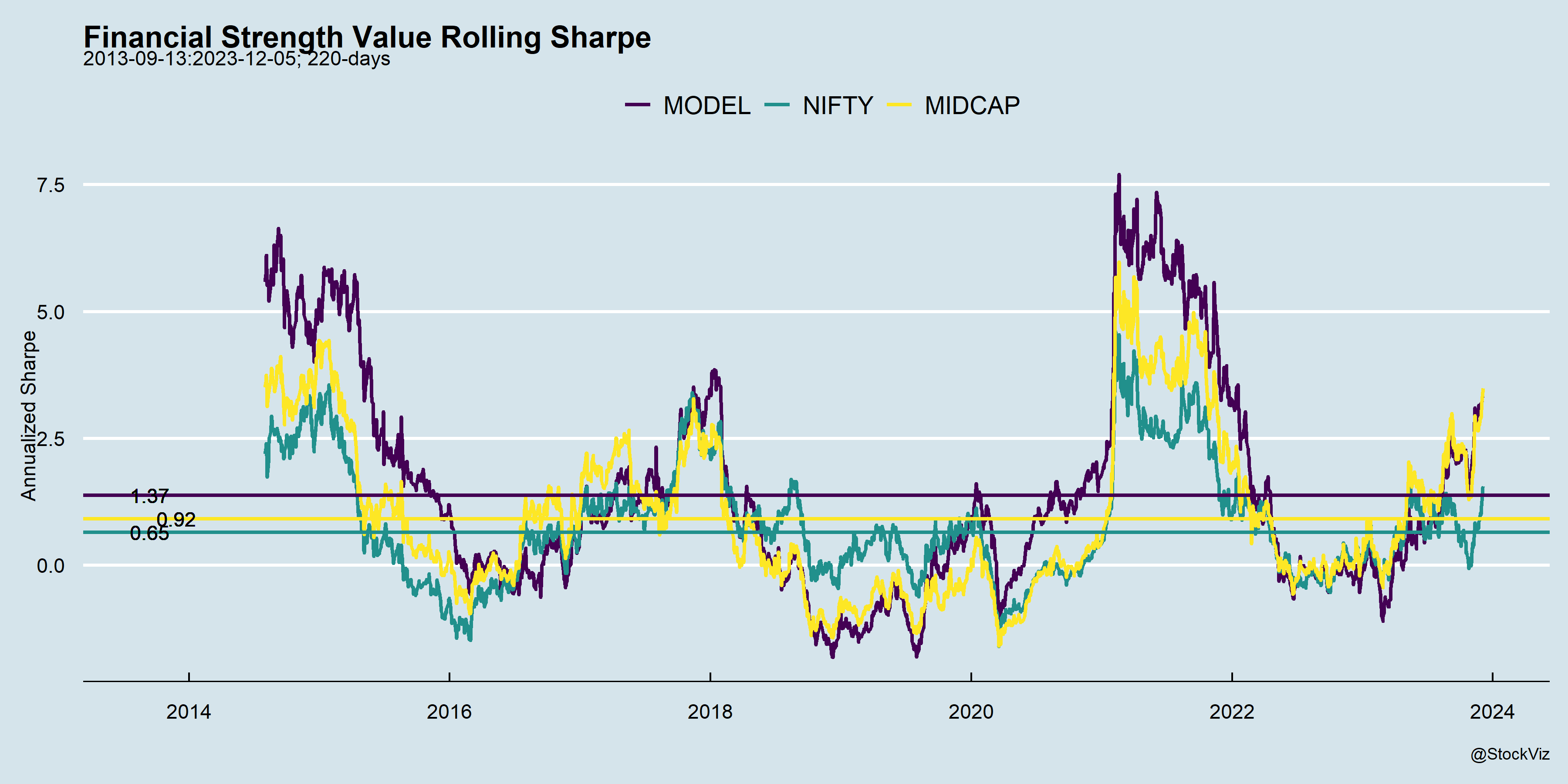

In an earlier post, we discussed how the risk-free rate influences the Sharpe Ratio. Another problem with using lifetime Sharpe to gauge investments is that if you are in the middle of a bull market, then everything looks good.

For example, our All Stars strategy recently hit a Sharpe of 2.0, which is sort of a holy grail in investing. However, if you had looked at it a few months ago, when it was still recovering from a drawdown, you would’ve stayed clear of it. So, what changed? The everything rally in stocks.

One way to avoid falling into this trap is to also look at the rolling Sharpe ratio over the life of the strategy.

While this is particularly true for momentum strategies that all look exceptional in bull markets, value strategies are not immune to this effect either.

Lifetime metrics are also sensitive to launch dates as well. Long running strategies would’ve seen their fair share of market ups and downs compared to newer ones launched during bear markets.

Rolling metrics will help investors get a better idea about strategy performance.

Previously, we discussed how momentum itself trends and how that can be used to manage risk. Using simple moving averages showed promise when it came to some versions of our slow momentum models (see Trending Momentum Models). However, given the faster turnover of our Momos, it wasn’t a suitable approach (see Trending Momo Models).

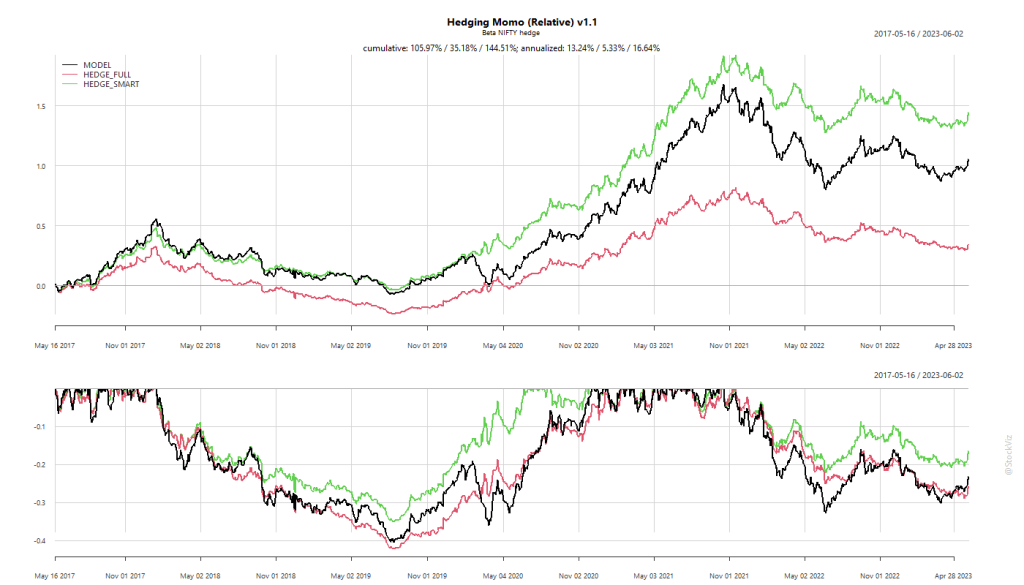

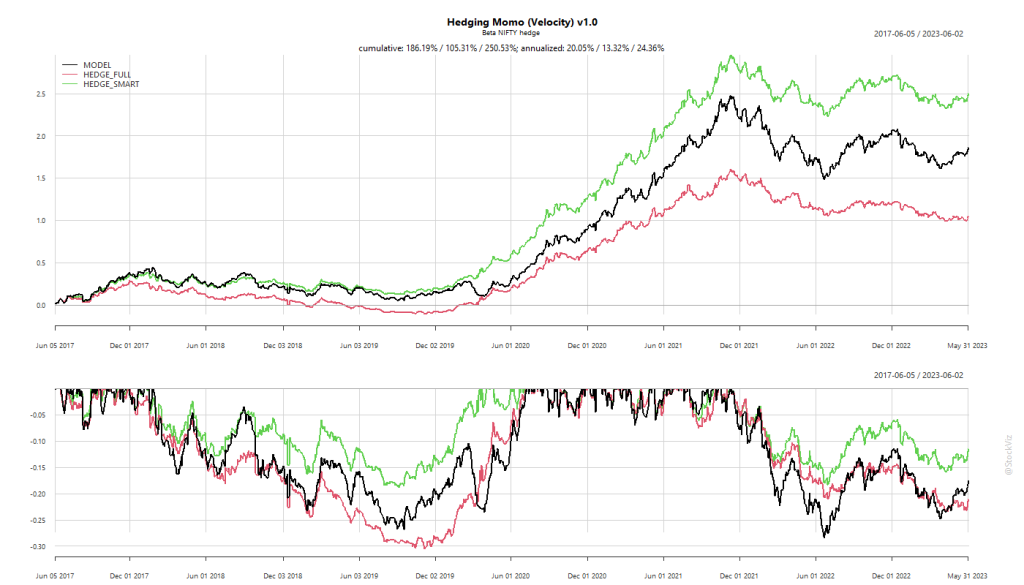

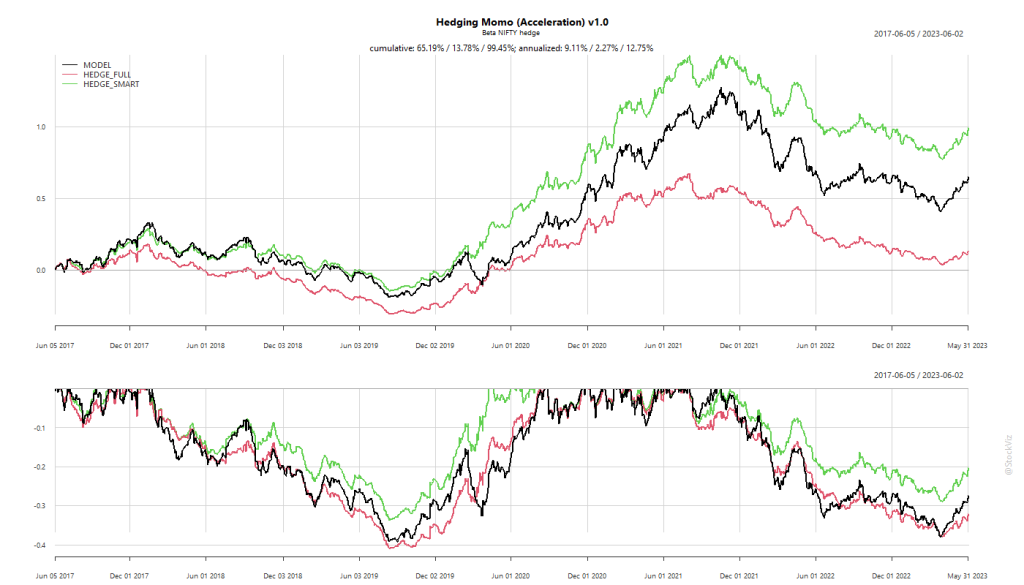

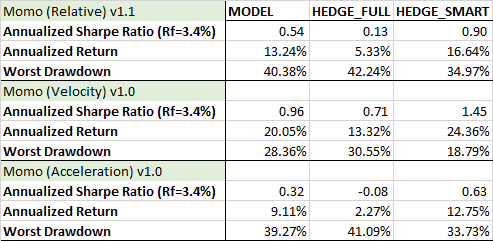

What if we shorted the NIFTY to hedge against market-risk instead?

The naïve approach, tagged “HEDGE_FULL” above, shorts the NIFTY in proportion to the rolling beta of the strategy. Turns out, this is a very sub-optimal way to go about it. Hence “HEDGE_SMART”, that tries to minimize the basis risk inherent in this approach, adds about 3-4% to the strategy’s returns (likely eaten away by transaction costs & taxes) and reduces the max-drawdown by a significant amount.

The question is whether the benefit of lower drawdowns is worth the added cost and complexity? In the case of Velocity, it could be.

Sharpe Ratios are often used to sort through competing investments. It is the original “risk adjusted returns.” It’s a mathematical expression of the insight that excess returns over a period of time may signify more volatility and risk, rather than investing skill (investopedia, wikipedia).

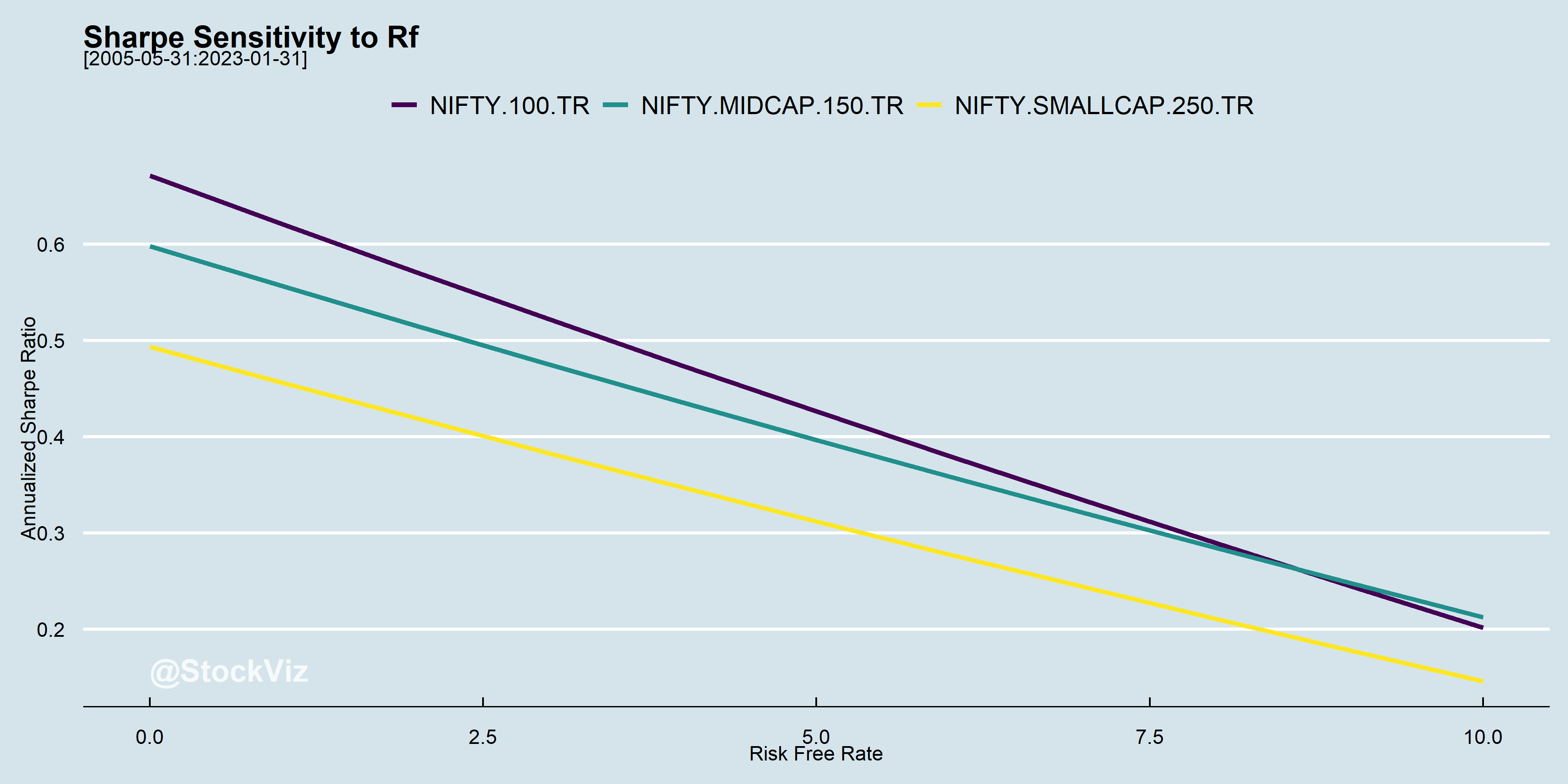

Rb or Rf, the risk-free return, is usually cumbersome to handle. So, typically, it is either set to zero or a constant value. The problem is that rates vary over time and has an impact on the relative ordering of investments.

At high interest rates, SR(mid-caps) > SR(large-caps)

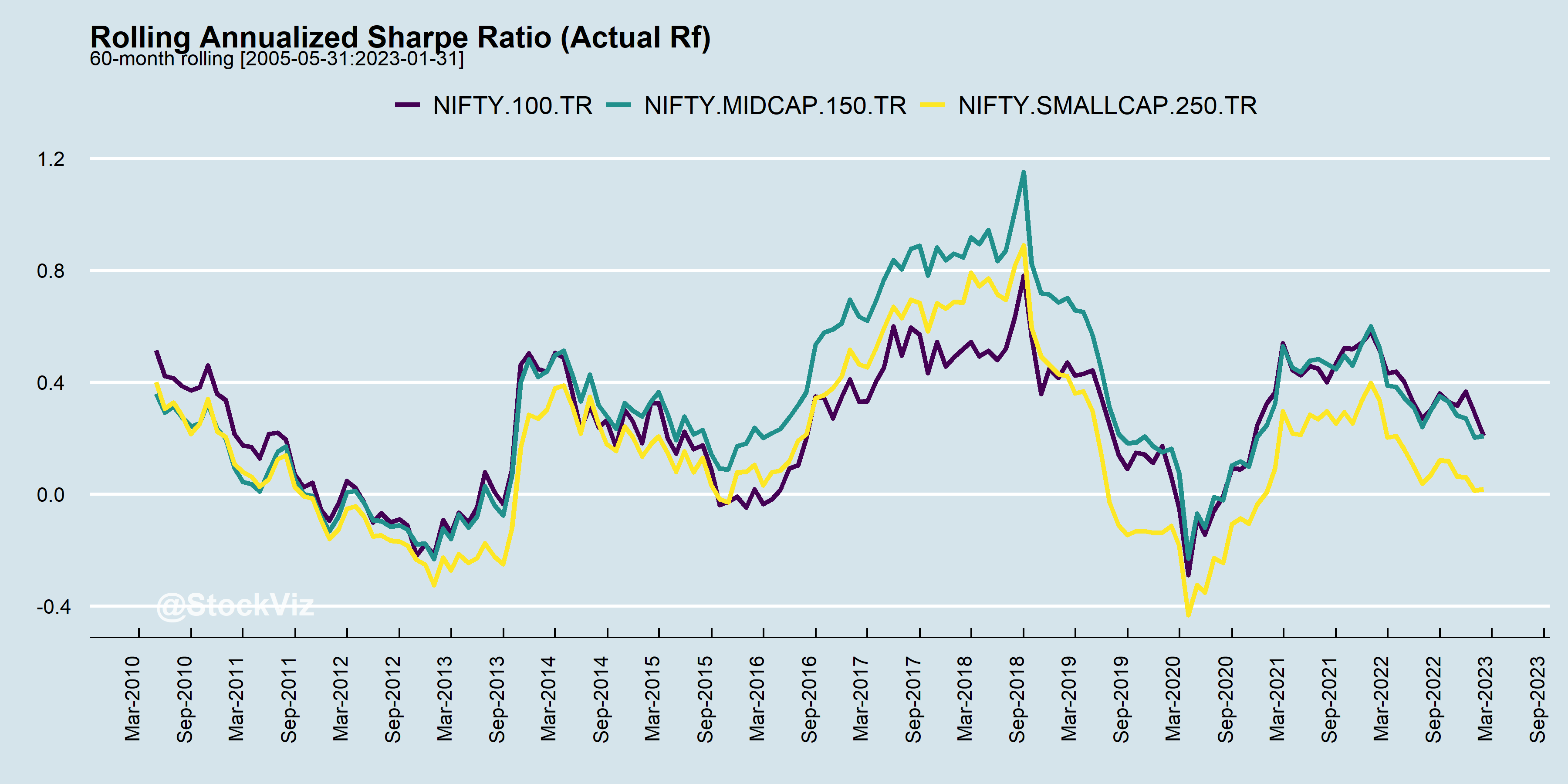

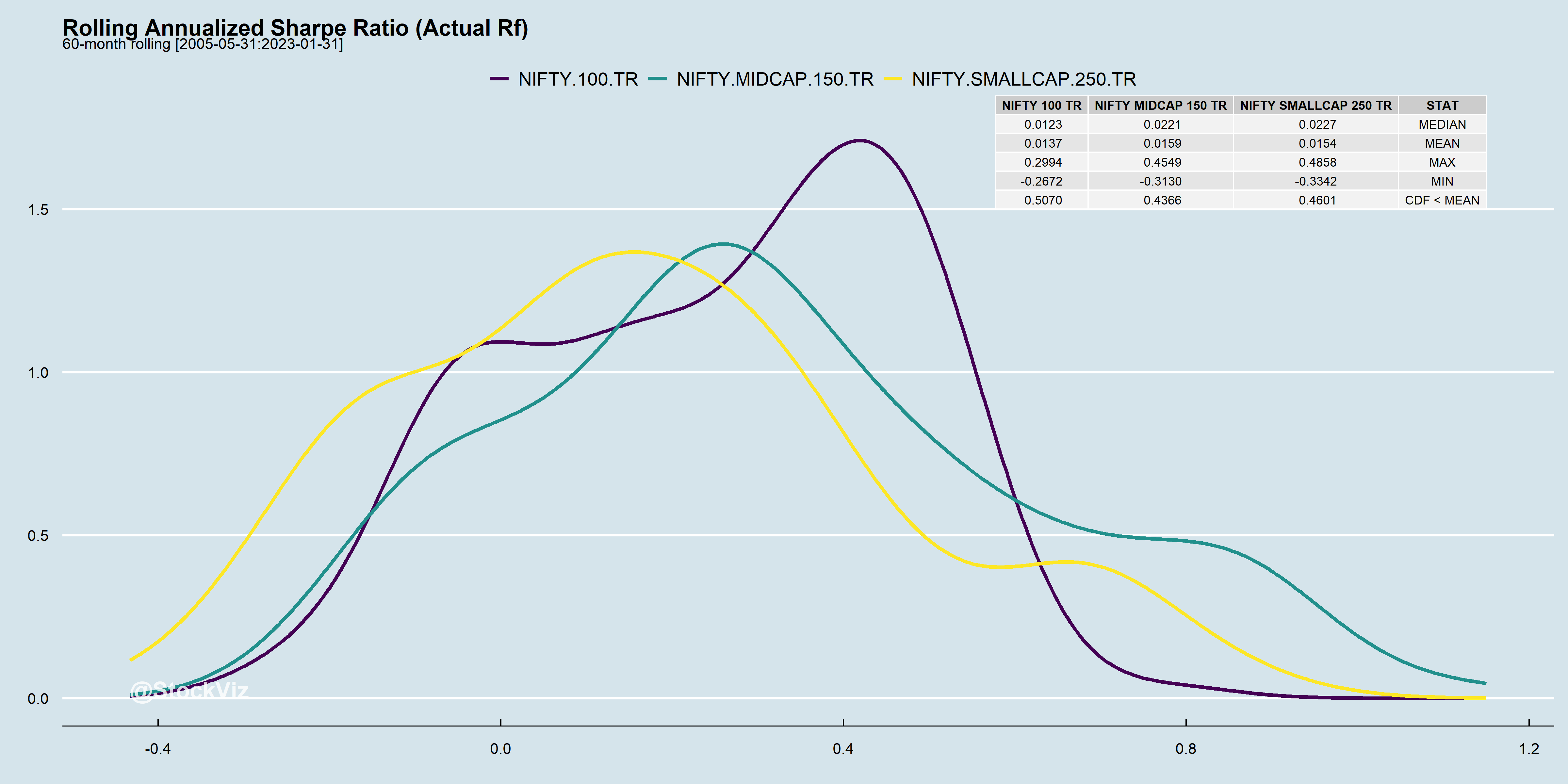

Ideally, you want your Sharpes to be positive and stable. Unfortunately, that is never the case.

During bull markets, Sharpes trend up and reverse course in bears.

At the end of the day, it boils down to whether the returns are worth the risk.

You might very well be trying to catch lightening in a bottle.

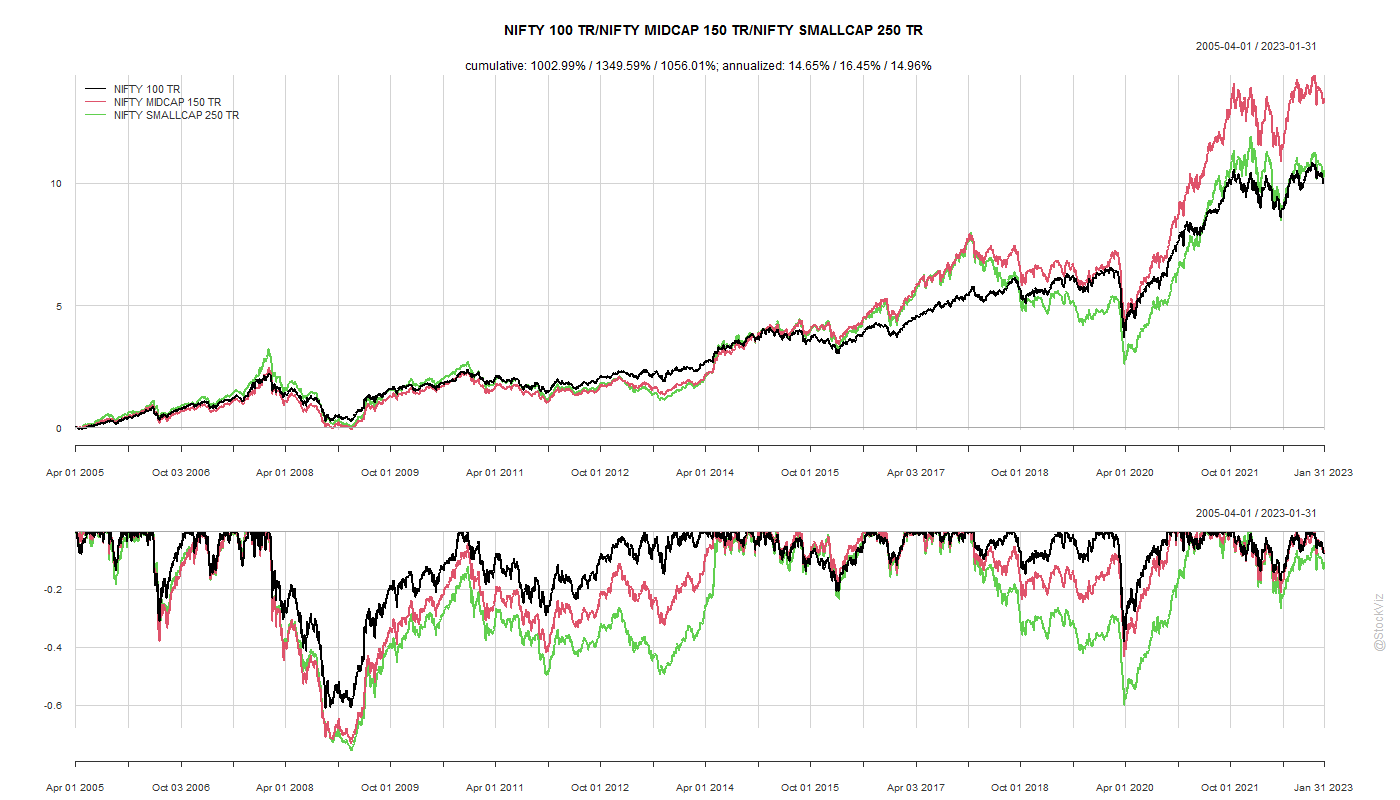

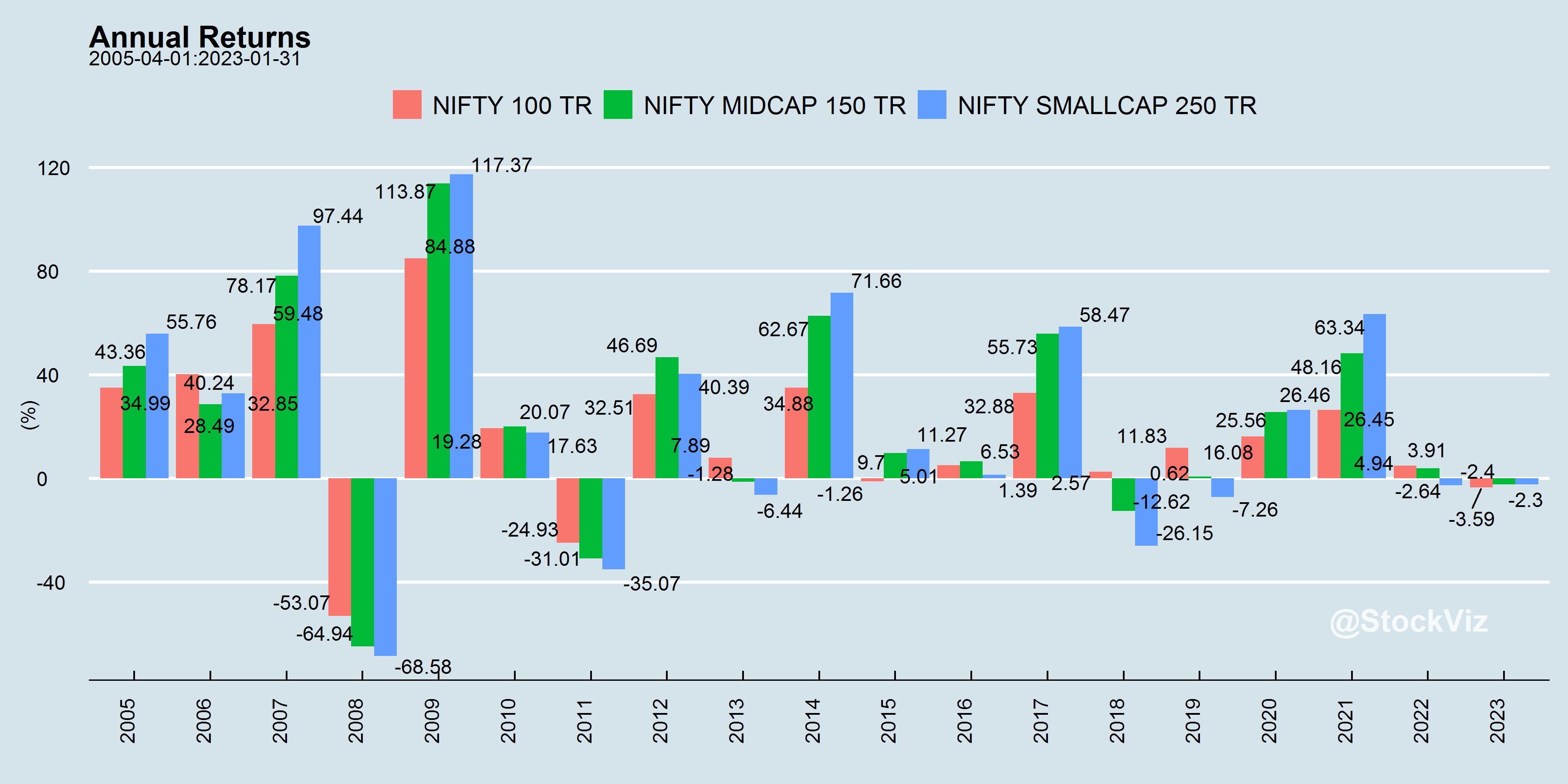

For more index stats, visit our Index Metrics dashboard.

Here are a couple of popular definitions and explanations to get the conversation started:

Investopedia: A hedge is an investment that is made with the intention of reducing the risk of adverse price movements in an asset. Normally, a hedge consists of taking an offsetting or opposite position in a related security.

Varsity: Hedging makes sense as it virtually insulates the position in the market and is therefore indifferent to what really happens in the market. It is like taking vaccine shot against a virus. Hence when the trader hedges he can be rest assured the adverse movement in the market will not affect his position.

The way it is commonly described, hedging is the act of taking offsetting positions against a portfolio to even out the bumps in the market.

The CAPM β

According to EMH, a portfolio’s return could be fully explained by the market (source):

r = rf+ ß(rm – rf) + α

Where:

r = Expected rate of return

rf = Risk-free rate

ß= Beta

(rm – rf)= Market risk premium

If you set the risk-free rate (rf) to zero, you get r = ß*rm + α

Now, subtract away the market from the asset returns and you’ll be left with α.

Basically, a perfectly hedged portfolio will be a completely market neutral portfolio who’s returns will be pure alpha.

The offsetting positions can be taken via futures or options. To keep it simple, we will use futures to illustrate an example.

An Example

It is 2005 and the master analyst that you are, you expect HDFCBANK and KOTAKBANK to be decades long compounders. So, you setup an equal weighted portfolio that has only those two stocks.

If you stayed with this portfolio, then you truly have ??

Even though the annualized returns during the ~15 year period is twice that of NIFTY 50’s, very few investors would have stuck through the 70% drawdown that the portfolio had in 2008 and the 40% drawdown it had in 2020. Not to mention the numerous 20% dips along the way.

The question that hedging tries to answer is as timeless as time itself: Can I have my cake and eat it too?Is there a way to get only the excess returns without the market’s ups and downs?

What is the “market?”

Given that your portfolio consists entirely of banks, what exactly is your “market?” The answer to this question is not trivial.

You could go with the NIFTY 50 index but it has companies from different sectors like oil, metals, IT, etc. How much of an offset do you expect it to provide?

Or, you could go with the NIFTY BANK index. Intuitively, you would expect it to be a better hedge because it is composed almost entirely of banks – just like your portfolio.

Rolling βs

Rolling βs of the portfolio to each index gives us an idea of the appropriate benchmark to use.

What this is telling us, with perfect hindsight, is that the NIFTY BANK index comes close.

Theoretically, Hedging works in Theory

The math checks out. Irrespective of whether you hedge against the NIFTY or the NIFTY BANK index, you end up with much lower drawdowns.

For example, if you hedge against the NIFTY BANK, assuming no frictions and slippage, drawdowns never exceeded 20% and returns came in at a respectable 12% annualized.

Reality Sucks

Hedged portfolios have high Sharpe ratios and look attractive in backtests. However, reality is quite different.

βs are not Stable

The chart of rolling betas of the portfolio over different indices highlight the biggest problem with hedging: the hedge ratio needs to be constantly adjusted because the relationships are unstable.

Adjust it too often, then you lose to transaction costs. Adjust it too slowly, then you are no longer perfectly hedged.

βs > 1

Sometimes, betas can exceed 1. This means that your portfolio is net short during those periods. If the original intent of setting up the portfolio + hedges was to just even out the market fluctuations in a long-only portfolio, then being net-short is something that you may not have bargained for.

Margin requirements Vary

The backtest presented above allocates 90% to the cash (long-only) part of the portfolio and 10% towards margin requirements. However, during periods of market stress, brokers are known to hike margins to protect themselves. This might end up putting you in a position where you will need to pare back some of your long-only exposure to raise funds to meet the increased margin requirements. Basically, selling the dip.

Markets have a Positive Drift

Over long time horizons, markets typically have a positive drift. With a hedged portfolio where you are short the market, you are betting that this drift is overshadowed by volatility and portfolio alpha. It may very well be true, but you are betting against the winds.

Who should Hedge?

Leveraged Investors

Hedging doesn’t make sense for long-only cash portfolios. If you are a CNC (Cash N’Carry) investor, then you are better off de-grossing (reducing overall exposure or positions) and focusing on diversification rather than trying to hedge your portfolio.

Investors who employ leverage, however, should hedge. For example, if you were to take levered positions in HDFCBANK and KOTAKBANK through futures, then it makes sense to try and hedge out the market risk. Futures have 5x leverage built in, so it has the potential to boost your CAGR, as long as you can meet the mark-to-market during the 20% drawdowns.

Tactical Positioning

Some investors may prefer to hedge only when they expect market volatility. In our introduction to Tactical Allocation, we touched upon how we can use moving averages to shift between stocks and bonds. Instead of trading in-and-out, investors might prefer to add a hedge instead.

Needless to say, we are not big fans of investors trying to time the market like this.

Conclusion

Hedging makes sense if you are a leveraged investor. Given the costs, complexity and performance drag involved, it doesn’t make much sense for cash investors to hedge.

Looking for a sensible way to invest? Here’s how to get started.

Volatility measures changes in price. Price is a measure of sentiment. Volatility measures changes in sentiment.

Most of the time, it is impossible to tell the difference between the two.

Exhibit A: AIG

American International Group, AIG, had enjoyed a AAA rating for 22 years and had been just one of eight US companies to hold the top rating from both S&P and Moody’s.

As mortgages started to go bad, AIG stock began its long journey to zero from July 2007. During that time, a majority of investors thought that every dip was a buying opportunity.

The problem with trying to be too smart about “volatility” vs. “risk” is how do you know what is priced-in vs. what is panic-selling?

If you are going to panic, panic early!

Panic is good only if you panic early, and as a trader the first thing you learn is to panic early. – Nassim Taleb

Discretionary investors wax eloquent about the strength of their conviction. Having done their homework, they claim, they have the “diamond hands” to hold onto their investments during bouts of volatility and to buy the dip.

However, these narratives are heavily driven by survivorship bias. You will never hear about conviction and diamond hands from investors who bought the dip in Bear Stearns, Suzlon or Kingfisher Airlines.

As an investor, you get no points for being a hero. If there is a whiff of something unpleasant, it is better to get out of an investment entirely, take a beat, re-evaluate, do a relative-value assessment to figure out how it compares to other opportunities and only then decide whether you want add it back to your portfolio.

Exit first. Ask questions later.

Compounding works both ways

Losers average losers – Paul Tudor Jones

We have all seen the Whatsapp forward about compounding: (1 + 0.1)^10 = 2.59 i.e., 10% compounded over 10 years will turn every rupee into 2.59 rupees. Rarely do you see the reverse: a 50% loss requires a 100% return to get back to even.

If you care about compounding your portfolio, stop compounding your losses!

Investing is risk management

… and risk management is not free.

Most investors focus on the glamor part of the process: scuttlebutt stock-picking to find the rare “hidden” gem that will 100x in 5 years. They would have better odds buying lottery tickets instead.

There are plenty of investors who became millionaires simply by grinding away at harvesting risk premia and managing risk.

Avoid blowing yourself up and allow statistics to do play out.

The only investors who shouldn’t diversify are those who are right 100% of the time. – Sir John Templeton

There is a big difference between the advice professional investors give to other professional investors (like the ones above) and the advice that savers need to follow. The media often focuses on the former because it is exciting and there’s always something new whereas the later is mostly timeless and boring.

The media’s sampling and survivorship bias ensures that only large, successful, telegenic professional investors get the spotlight. And media’s short attention span ensures that most of them are never held to account for their pontifications. As far as the media is concerned, the only crime is to be boring.

The tragedy is that there are only so many ways in which you reframe “save into a diversified portfolio by dollar cost averaging into a low-cost, broad-based equity fund and a short-term bond fund.” So it is guaranteed to never get the airtime in proportion to how important it is.

— Dividend Growth Investor (@DividendGrowth) April 22, 2021

Diversification means that your incremental dollar is buying the asset that has not appreciated as much as the other. For example, if you keep a static 50/50 equity/bond portfolio and equities are up 10% but bonds are up 2% then the next dollar you put into that portfolio is going to buy more of the bonds and less of equities. This is where the Risk Management is Not Free rule kicks in: diversification is anti-momentum, a premier market anomaly. By diversifying and rebalancing, you are not maximizing your portfolio returns but minimizing volatility in a cost-effective way.

Remember, that in the end, we are all short volatility.