Benjamin Graham described Mr. Market as a manic-depressive, randomly swinging from bouts of optimism to moods of pessimism. While equities and markets exist in perpetuity and can create wealth in the long-term, most investors don’t have the luxury of remaining invested forever. We have extensively discussed the problem of sequence-of-returns risk for investors who have finite investment horizons in our Free Float newsletters (Intro.)

A bigger problem than sequence, is the severity of low-probability events. Also called fat-tails or black-swans.

NIFTY 50 Monthly ReturnsNIFTY MIDCAP Monthly ReturnsNIFTY 10-year government bond Monthly Returns

While an investor can mitigate an unfortunate sequence of returns through diversification, a market tsunami can hit all assets at the same time.

US/India Equity and Bonds during the Corona Panic

The charts show how years of returns can get wiped out in a month in the markets. While investors mostly focus on the average, the tails end up dictating their actual returns.

While using traditional statistical tools like average, std-deviation, correlation, etc. makes sense 99% of the time, they breakdown during that 1% of the time where an investor needs them to hold. This is the main motivation behind studying tail-risk events.

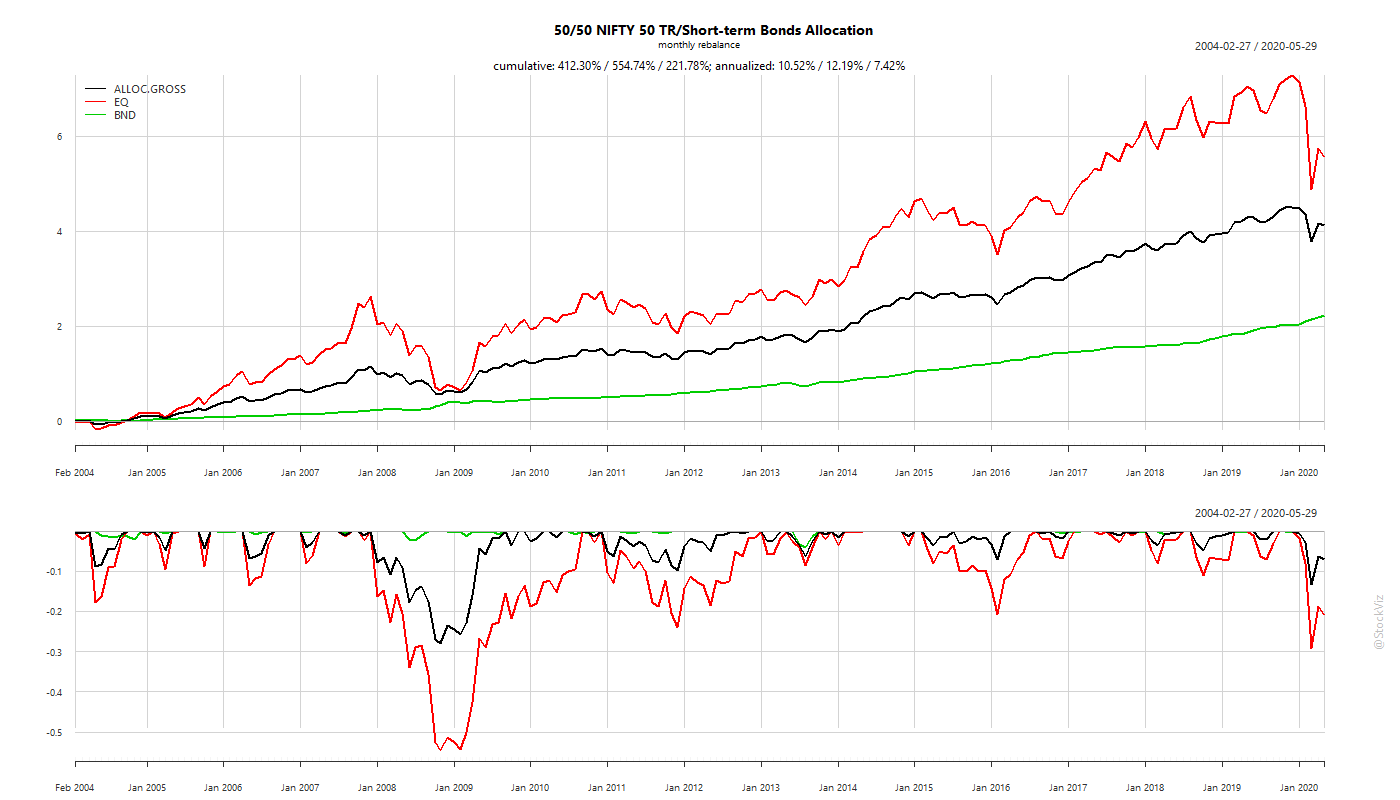

Our first post discussed one of the biggest risk that investors face: sequence-of-returns risk. One way to mitigate this is through asset allocation. You can just put half your investments in equities and half in bonds to reduce your over-all risk. An alternative is tactical allocation. In tactical allocation, you use a signal, like an SMA (Simple Moving Average) or equity valuations to switch between equities and bonds. Here, at any given point in time, you are fully invested in one asset class.

So, which one is “better?”

The answer is, “it depends!”

It depends on the investor’s tax slab and whether it is going to be a lump-sum investment or a SIP. For lump-sums, investors are better off with a tactical approach (bonus if you are in a lower tax slab.) For SIP investors, static allocation makes more sense because you can maintain proportions without selling the over-allocated asset. And, surprisingly, the frequency of re-balance did not matter for static allocation.

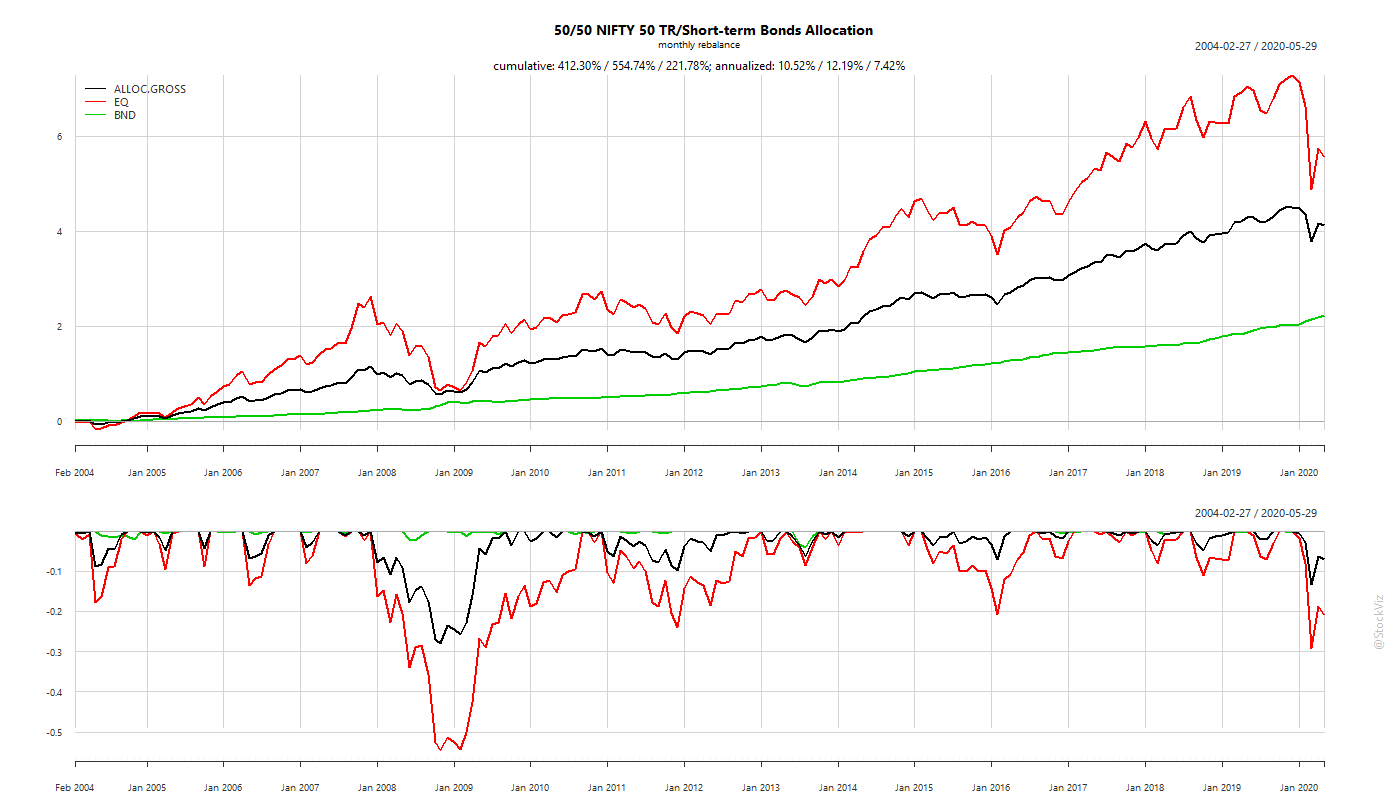

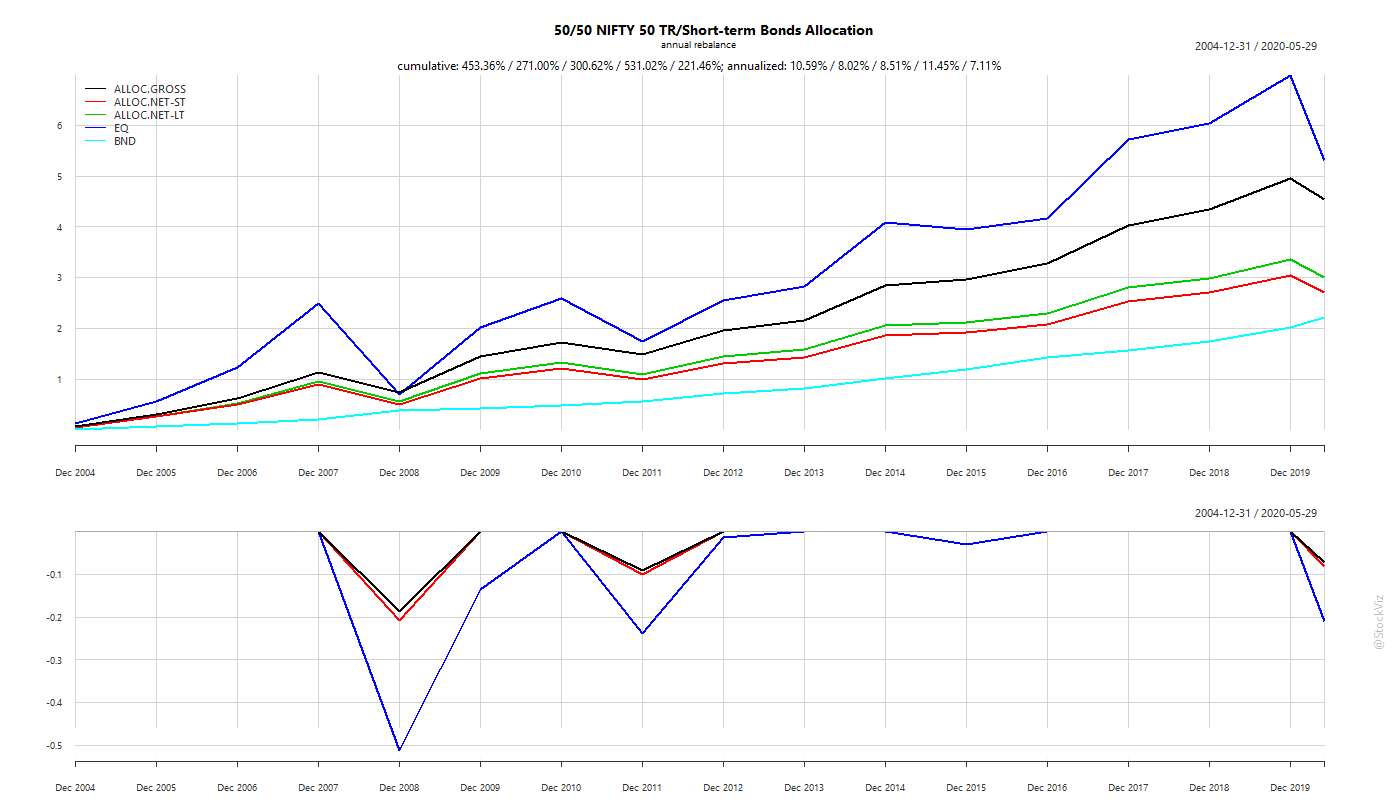

Re-balance Frequency for Static Allocation

Our back-test shows that there is no difference to overall returns between monthly and annual re-balance frequencies. Focus on the black line on the following charts.

Monthly re-balance:

Annual re-balance:

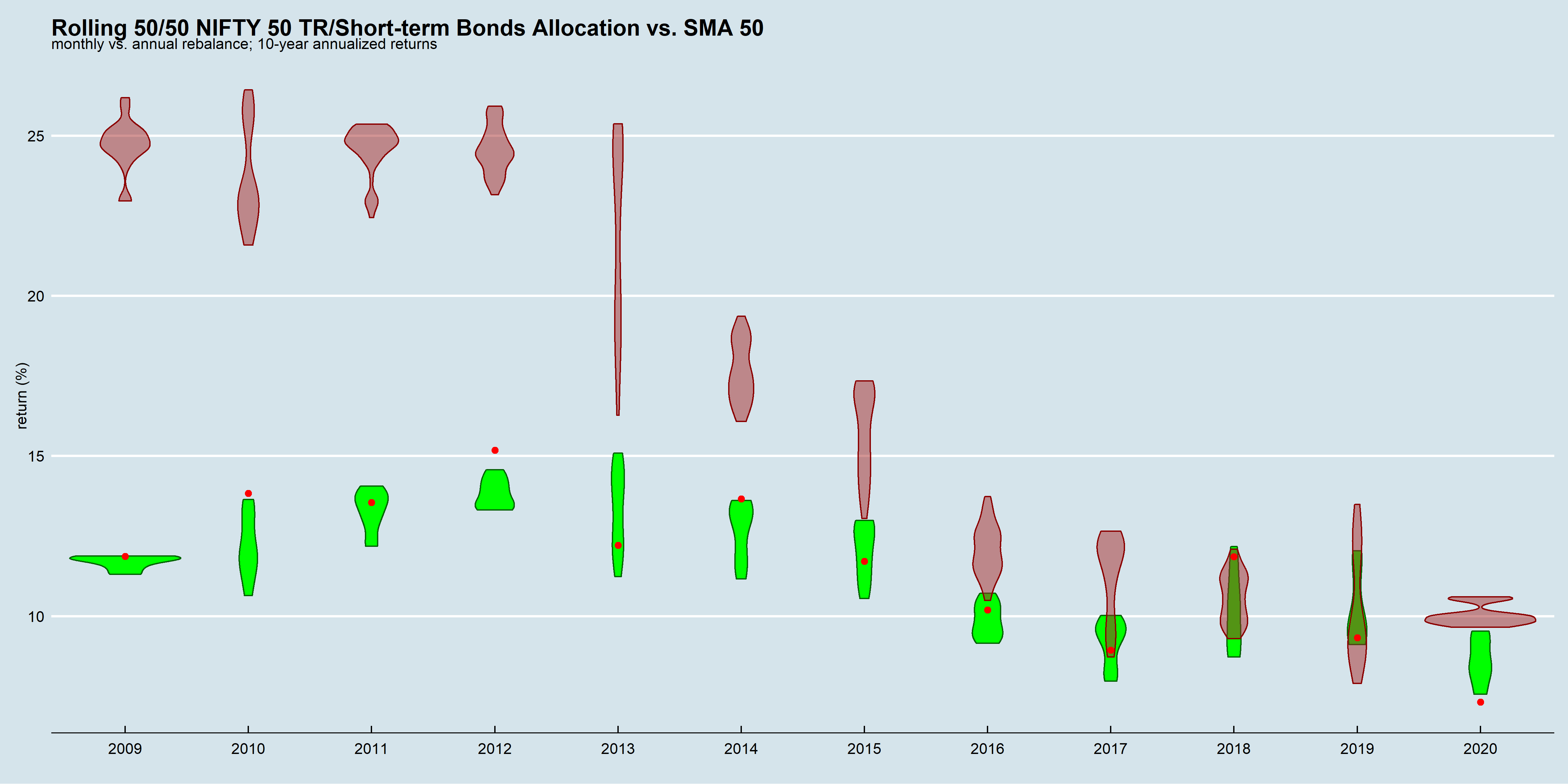

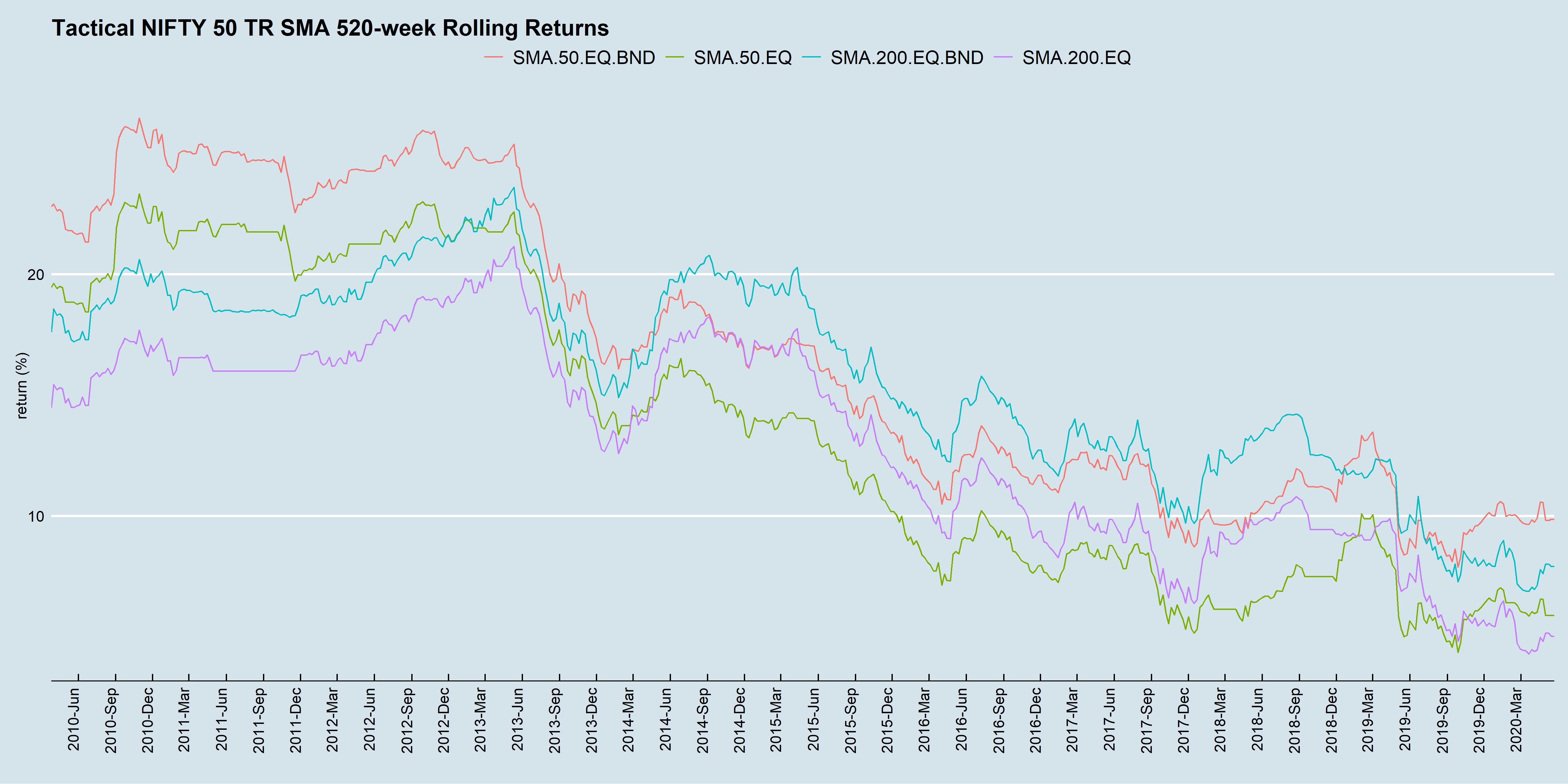

Static vs. Tactical – Rolling 10-year Returns

Static allocation returns have been converging with those of the tactical strategy.

Red dot: static 50/50 allocation, annual re-balance

Brown: 50-day SMA, weekly sampling

The above chart reinforces a couple of points we made earlier:

Sequence-of-returns risk is real.

Large impact of when you start and stop your investments (“luck” factor,) is real.

Excess returns in a back-test could be because of high transaction costs or lack of liquidity. In such cases, expect excess returns to diminish as those factors improve.

Barring a couple of instances, annually re-balanced returns were within the range of those that were re-balanced monthly.

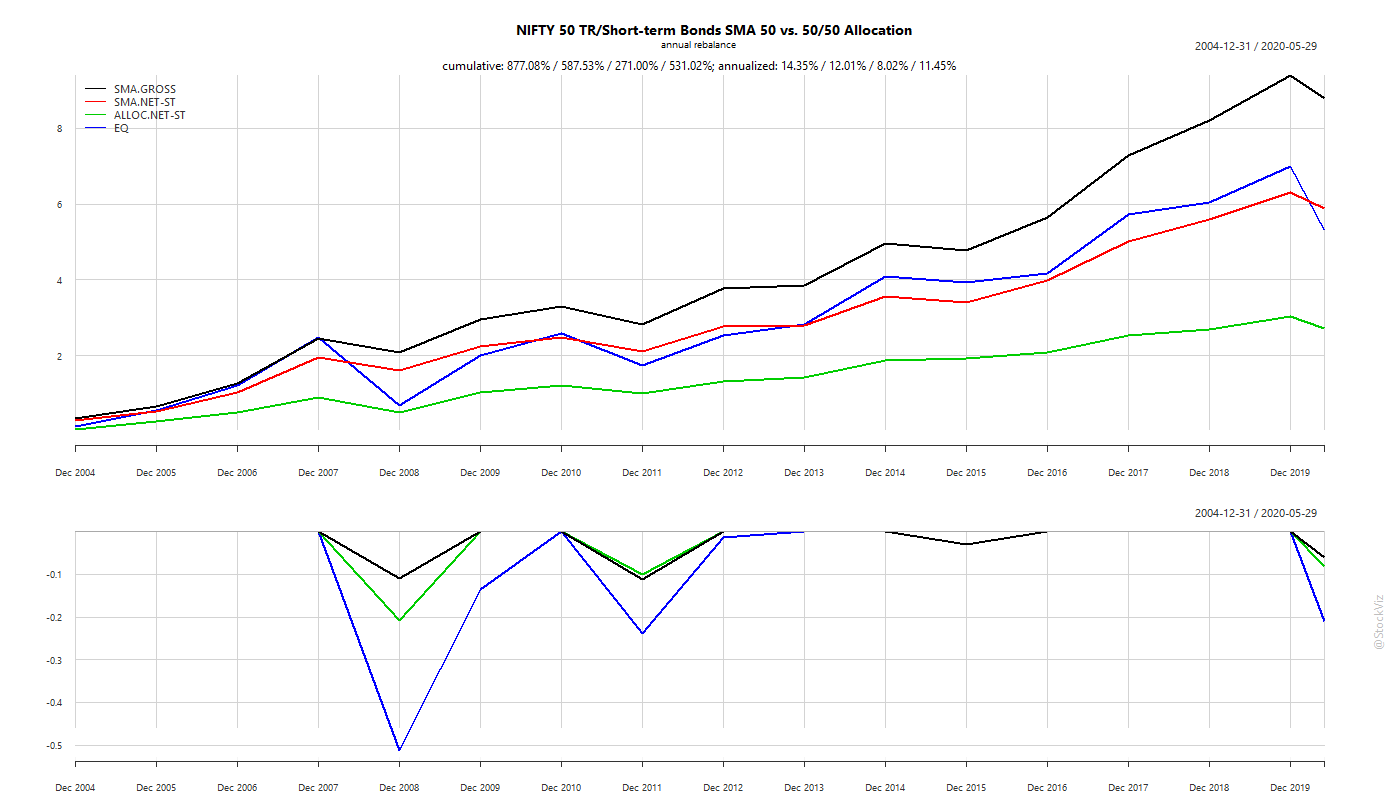

Tax impact

If you do a worst-case tax impact analysis on both static vs tactical (SMA) strategies, over the long-arch of time, tactical wins. In the chart below, static allocation is the ALLOC.NET-ST (green) line and tactical is the SMA.NET-ST (red) line.

However, if you are a SIP investor, then you don’t need to sell the over-allocated asset under a static-allocation setup – you could just buy the under-allocated one till it falls back in line. So, if you plot the after-tax returns of tactical allocation with pre-tax returns of static allocation by year:

Years 2011 through now, there is hardly any difference between them. They both turn in annualized gains in the low 7% range – adding about 1.25% over an all equity portfolio.

Summary

For lump-sums, choose tactical. For SIP choose static allocation.

Don’t ignore bonds. There are periods where a bulk of the returns are driven them.

Don’t ignore the role of taxes in DIY. For example, a mutual fund that wraps the SMA strategy would enjoy a 2+ % boost in annualized returns.

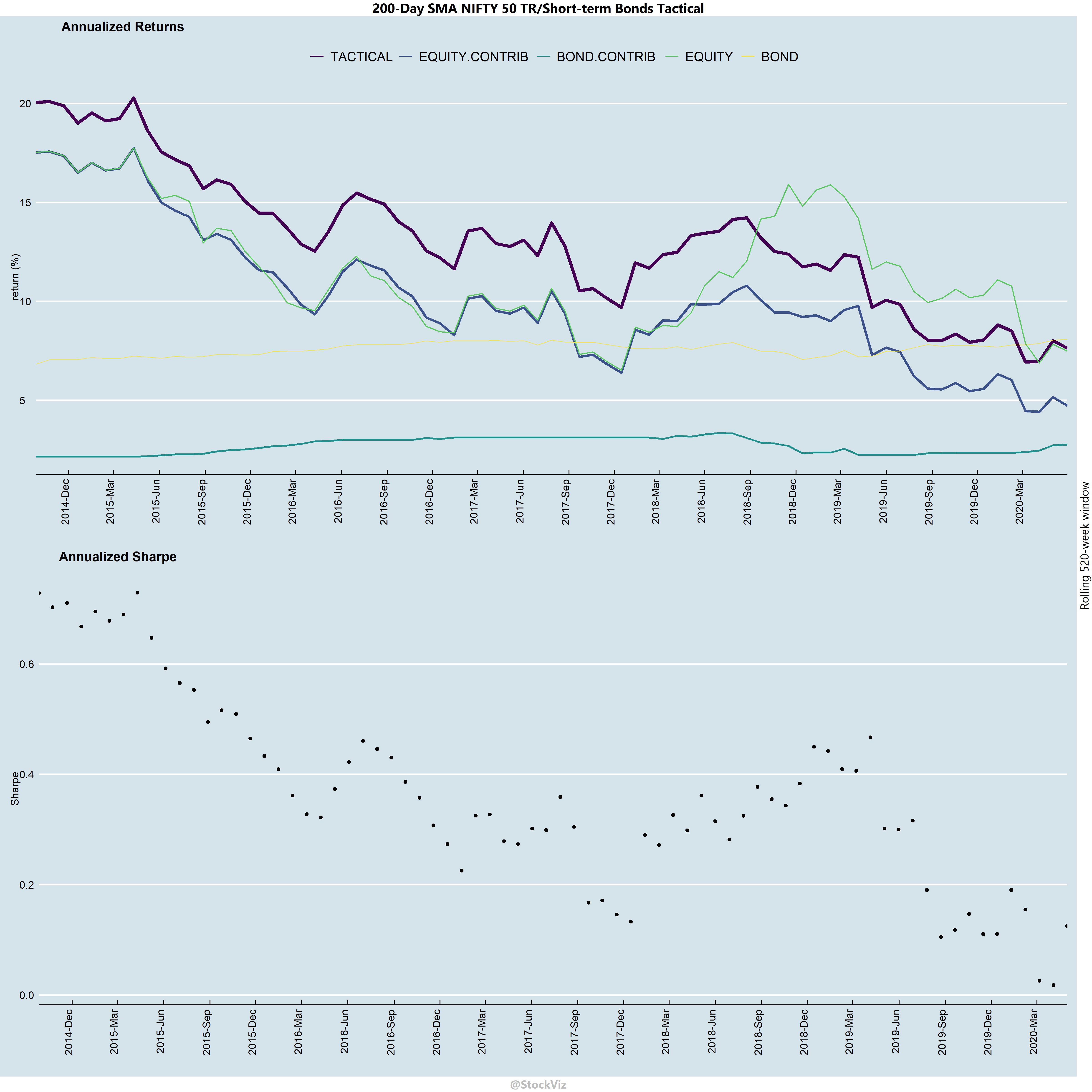

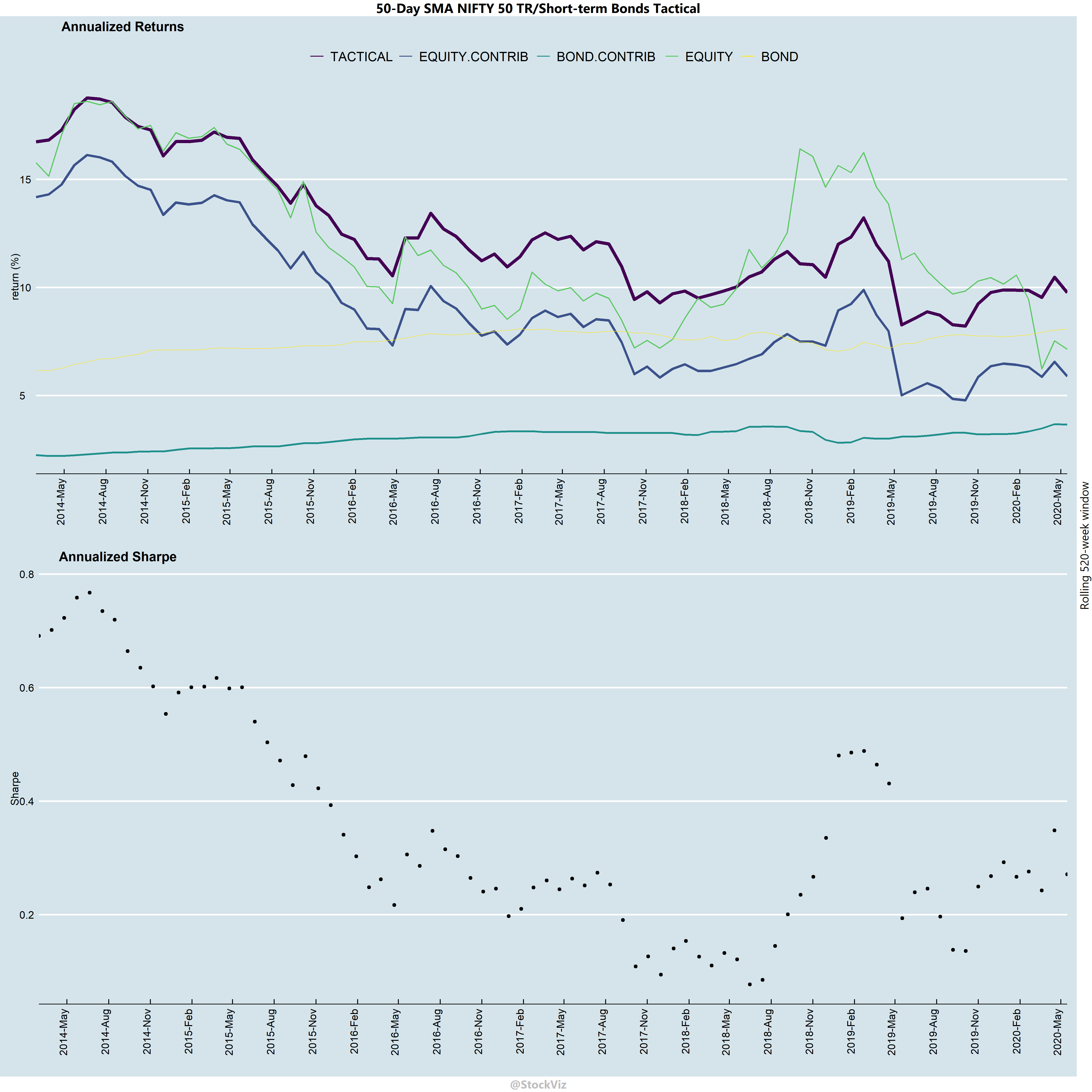

We introduced tactical allocation in our Free Float newsletter last week. We saw how, by using a simple moving average to toggle between equities and bonds, one can reduce drawdowns in their portfolios. In the ensuing discussion, we mentioned how excess-returns found during back-tests could be an artifact of illiquidity and high transaction costs of the markets in the past. It is not like people who traded markets before us were dumb (or somehow, we suddenly added 50 IQ points in the last 20 years.) There has to be a reason why the money was left on the table.

Indian markets have seen significant changes over time. It has got more deeper and wider with better liquidity, lower transaction costs and higher levels of automation. One way to gauge the efficacy of strategies is to use a metric like Sharpe or Information Ratio over rolling-windows through time. Also, the drivers of total returns in allocation strategies will be different across different time-horizons leading to different tax liabilities. It is useful to decompose returns to handicap them from a tax angle.

200-day Tactical Strategy50-day Tactical Strategy

There are quite a few time-periods where tactical allocations will under-perform buy-and-hold equities.

Over a 10-year horizon, on an annualized basis, bonds have contributed about 1-4% to over-all returns.

Sharpes have been falling through time. One should expect this strategy to attenuate further.

Bonds have a bigger say in determining over-all returns in low equity return environments. So, use both assets!

Bond returns have been less volatile that those of equities’. However, that doesn’t mean that have been constant through time.

With and without bonds

In high equity-returns environments, bonds are usually an after-thought. However, running these strategies “equities-only” is ill-advised. In the chart above, returns in the recent 10-year periods have been palatable only because of the returns contributed by bonds.

Our personal experience has been that when equities drawdown, investors switch over to tactical strategies, only to abandon them once stocks recover. Thus, leaving their downsides exposed during the next drawdown; ensuring that they end up with the worst of both worlds.

Excess returns aside, SMA strategies are also useful in managing risk. With lower risk, one can employ a bit of leverage to boost returns. We have done deep-dives into variations of these strategies in the past. Interested readers can have a look at our SMA Collection.

Sequence Risk (sometimes called sequence-of-returns risk) is the effect that the order of returns has on a portfolio.

For example, say you look at NIFTY and find that it gave negative 10% returns 4 years out of 10, and the rest of the years it gave positive 10% returns. You want to be invested for 5 years, so you expect 2 of those years to be negative. Sequence risk means that it is possible that you could have all of those negative 4 years during the 5 year period that you have invested.

The order in which losses occur impacts the portfolio’s terminal value

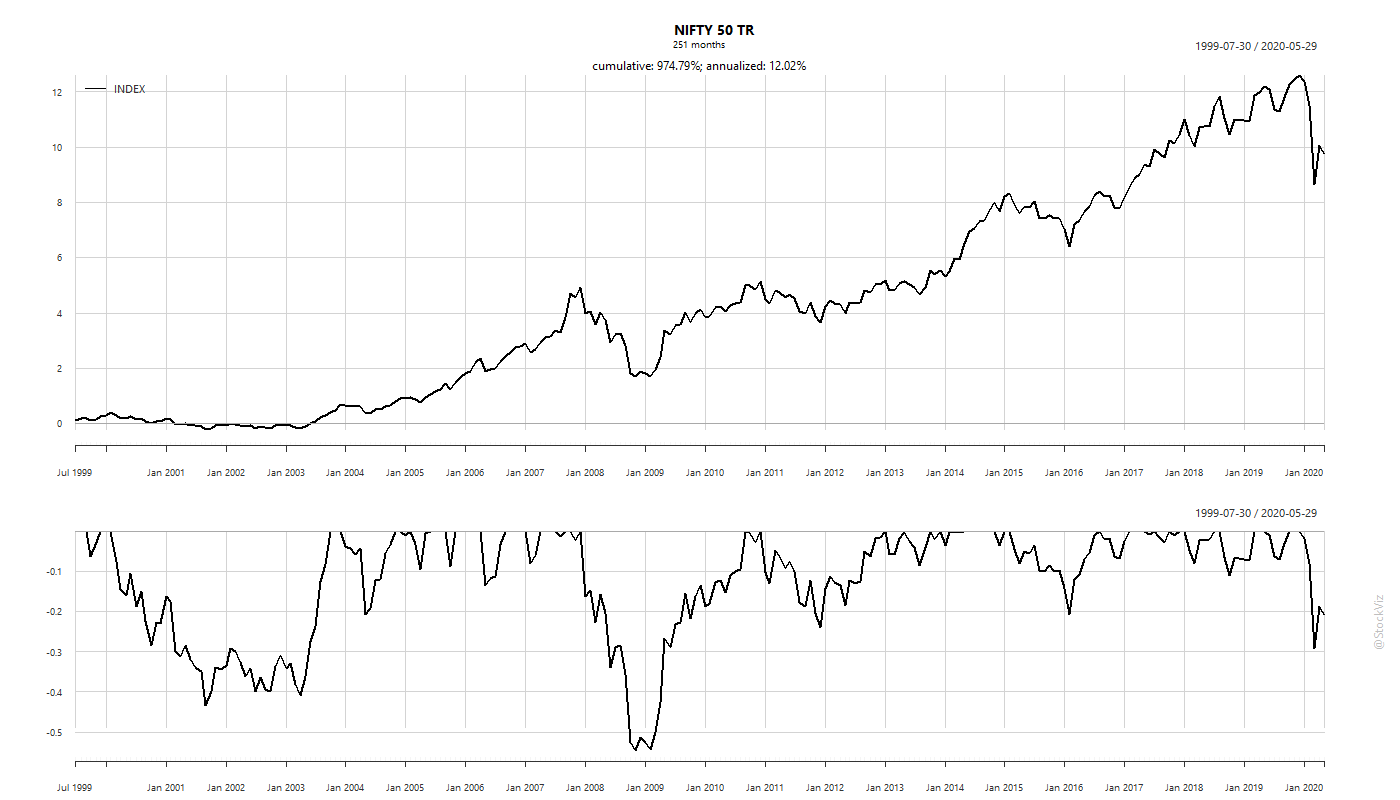

The annualized return of the NIFTY 50 TR index, since inception through May-2020, is roughly 12%. However, it has not been without periods where it was down over 50%.

NIFY 50 TR cumulative returns since inception

The lower part of the chart shows the drawdowns that have occurred in the past. Sometimes, it has taken years to recover from losses. The problem is that most investors have a pre-defined time-frame in mind. They want to be invested, say, for 10 years. Not “forever.” This is where sequence risk becomes a problem.

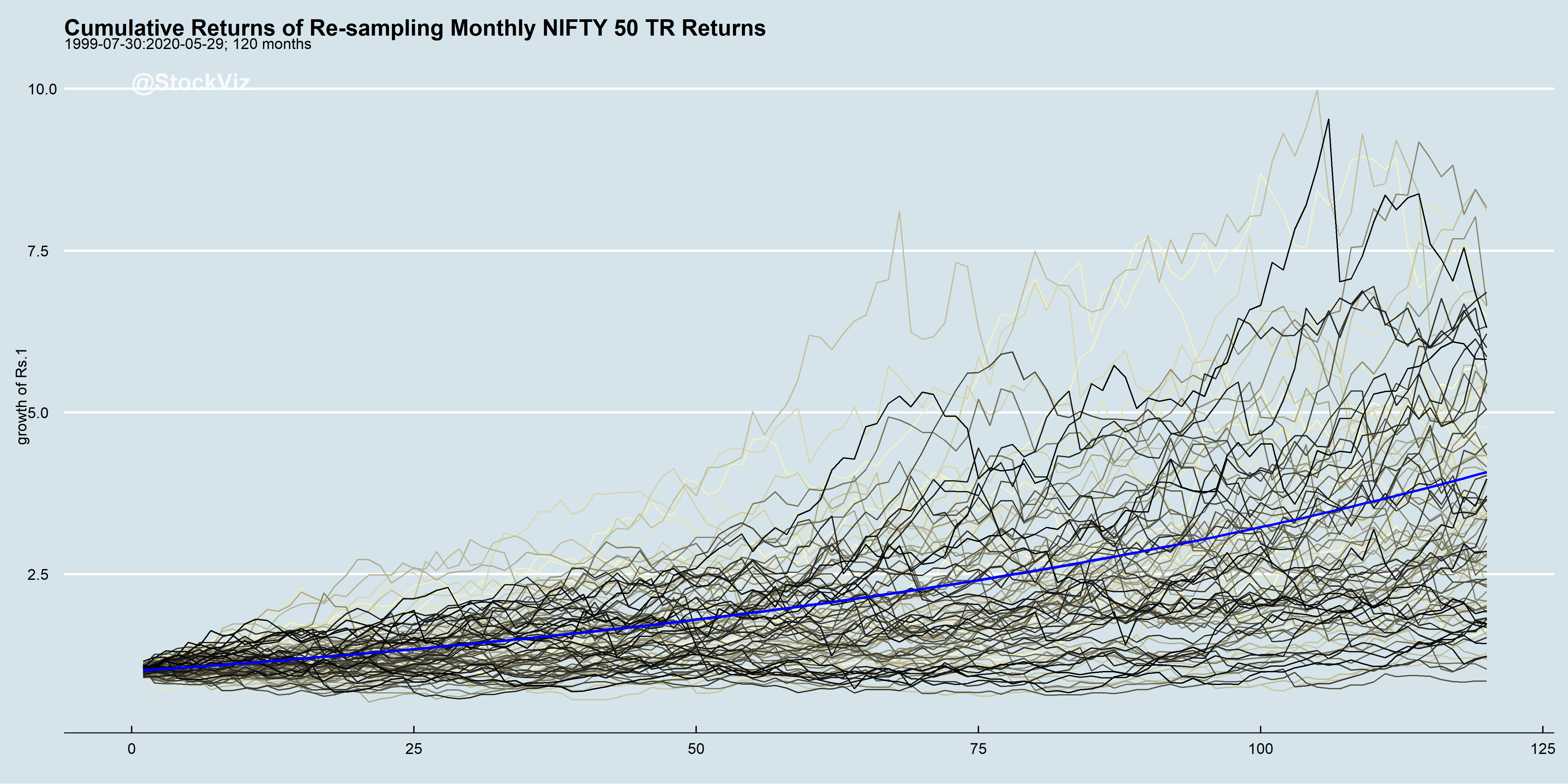

For a 10-year period, if you re-sample the monthly returns of the NIFTY 50 TR index and re-construct a return time-series, say, a 100 times, and plot the cumulative returns of each, it looks something like this:

The blue line is the “average” monthly return compounded for 10-years

Put another way, there is a non-trivial chance that an investor could end up with negative returns in a given 10-year period even if NIFTY’s return distribution did not change.

So, what is an investor to do? There are two approaches that have known to work:

Diversification. Allocate to non-correlated assets.

Get Tactical. Markets are known to trend. Try and preemptively exit from assets who’s prices are trending down.

There are a million different ways to skin each of these approaches. The simplest one is to add bonds to the portfolio.

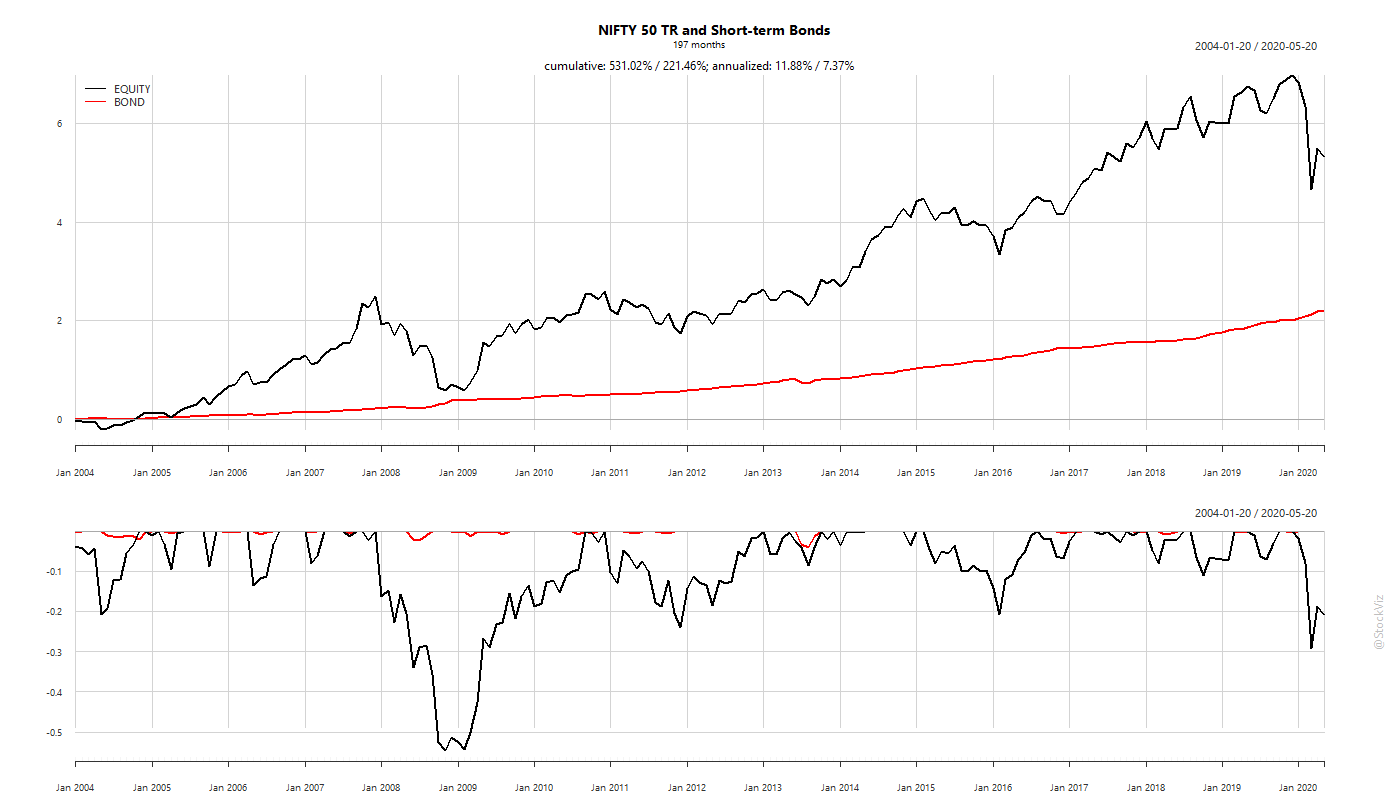

NIFTY 50 TR and 0-5yr TRI

Bonds, especially sovereign bonds (issued by stable countries, of course) have very low drawdowns. So when you combine it with equities, you end up with a lot less sequence risk than pure equities.

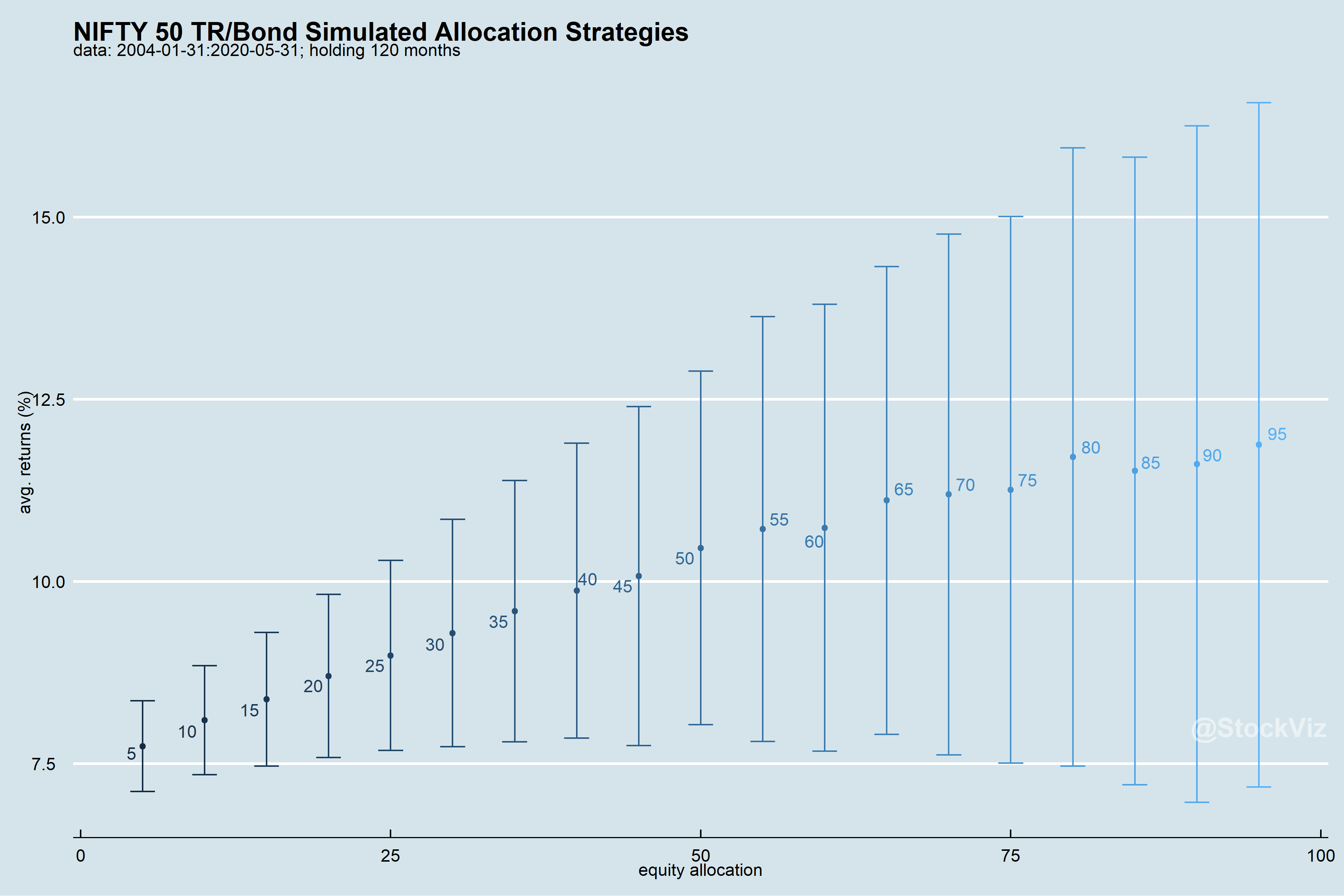

If you simulate different proportions of equities and bonds and plot them along with their standard deviations, you’ll get an idea of where to trade-off stability with returns.

Trade-off between risk and returns

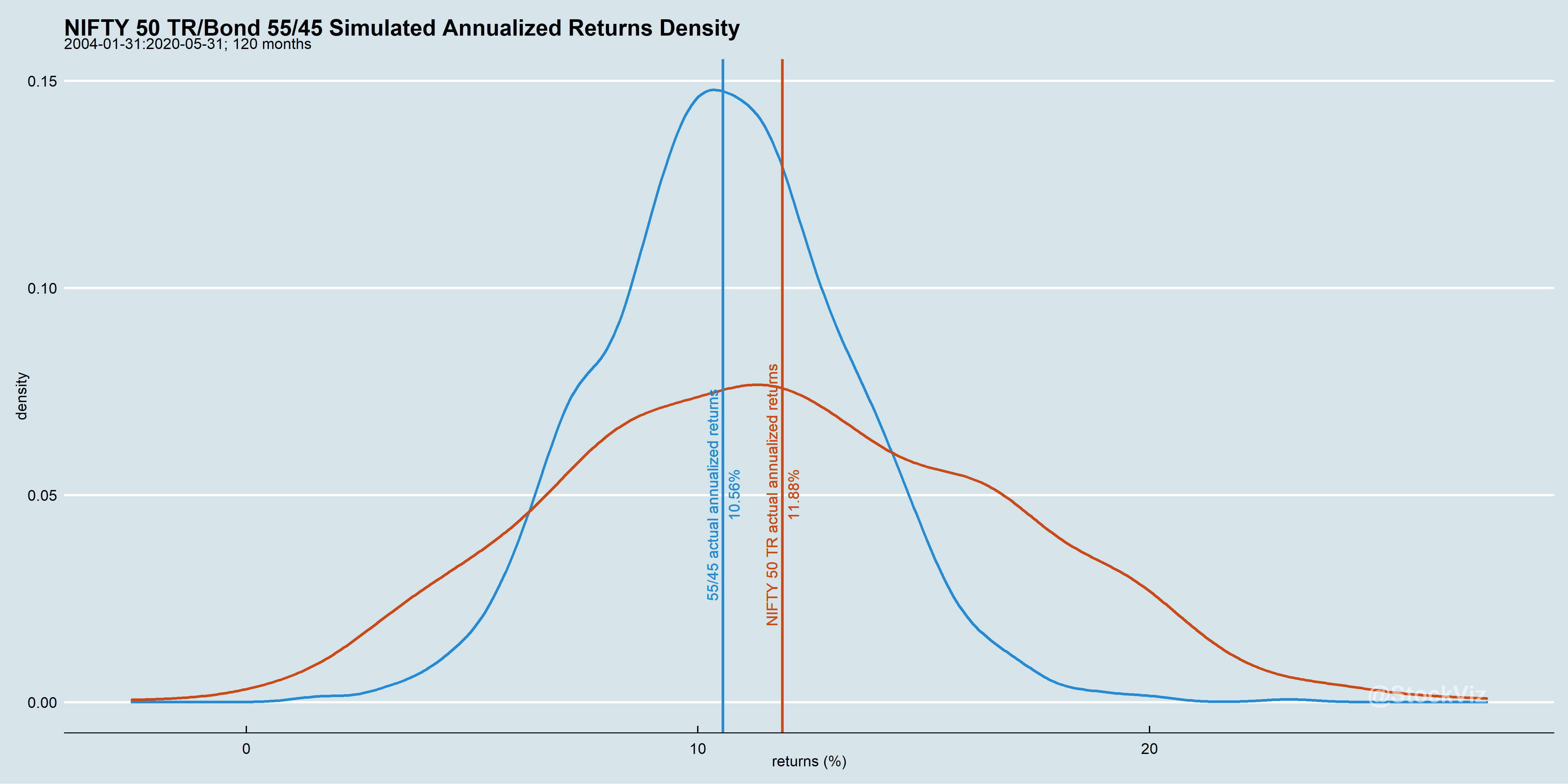

Let’s say that the sweet-spot is equity/bond ratios with avg. returns more than 10% but lower-bounded at 7.5%, you get 45/55, 50/50 and 55/45 as ideal allocations. While a 60/40 equity/bond allocation is the go-to for most advisors, there is no reason why it can’t be a more conservative 45/55.

Cumulative returns of different allocation ratios

Note the lower drawdowns of diversified portfolios. While the equity-only portfolio would have had an annualized return of 11.88% during the period, diversified portfolios ranged from 10.10% – 10.56%. The trade-off is that diversified portfolios have vastly less sequence risk.

The left-tail has been flattened while returns are now clustered more towards the average

Diversification changes the shape of the return distribution so that an average investor has a greater probability of experiencing average returns.

Read more about portfolio allocation across different assets here.

There is absolutely zero stability in metrics used to analyze mutual fund performance. Whether it is alpha, beta or information ratio, they all vary over time and across market environments. Using them to pick the next “winning” fund is pointless. They are, at best, a measure of what happened in the past.

Sharpe Ratio was one of the first attempts at quantifying investment returns. It is simply the average return divided by the standard deviation of returns. However, the approximation that returns are normally distributed makes it unsuitable for comparing across different investments/strategies.

But what if you kept the basic assumption that returns are normally distributed and introduced adjustments for kurtosis and skewness? One such approach is Marcos López de Prado’s Probabilistic Sharpe Ratio (pdf.)

Let’s say the calculated (historical) Sharpe Ratio of the investment is SR^. The benchmark has a Sharpe of SR*. Then, the Probabilistic Sharpe Ratio, PSR(SR*) = Prob[SR <= SR^]

Intuitively, PSR increases as the standard deviation of SR decreases, increases with positively skewed returns and decreases with fatter tails.

So, given investments with similar Sharpe Ratios, invest in the one that has a higher PSR.

We took two large-cap mutual funds that have been around since 2006, the NIFTY 50 TR index and a basic SMA-50 long-only strategy over NIFTY 50 TR to see how the ratios shake out.

Probabilistic Sharpe Ratio

From what we see here, both from a historical Sharpe as well as PSR, given a choice between MF1 and MF2, one would pick MF1.

Our take: PSR is valuable in cases where you have to choose between multiple strategies with equally attractive Sharpe Ratios since it gives a confidence level around that number.