A recent article in WSJ had this to say about emerging market bonds:

Research on hard-currency bonds since Britain and Prussia defeated France at the Battle of Waterloo in 1815 shows that on average the return from lending to governments issuing external debt in sterling or dollars delivered a return close to U.S. stocks, with lower volatility.

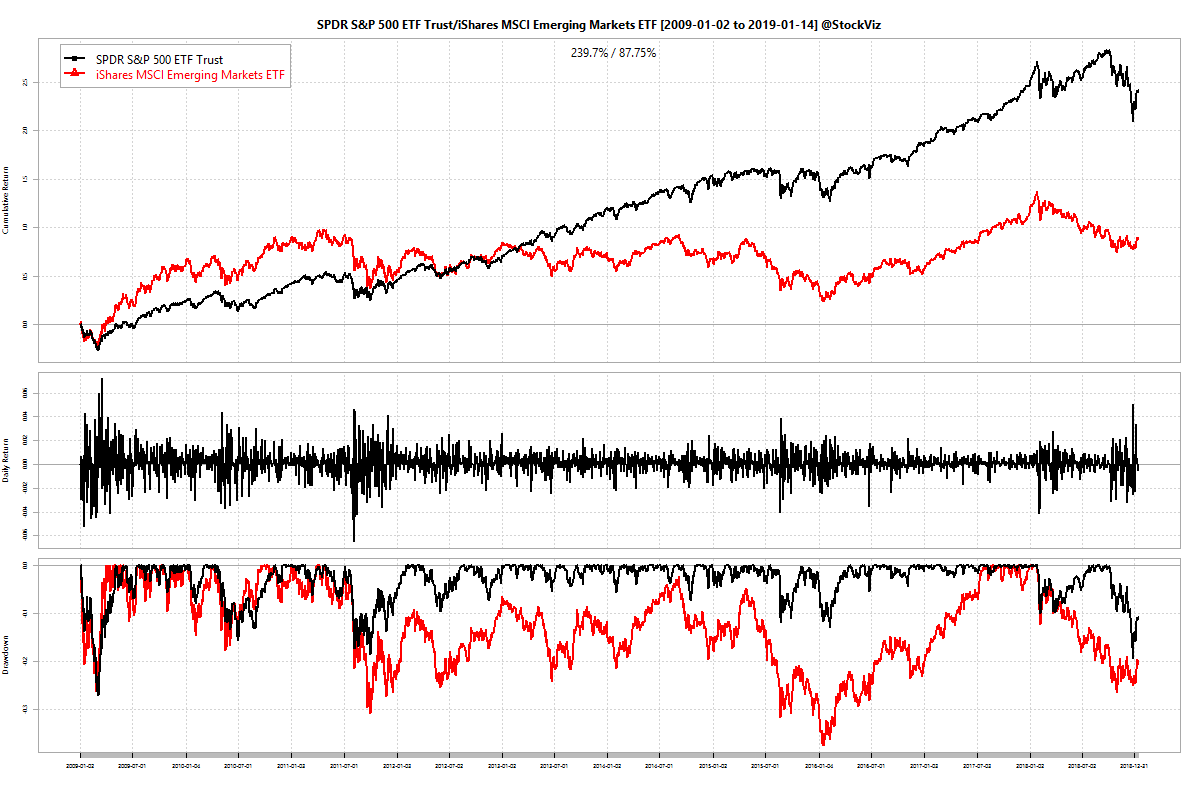

EM bonds giving better returns than US stocks seems counter-intuitive. There is an ETF that tracks the bond index that the article talks about: EMB – iShares JP Morgan USD Emerging Markets Bond ETF. The ETF was launched on December 2007 (not during the Battle of Waterloo,) so we cannot really put that claim to test. However, here are the last 10-years for EMB, EEM (iShares MSCI Emerging Markets ETF) and SPY (SPDR S&P 500 ETF Trust):

EM bonds beat EM equities, but not US stocks (SPY). US mega-caps pretty much beat every other equity market. Here are the MSCI indices of USA, WORLD ex US and EM:

.cumulative.2007-11-30.2019-02-28.png)

Can’t really single out EM for under-performance when everything trailed. Besides, if you look at performance since 1987, aggregate returns from EM have been on par with those of US with complementary periods:

.cumulative.1987-12-31.2019-02-28.png)

So, should you ditch your EM equities portfolio and get into EM bonds and US stocks? Some analysts could look at a decade of EM equity under-performance, point to its valuation spread vs. US mega-caps, and conclude that EMs are a better place to be for the next decade. While others could point out that the US is the home to most of the world’s biggest tech monopolies so it deserves the out-performance. We will only know who is right once 2030 rolls in. Until then, diversify your portfolio and enjoy your life.

Code and annual return charts are on github.