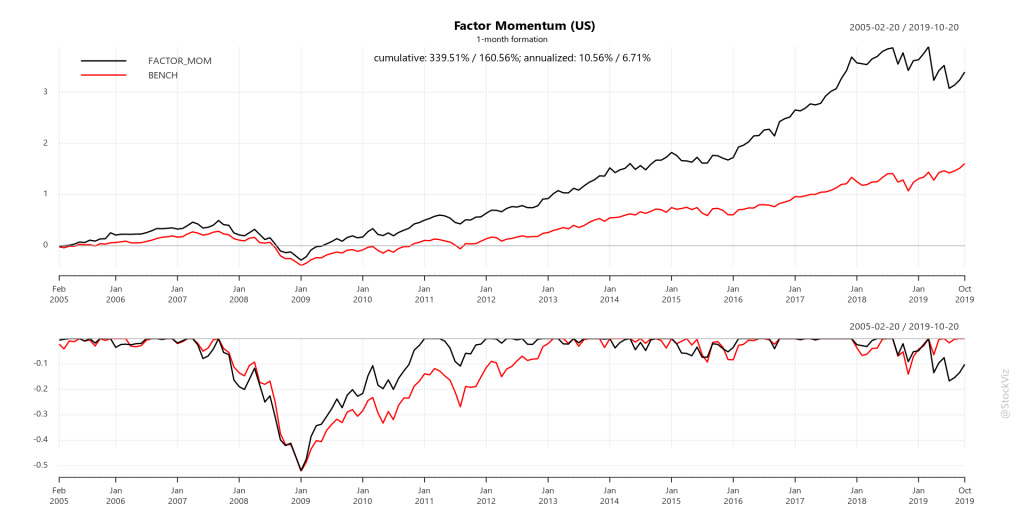

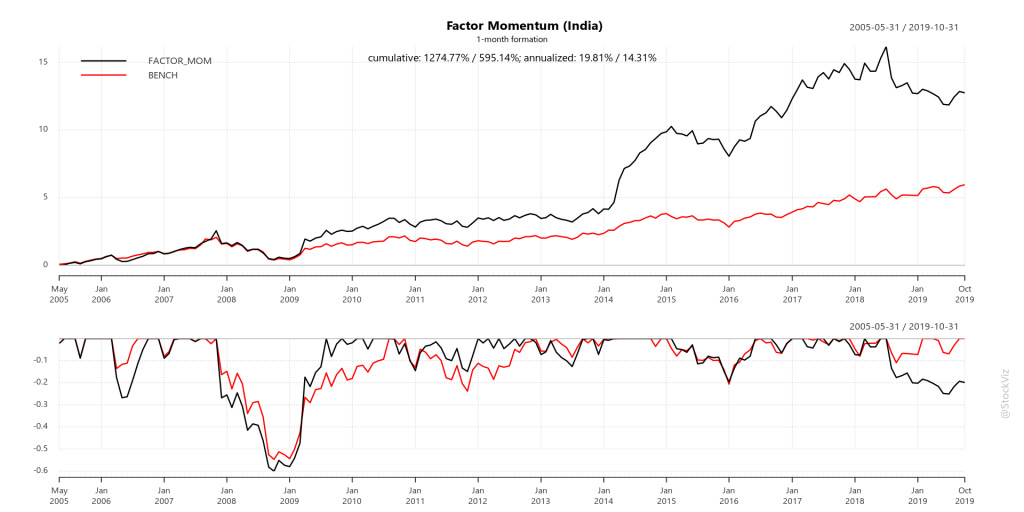

Factor Momentum Everywhere – Tarun Gupta, Bryan T. Kelly (AQR)

Rule: Buy whatever worked in the last month

Worked in the US

Worked in India

The problem, however, is that India has STT (Securities Transaction Tax) that the US doesn’t. And with a high turn-over strategy, STT can completely sap whatever alpha was produced.

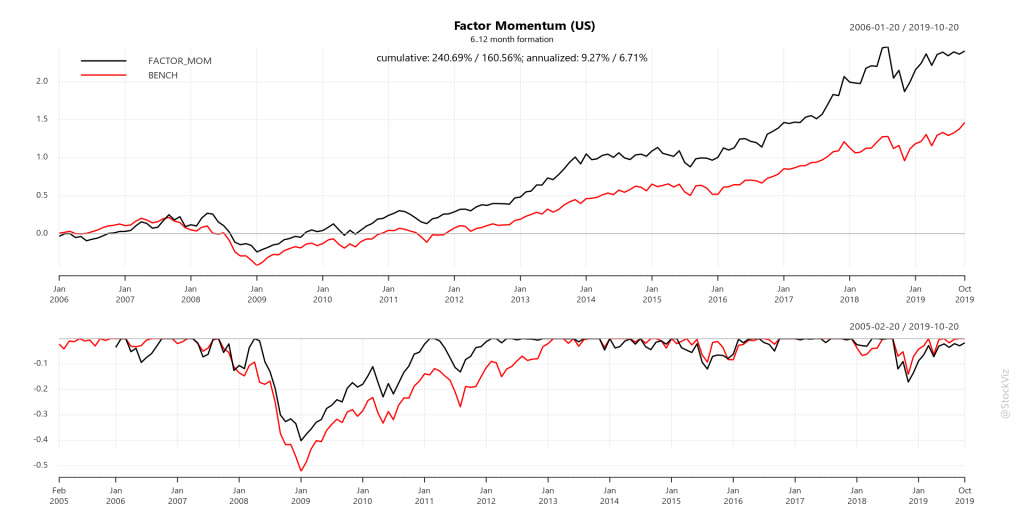

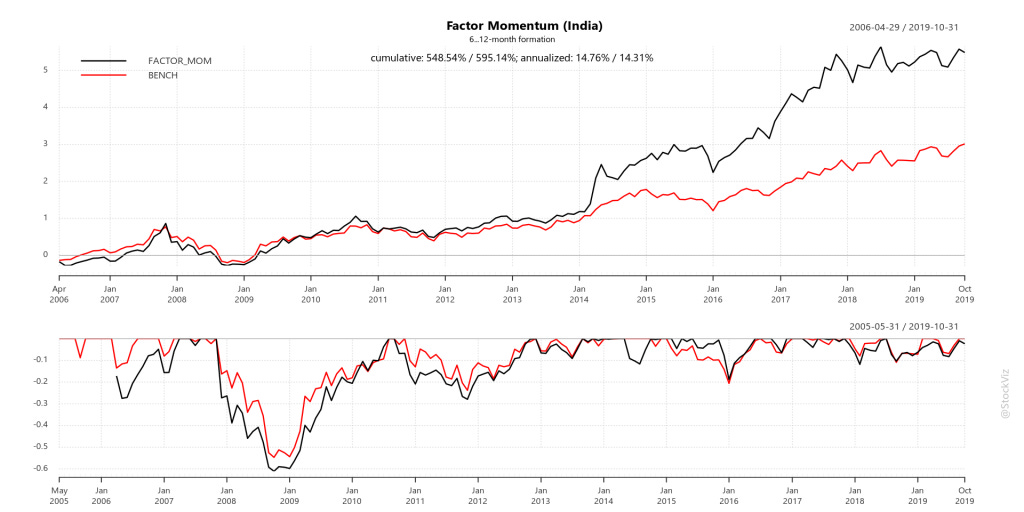

Rule: Buy the one with the Best Average Returns over the last 6-12 months

Worked in the US

Worked in India

Forward-Test

The back-test showed that for the US markets, investors can rotate into the factor that performed the best in the last month. And for India, investors can average into the one that had the best average 6-12 month returns.

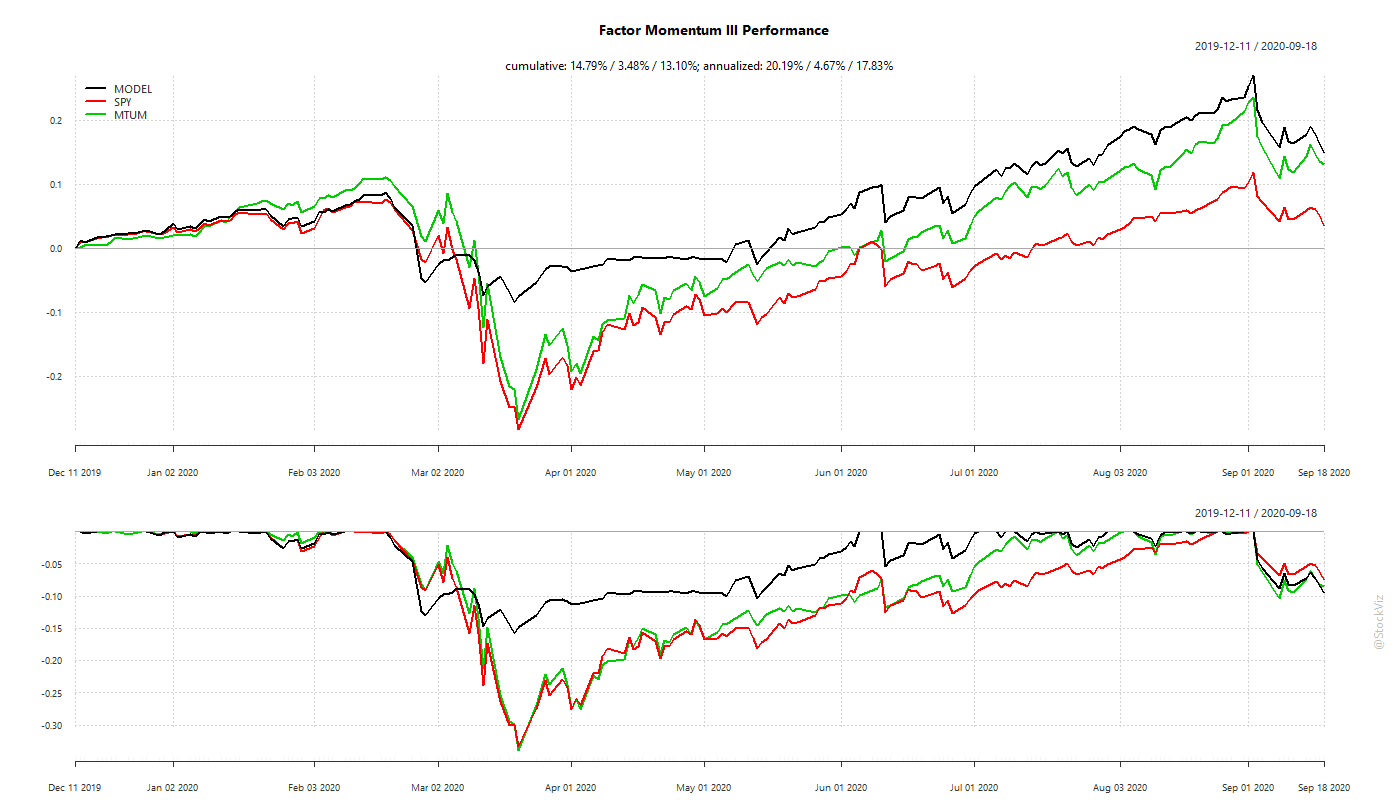

US

The Factor Momentum strategy beat plain-vanilla momentum (MTUM) and S&P 500 (SPY). It also avoided the Corona Cliff in March 2020.

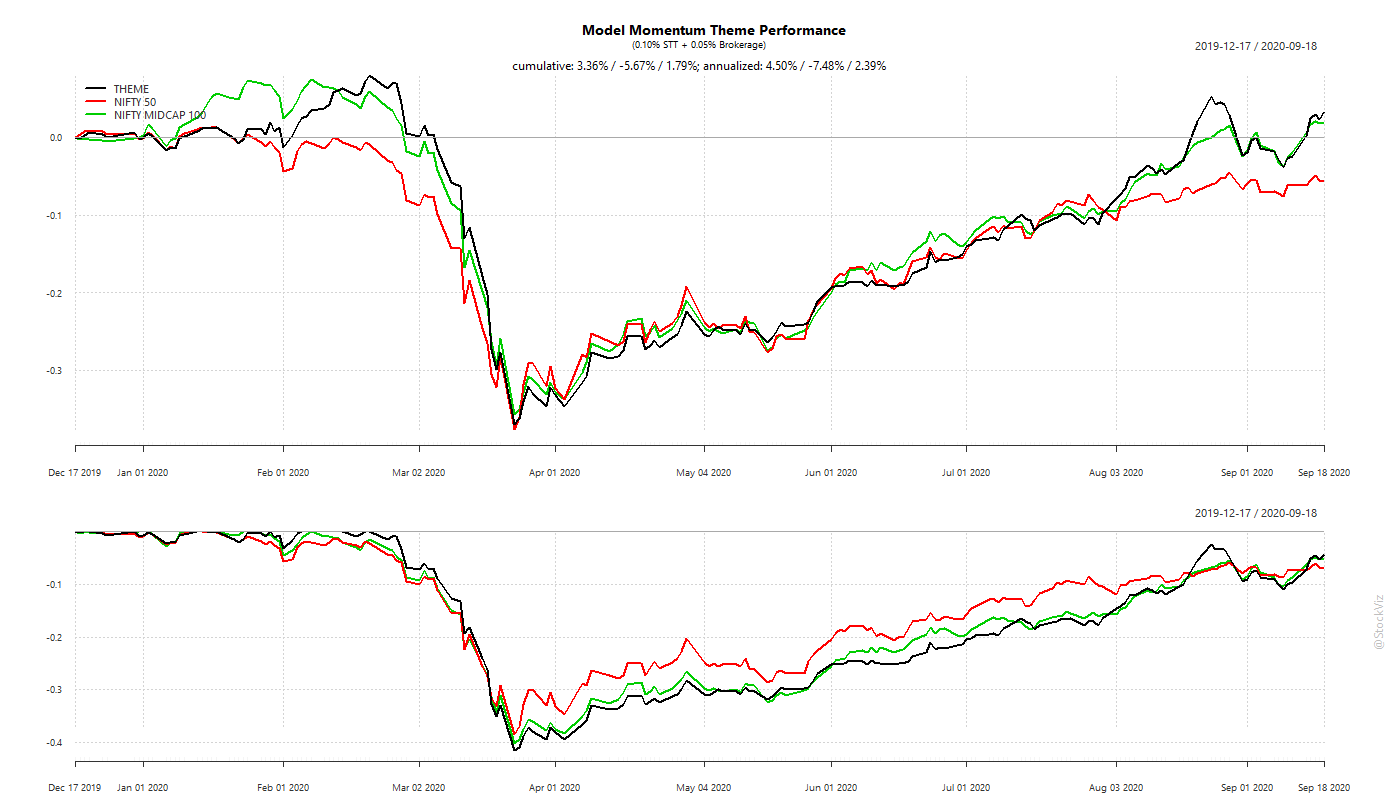

India

The Indian version of the Factor Momentum strategy is a mixed bag. Since it averages over a longer time-period, it is (understandably) slow to respond to sudden events. The dive during the Corona Cliff and subsequent performance is inline with the back-test. Thus far, it has marginally out-performed NIFTY 50 and MIDCAP 100 after STT and brokerage and we remain optimistic about its future.

Conclusion

Factor Rotation holds promise. Research, back-tests and forward-tests confirm. The trade-off is pretty clear as well: shorter look-backs/shallower draw-downs vs. transaction costs. Since trading US equities is nearly friction free, investors can use shorter look-backs. Indian investors will have to stomach deeper draw-downs given transaction taxes.