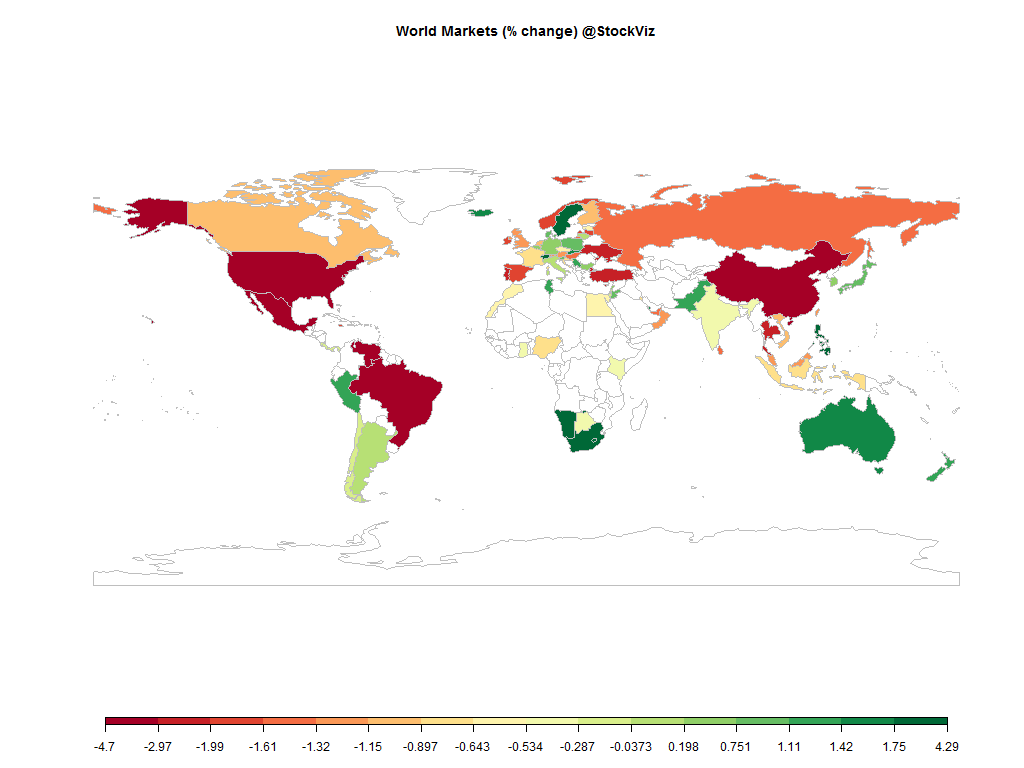

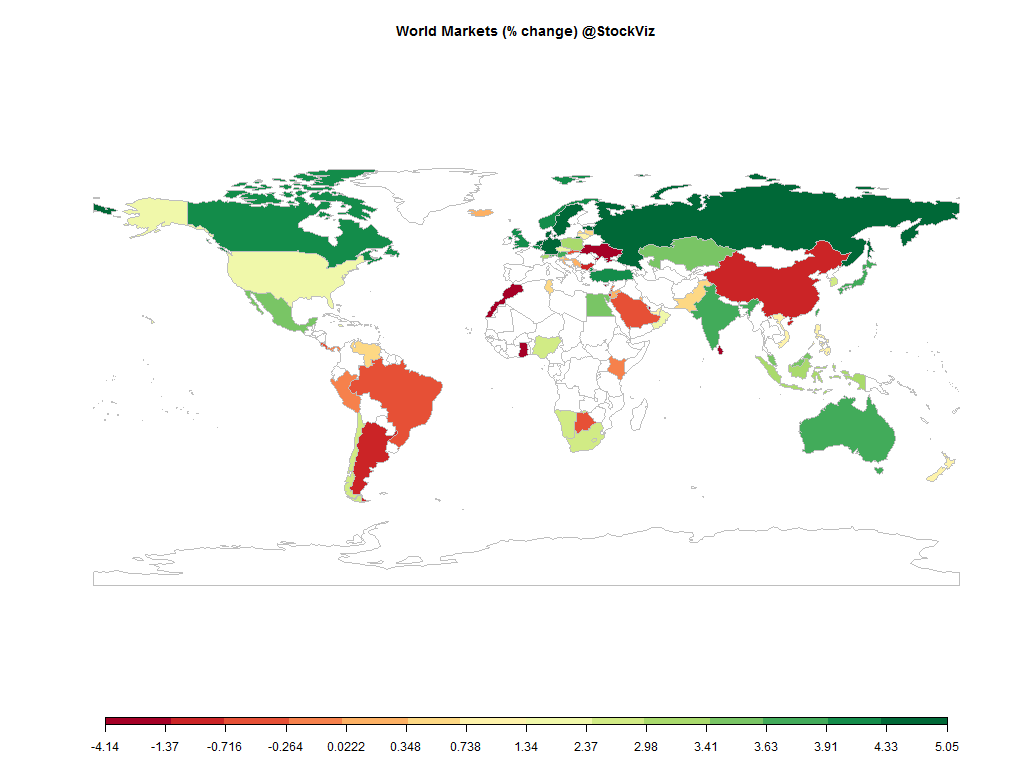

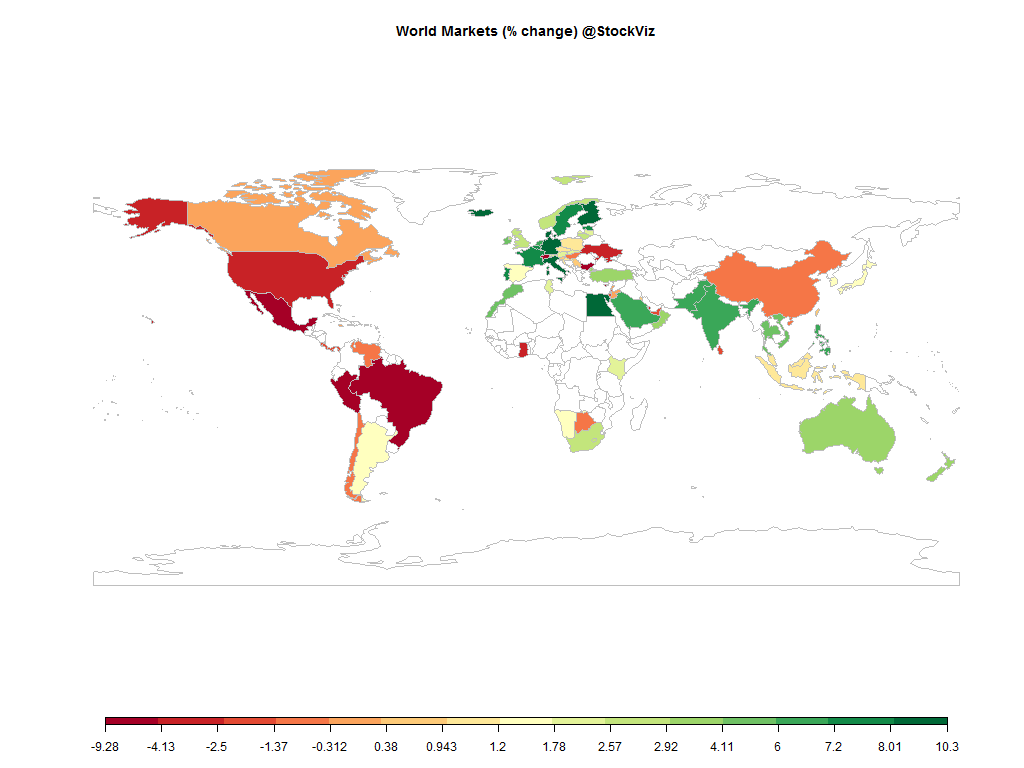

Equities

| MINTs | |

|---|---|

| JCI(IDN) | +1.19% |

| INMEX(MEX) | -6.09% |

| NGSEINDX(NGA) | -14.70% |

| XU030(TUR) | +3.79% |

| BRICS | |

|---|---|

| IBOV(BRA) | -6.20% |

| SHCOMP(CHN) | -0.75% |

| NIFTY(IND) | +6.35% |

| INDEXCF(RUS) | +17.98% |

| TOP40(ZAF) | +2.60% |

Commodities

| Energy | |

|---|---|

| Heating Oil | -9.59% |

| Brent Crude Oil | -6.64% |

| Ethanol | -15.22% |

| WTI Crude Oil | -9.49% |

| Natural Gas | -9.44% |

| RBOB Gasoline | +2.30% |

| Metals | |

|---|---|

| Copper | -10.92% |

| Gold 100oz | +7.99% |

| Platinum | +2.27% |

| Palladium | -3.38% |

| Silver 5000oz | +9.55% |

Currencies

| MINTs | |

|---|---|

| USDIDR(IDN) | +2.29% |

| USDMXN(MEX) | +1.54% |

| USDNGN(NGA) | +2.25% |

| USDTRY(TUR) | +4.55% |

| BRICS | |

|---|---|

| USDBRL(BRA) | +0.94% |

| USDCNY(CHN) | +0.73% |

| USDINR(IND) | -1.86% |

| USDRUB(RUS) | +19.40% |

| USDZAR(ZAF) | +0.79% |

| Agricultural | |

|---|---|

| Cocoa | -3.55% |

| Coffee (Robusta) | +1.53% |

| Lumber | -2.74% |

| Soybean Meal | -9.07% |

| White Sugar | -2.07% |

| Soybeans | -5.88% |

| Coffee (Arabica) | -4.31% |

| Corn | -7.56% |

| Feeder Cattle | -6.25% |

| Wheat | -14.73% |

| Cattle | -6.55% |

| Cotton | -2.45% |

| Lean Hogs | -17.35% |

| Orange Juice | +0.07% |

| Sugar #11 | +1.44% |

Credit Indices

| Index | Change |

|---|---|

| Markit CDX EM | -2.75% |

| Markit CDX NA HY | -0.52% |

| Markit CDX NA IG | +2.54% |

| Markit iTraxx Asia ex-Japan IG | +5.51% |

| Markit iTraxx Australia | +2.89% |

| Markit iTraxx Europe | -7.13% |

| Markit iTraxx Europe Crossover | -36.06% |

| Markit iTraxx Japan | -2.64% |

| Markit iTraxx SovX Western Europe | -2.88% |

| Markit LCDX (Loan CDS) | +0.24% |

| Markit MCDX (Municipal CDS) | +3.87% |

We certainly started the party with a bang: Euro QE, Swiss abandon, Rajan rate-cut… Oh my!

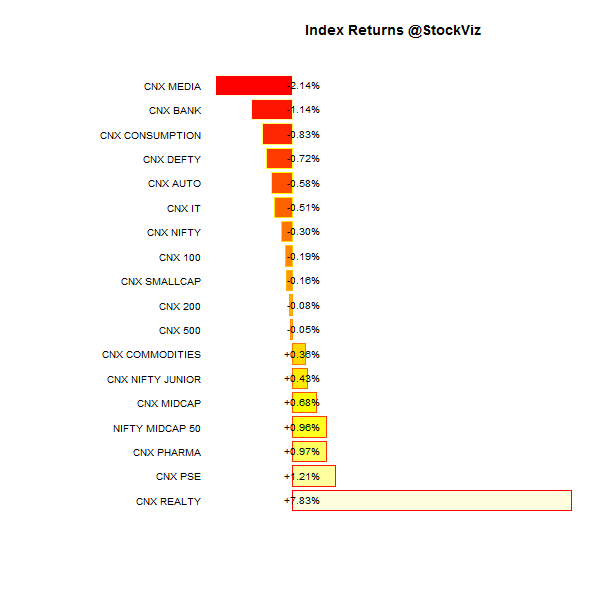

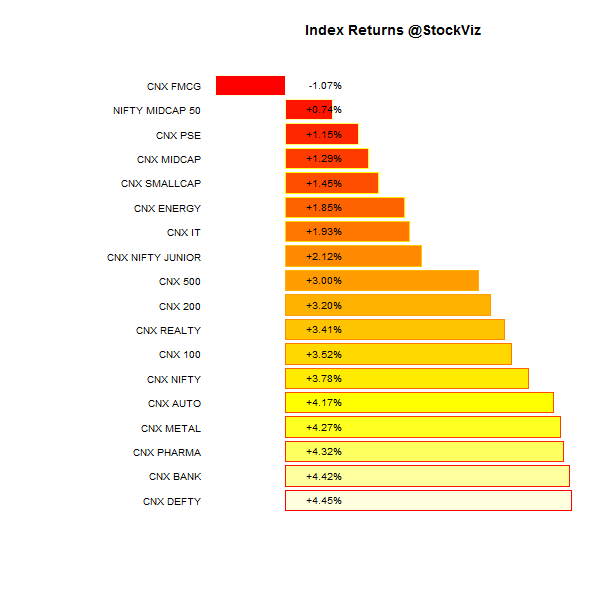

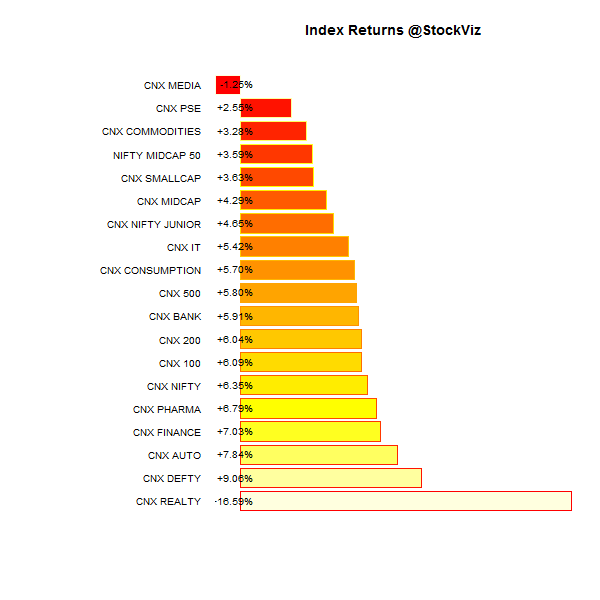

Index Returns

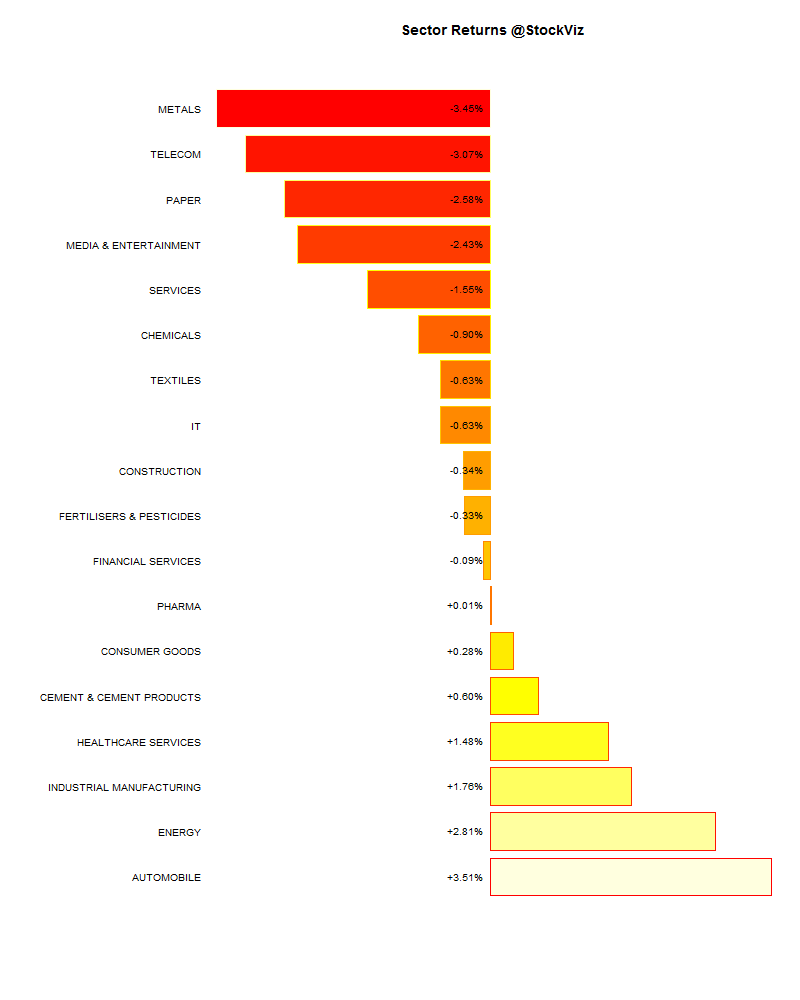

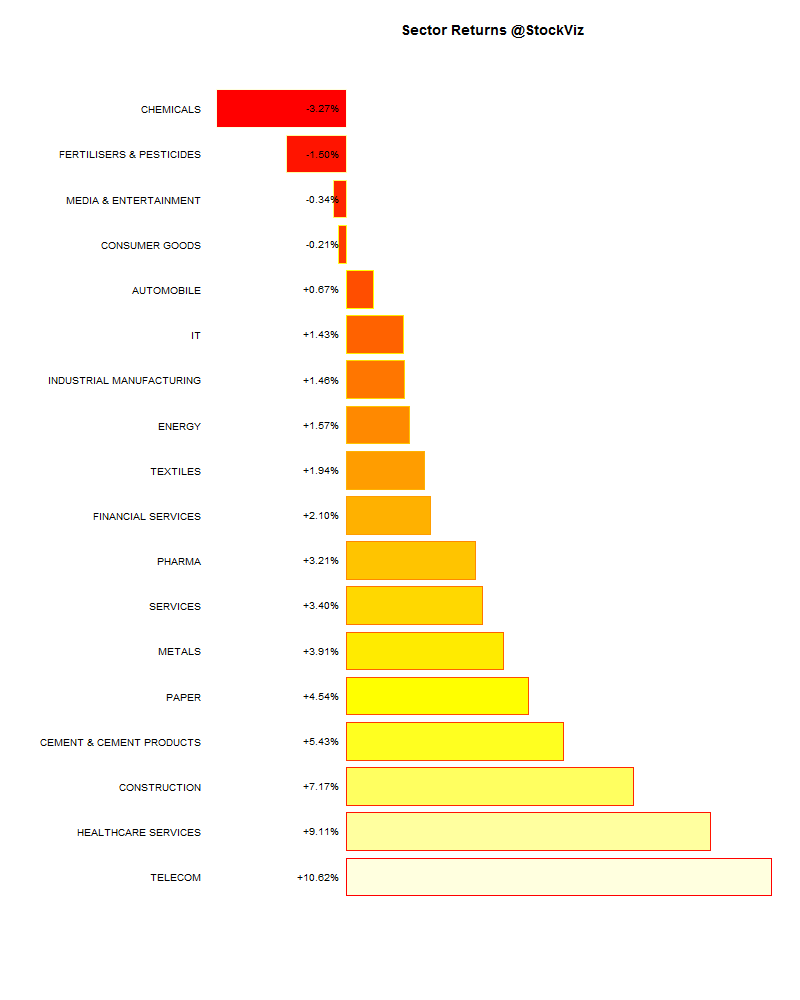

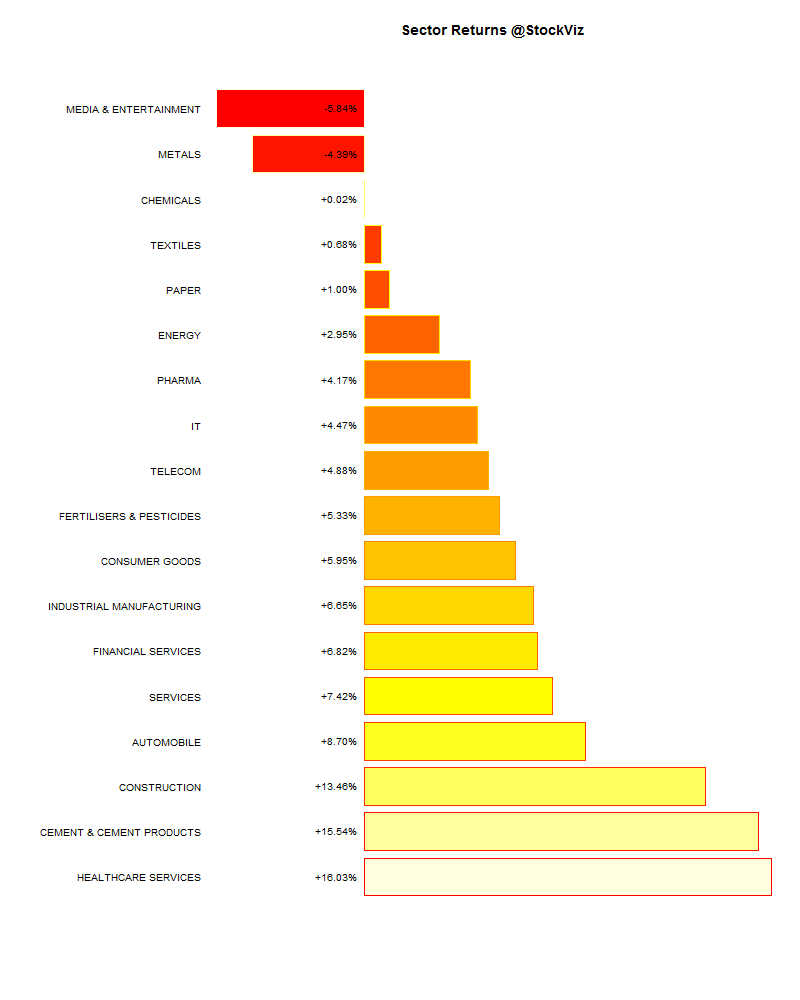

Sector Performance

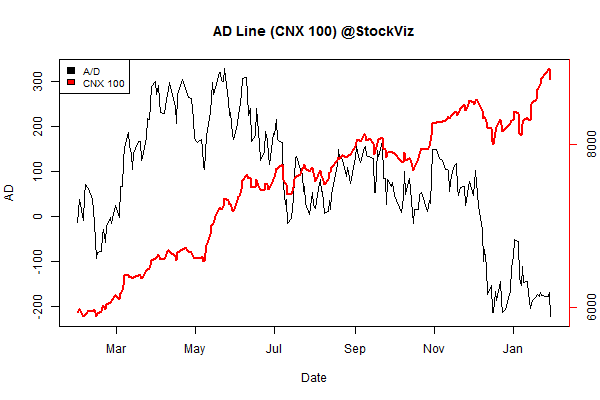

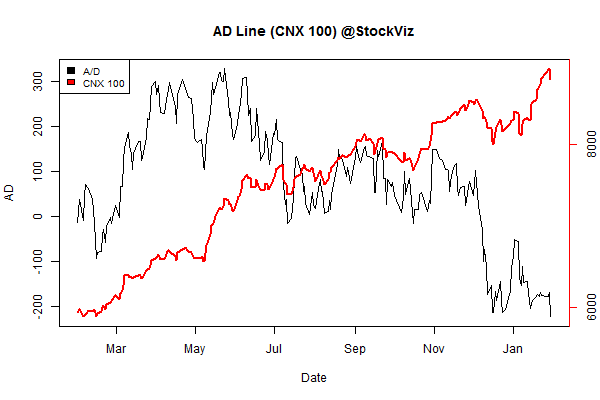

Advance Decline

Market Cap Decile Performance

| Decile | Mkt. Cap. | Adv/Decl |

|---|---|---|

| 1 (micro) | -3.90% | 68/66 |

| 2 | +2.62% | 79/54 |

| 3 | +0.33% | 73/60 |

| 4 | +2.82% | 81/52 |

| 5 | +4.56% | 72/61 |

| 6 | +3.52% | 81/52 |

| 7 | +7.85% | 77/56 |

| 8 | +5.76% | 76/57 |

| 9 | +5.68% | 69/64 |

| 10 (mega) | +8.38% | 69/65 |

Large caps did good. Midcaps not so much.

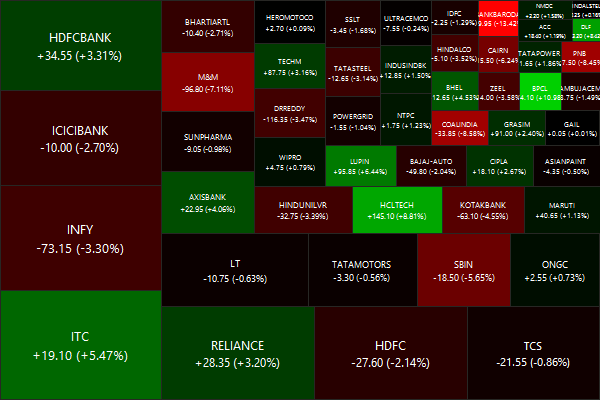

Top Winners and Losers

DLF – looks like the market likes the EMI scheme. M&MFIN and PNB got shellacked because of poor shows at earnings parade. The Adanis continued to entertain…

ETF Performance

| INFRABEES | +7.79% |

| NIFTYBEES | +6.68% |

| BANKBEES | +5.84% |

| JUNIORBEES | +5.46% |

| GOLDBEES | +4.65% |

| CPSEETF | -0.12% |

| PSUBNKBEES | -3.71% |

Had gold found a bottom?

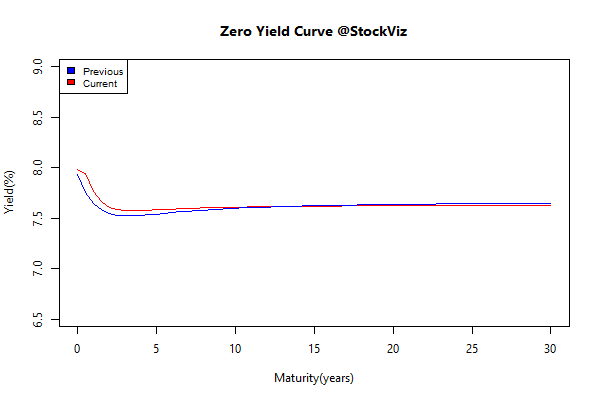

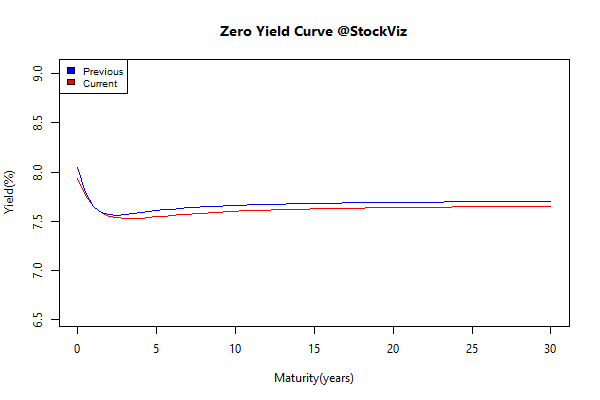

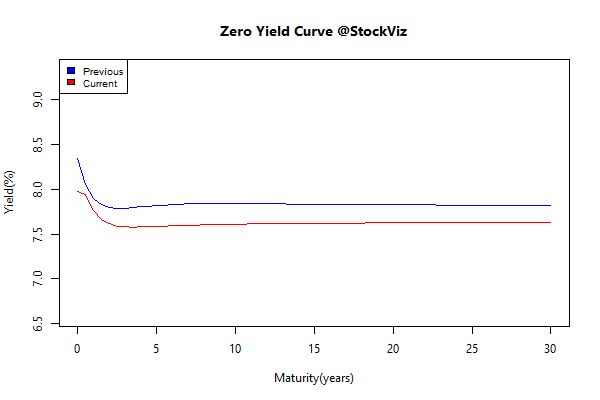

Yield Curve

Bond Indices

| Sub Index | Change in YTM | Total Return(%) |

|---|---|---|

| GSEC TB | -0.33 | +0.74% |

| GSEC SUB 1-3 | -0.92 | +0.94% |

| GSEC SUB 3-8 | -0.18 | +1.48% |

| GSEC SUB 8 | -0.14 | +1.91% |

The long bond was a rock-star.

Investment Theme Performance

| Growth with Moat | +10.36% |

| Efficient Growth | +9.20% |

| Market Elephants | +8.04% |

| Financial Strength Value | +7.70% |

| Balance-sheet Strength | +5.57% |

| CNX 100 50-Day Tactical | +5.37% |

| Auto | +3.66% |

| Quality to Price | +3.53% |

| Market Fliers | +3.06% |

| Magic Formula Investing | +2.85% |

| The Other Value | +2.19% |

| IT 3rd Benchers | +2.10% |

| Old Economy Value | +1.61% |

| Momentum 200 | +1.54% |

| ADAG Mania | +0.25% |

| Enterprise Yield | +0.22% |

| Refract: PPFAS Long Term Value Fund | -1.63% |

| Piotroski ROC Small Caps | -2.80% |

comme ci comme ça…

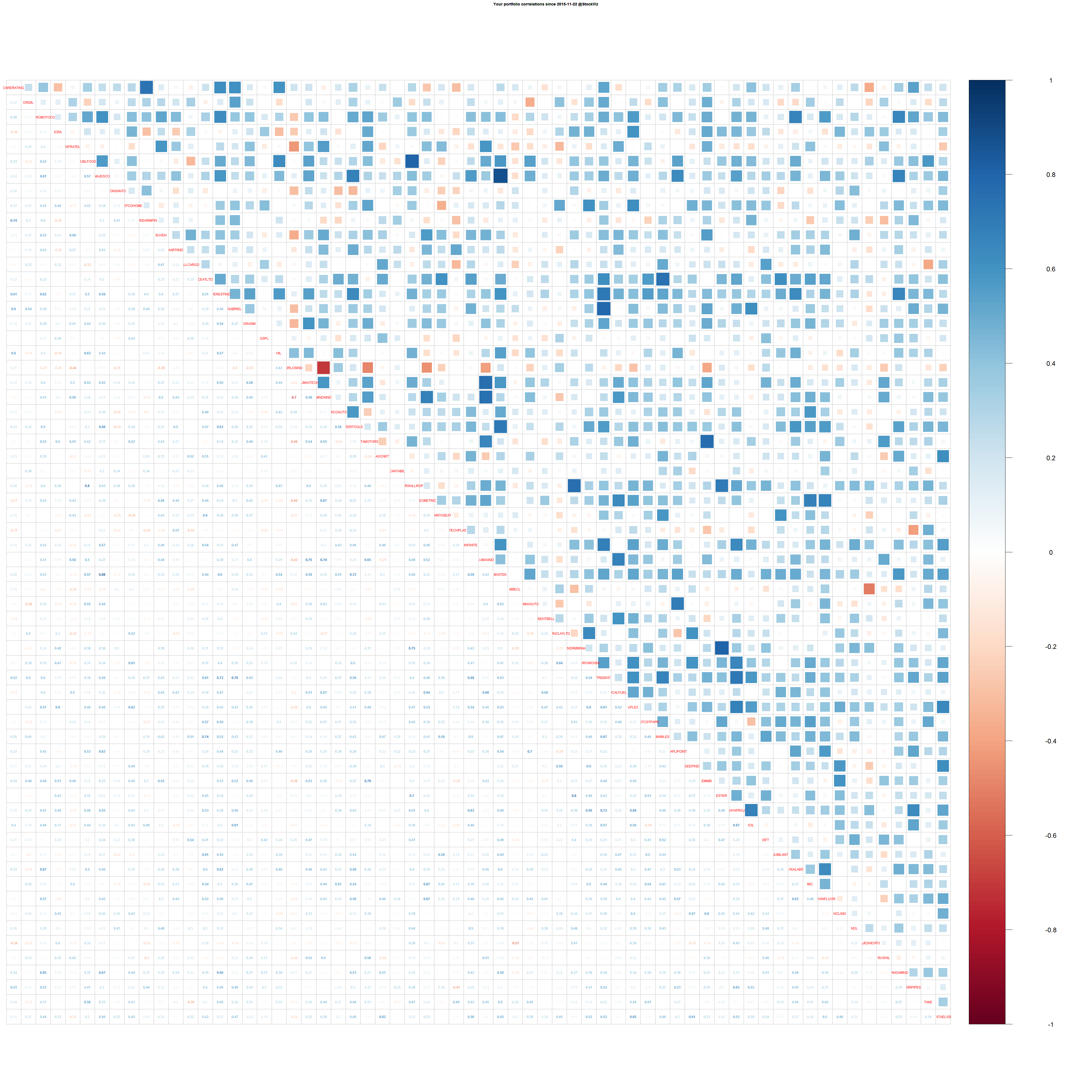

Equity Mutual Funds

Bond Mutual Funds

Thought to sum up the month

Is there such a thing as a “perfect” value investor? Bob Goldfarb, chief executive of the legendary Sequoia Fund, was asked by Columbia University professor Louis Lowenstein “to select ten dyed-in-the-wool value investors who all followed the essential edicts of Graham and Dodd.”

Goldfarb came up with nine. For a nine-year period from 2006 through 2014, the average return of the eight funds that survived to the end was 6.70% vs. the S&P 500 Index’s 7.99%.

Source: Looking Back at James Montier’s “Perfect” Value Investors