Our Volatility and VIX Collection had some charts that were more than two years old. This post updates some of those charts and will re-create them more often.

Volatility can be measured in a number of ways and its profile changes based on the look-back period. The parameters are selected based on what the volatility estimate is used for. Moreover, no two indices exhibit the same profile – traders need to be vary of transplanting trading strategies that work for one market into another.

Historical volatility density plots

20-day historical volatility density plots

20-day historical volatility plots

US S&P 500

Japanese Nikkei 225

Indian NIFTY 50

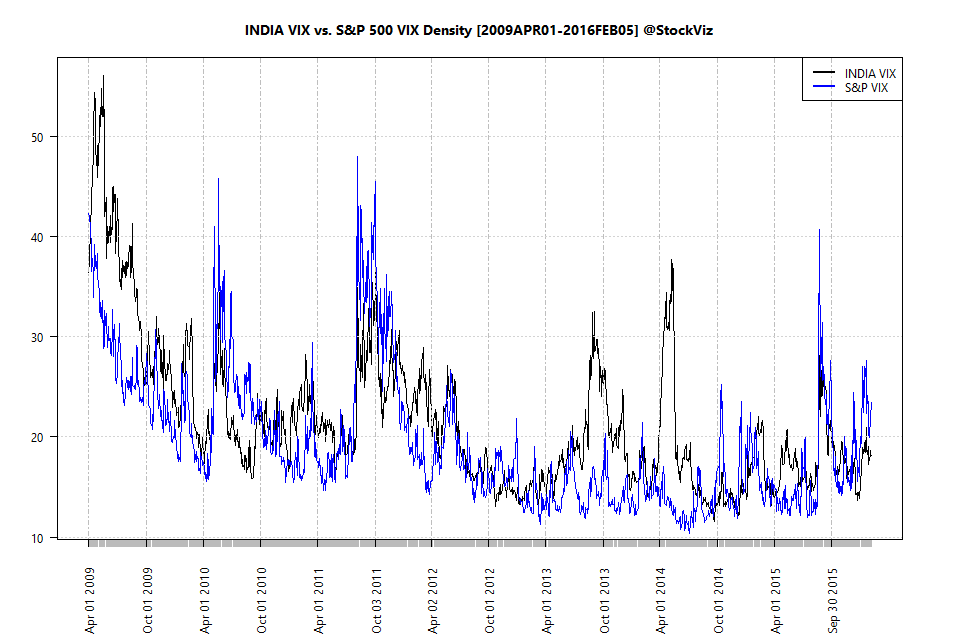

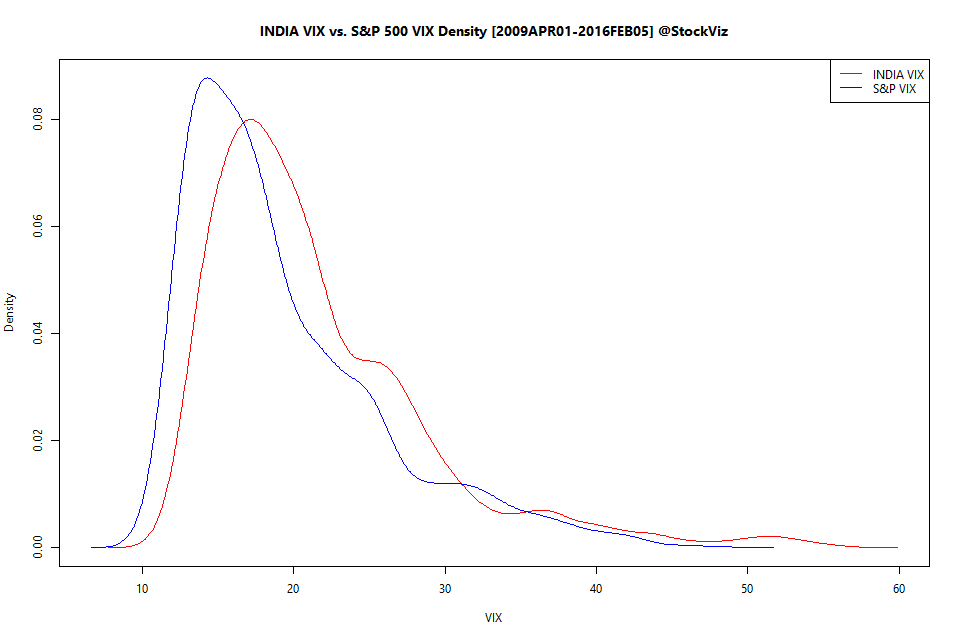

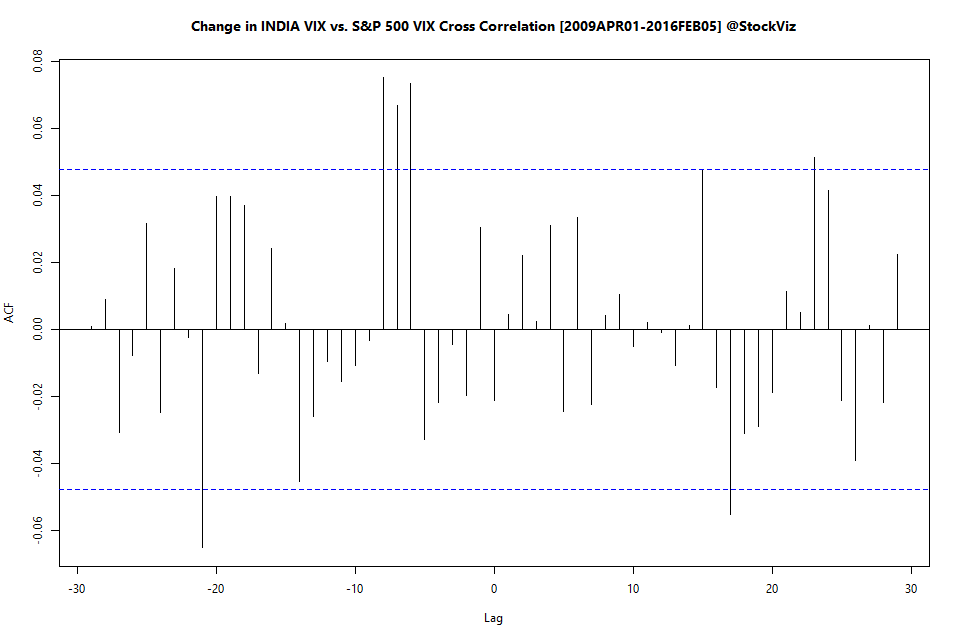

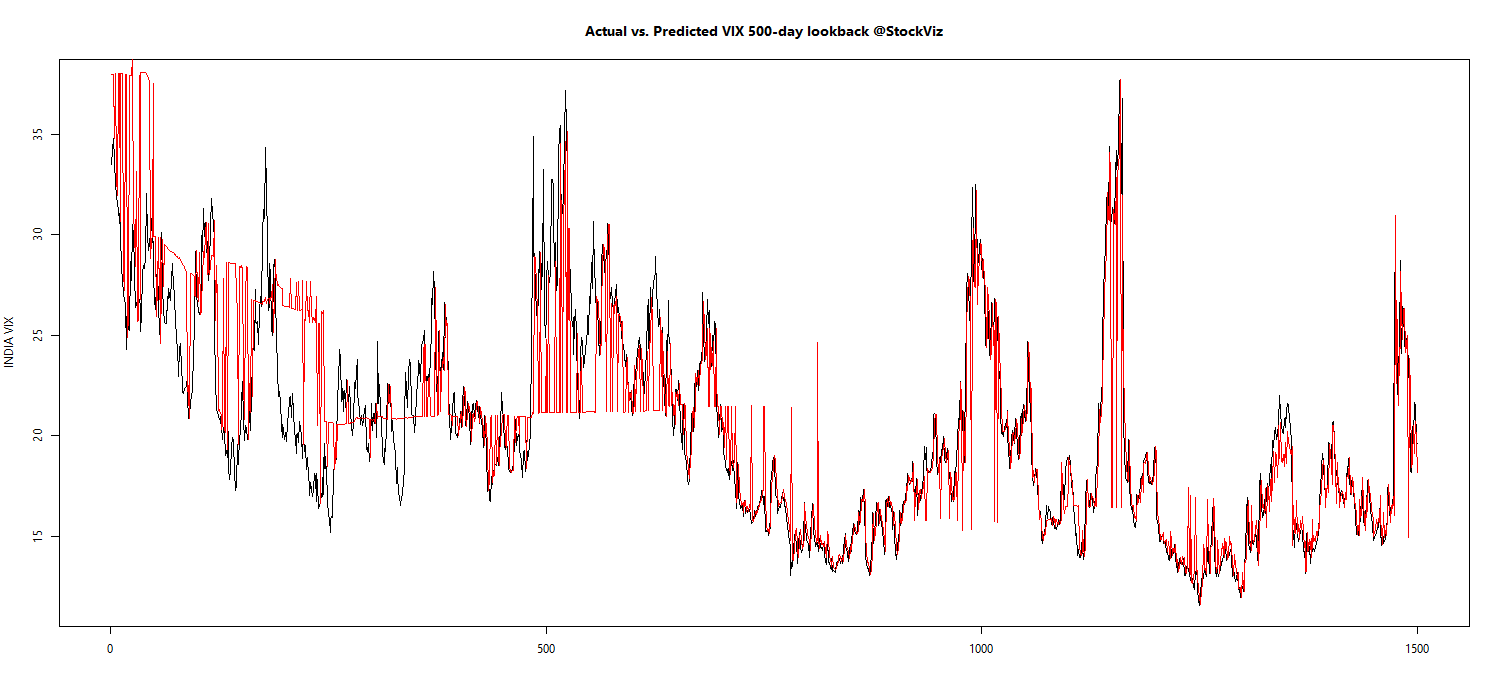

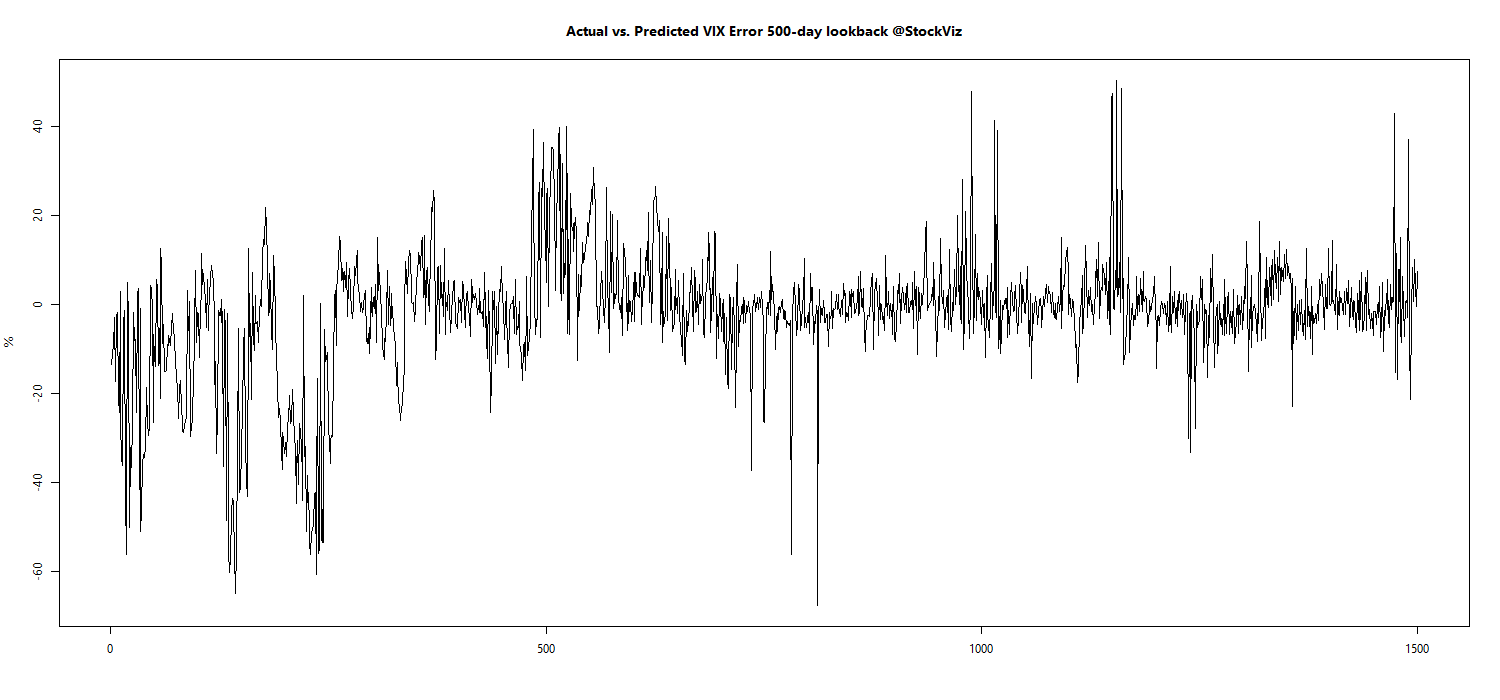

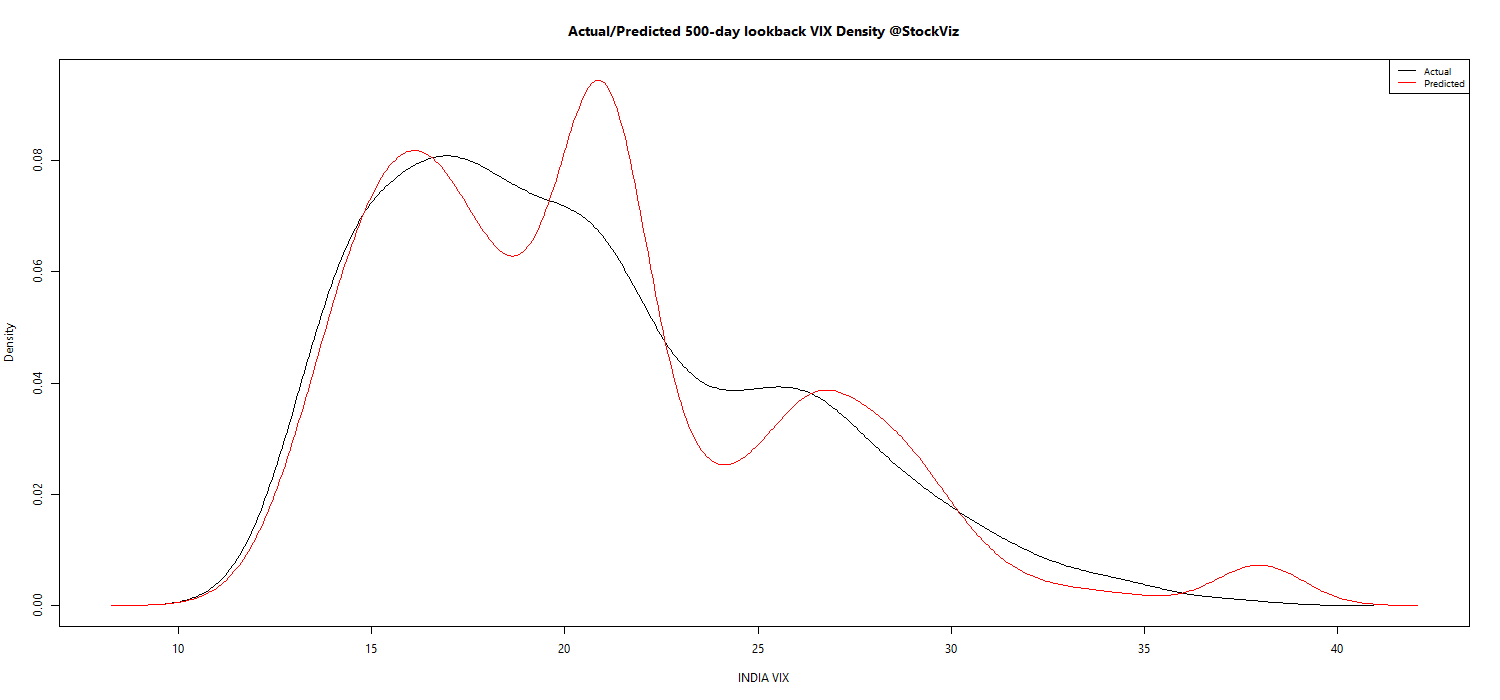

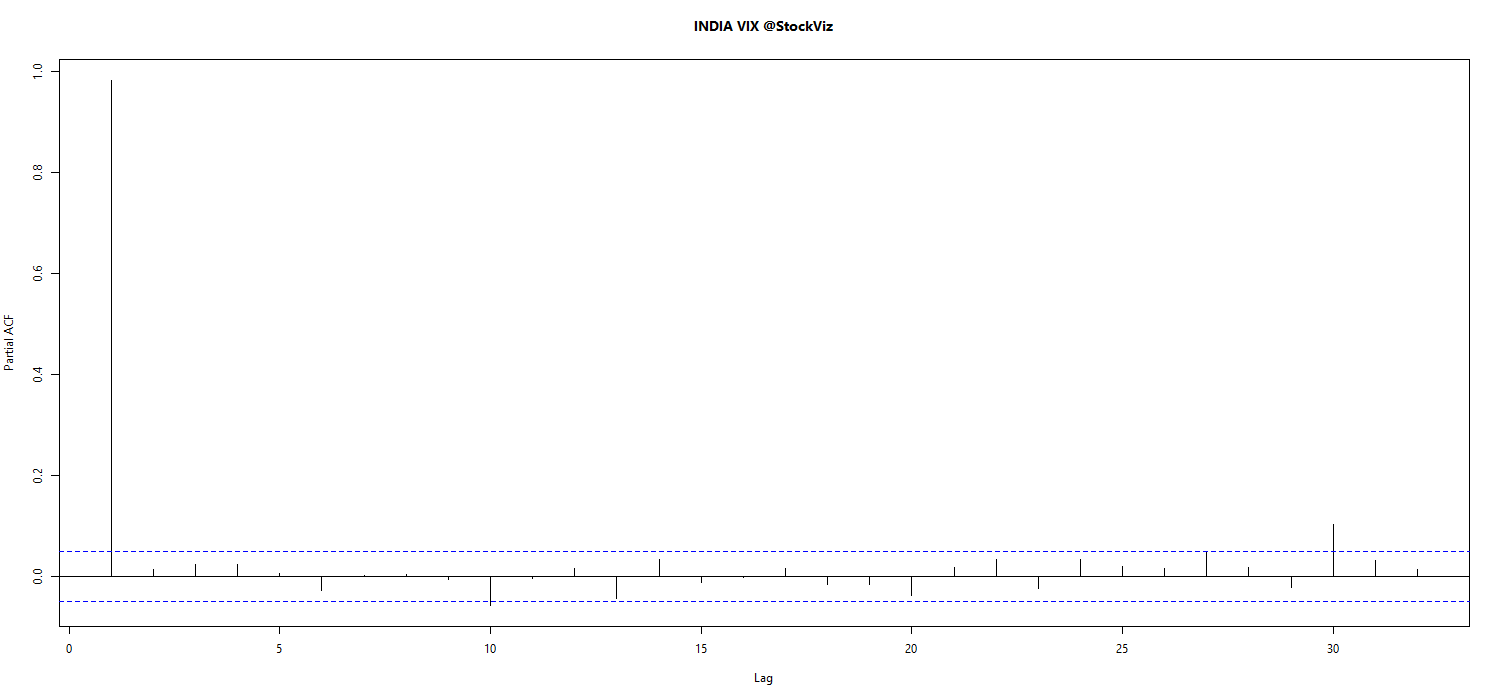

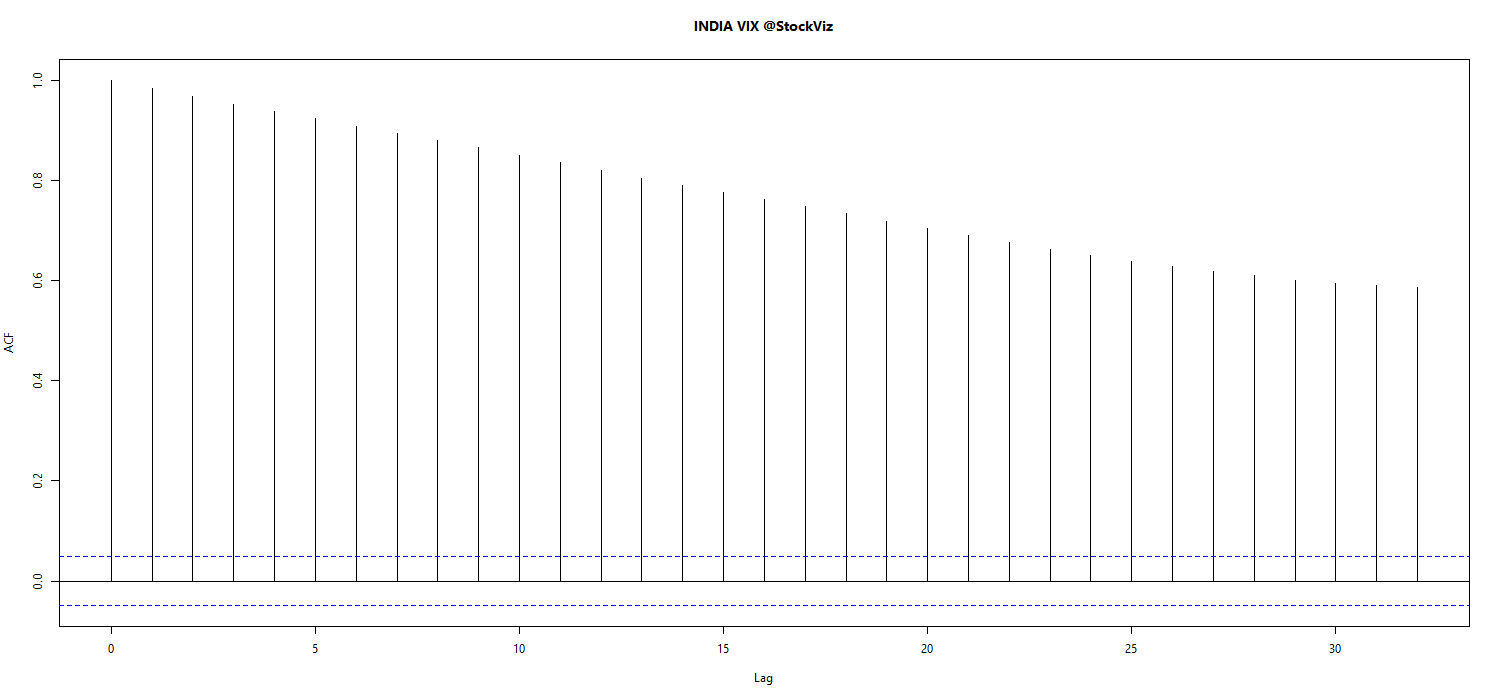

Implied volatility

Code and a lot more charts are on github.