We’ve been having a bit of fun with the S&P Sector “Spider” ETFs: Intro, Momentum, Anti-Momentum. We saw how strategies that backtested well with pre-2011 data failed later. In this post, we see if buying all ETFs with a positive return over n-months help us beat the S&P 500 index.

Calculate rolling returns over n months. Where n = 1, 3, 6, 12.

For the n+1th month, go long the ETFs that had positive returns in Step 1.

Like before, we split the dataset into Before 2010 and After 2011.

Pick your Fighter

The Before 2010 dataset shows rotation by 6- and 12-month look-back periods to be better than buying-and-holding the S&P 500.

The SPY Rope-a-Dope

MOM6 and MOM12 were too close to call in the training set. If you had “course-corrected” after the first couple of years of under-performance of MOM12 and switched to MOM6, you would’ve out-performed. On the other hand, staying the course would’ve meant losing out to the mighty S&P 500.

Once again, by simply holding onto the ropes, a passive buy-and-hold S&P 500 investor would’ve come out miles ahead of someone who tried to time sectors systematically.

What did we learn?

We tested a few basic allocation strategies that investors typically use to approach the “rotation” problem. Some of them worked well in the training set but their performance failed to carry over. Besides, if you add transaction costs and taxes, we are not sure if it was worth the effort given the post-2011 market regime.

Maybe there are more sophisticated qualitative/fundamental ways to approach this problem that work. However, most media articles about “sector rotation” are written with perfect hindsight and it is near impossible to do it with simple strategies that are accessible to the average investor.

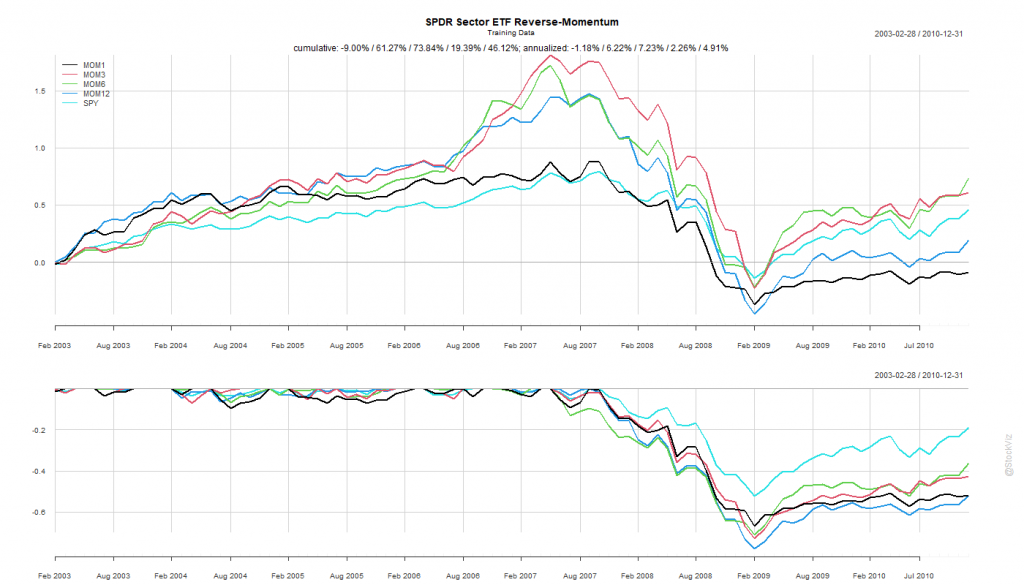

Previously, we saw how buying the best performing sector and holding it for a month didn’t quite pan out. What if, we bought the worst performing sector instead? The “Dogs of Sector Spiders,” if you will.

Calculate rolling returns over n months. Where n = 1, 3, 6, 12.

For the n+1th month, go long the ETF that had the lowest return in Step 1.

Like before, we split the dataset into Before 2010 and After 2011.

Pick your Fighter

The Before 2010 dataset shows rotation by 3- and 6-month look-back periods to be better than buying-and-holding the S&P 500.

The 6-month look-back rotation strategy – MOM6 – would’ve been the strategy to bet on.

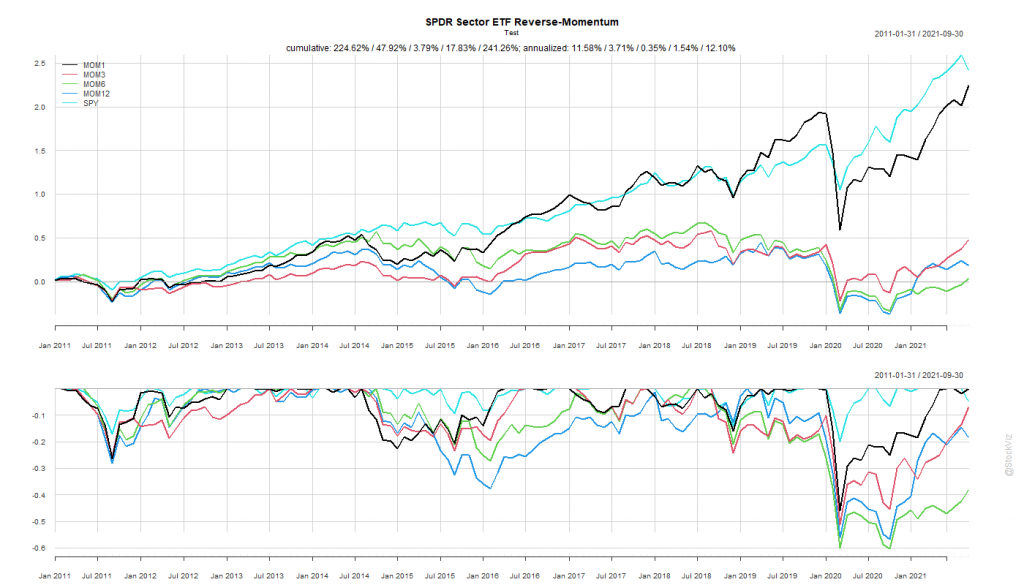

The SPY Rope-a-Dope

“Sure-things” don’t exist in finance.

MOM6 spent the last decade getting absolutely decimated by the S&P 500.

Once again, by simply holding onto the ropes, a passive buy-and-hold S&P 500 investor would’ve come out miles ahead of someone who employed this rotation strategy.

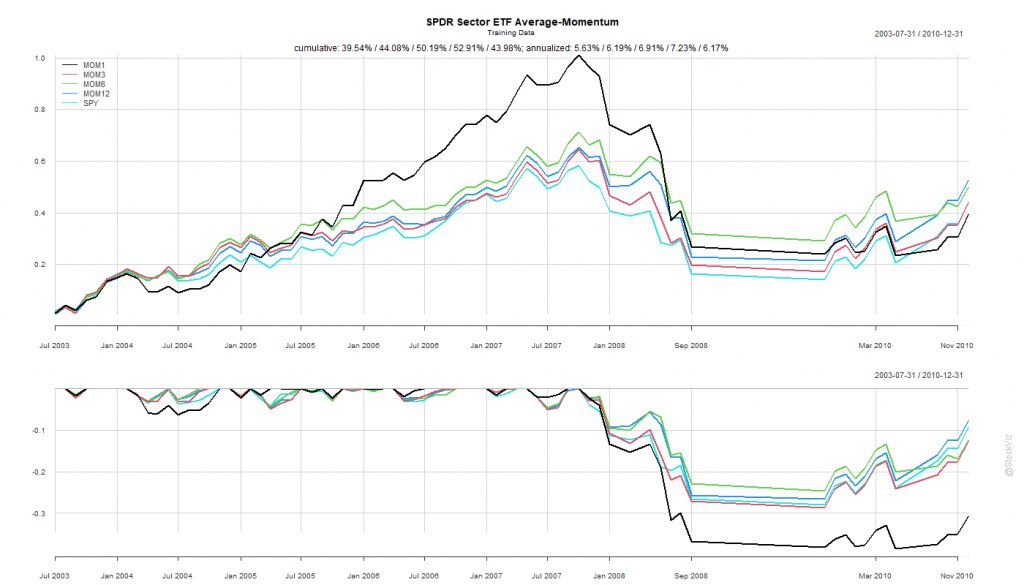

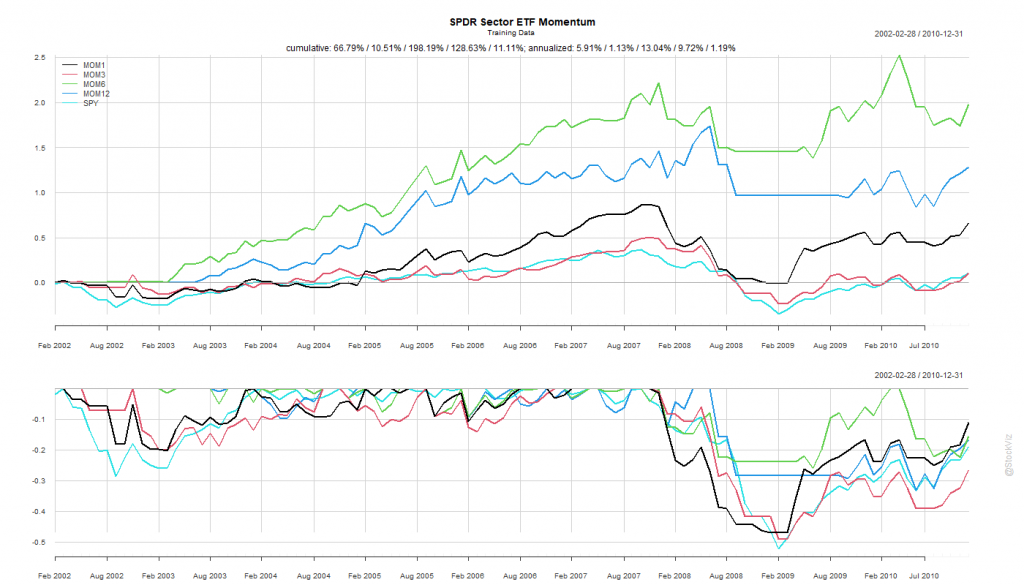

While introducing S&P 500 sector ETFs, we showed how the cross-correlations between them were unstable. This makes developing simple strategies challenging. One common momentum strategy is to simply go long whatever worked best in the previous period.

Rules of Rotation

For ETFs: XLY, XLP, XLE, XLF, XLV, XLI, XLB, XLK, XLU, and SPY

Calculate rolling returns over n months. Where n = 1, 3, 6, 12.

For the n+1th month, go long the ETF that had the highest return in Step 1.

In Step 2, if the selected ETF has -ve returns, stay in cash and earn zero.

We split the dataset into Before 2010 and After 2011.

Pick your Fighter

The Before 2010 dataset shows rotation by all look-back periods to be better than buying-and-holding the S&P 500.

Probably because of the prolonged dislocation caused by the GFC in 2008 and 2009, all rotation strategies based on the rules above exhibited great stats.

The 6-month look-back rotation strategy – MOM6 – gave an annualized return of 13.04% vs. S&P 500’s 1.19%. Coming out of the crisis, this would have been the fighter to bet on.

The SPY Rope-a-Dope

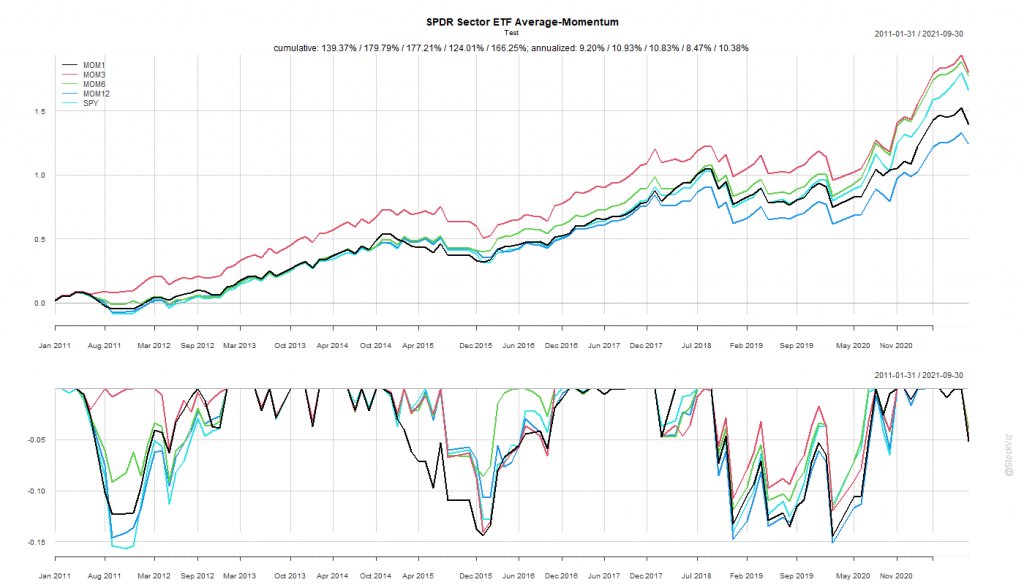

In boxing parlance, a “Rope-a-Dope” is

When you maintain a defensive posture on the ropes in an attempt to outlast or tire your opponent. It is most recognized and was actually given that name by Muhammad Ali when he employed the technique to defeat George Foreman.

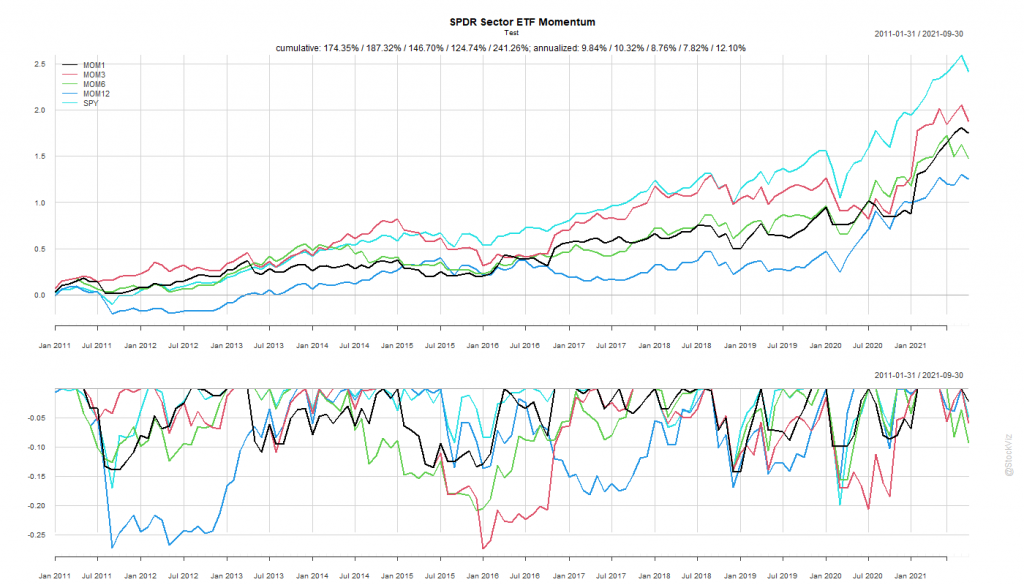

The After 2011 dataset is a prime exhibit of why “sure-things” don’t exist in finance.

The S&P 500 spent the next decade demolishing everything.

MOM6, the winner from our first round, went on to underperform the S&P 500 for the next 10 years by ~4%

By simply holding onto the ropes, a passive buy-and-hold S&P 500 investor would’ve come out miles ahead of someone who employed this rotation strategy.

State Street Global Advisors (SSGA) is known for its monster S&P 500 SPY ETF. With roughly $390 billion in AUM, SPY is one of the largest ETFs out there. Apart from SPY, they are also known for their SPDR “Spider” sector ETFs.

SYMBOL

FUND

LAUNCH_YEAR

XLB

Materials Select Sector SPDR Fund

1998

XLE

Energy Select Sector SPDR Fund

1998

XLV

Health Care Select Sector SPDR Fund

1998

XLI

Industrial Select Sector SPDR Fund

1998

XLY

Consumer Discretionary Select Sector SPDR Fund

1998

XLP

Consumer Staples Select Sector SPDR Fund

1998

XLF

Financial Select Sector SPDR Fund

1998

XLU

Utilities Select Sector SPDR Fund

1998

XLK

Technology Select Sector SPDR Fund

1998

XLRE

Real Estate Select Sector SPDR Fund

2015

XLC

Communication Services Select Sector SPDR Fund

2018

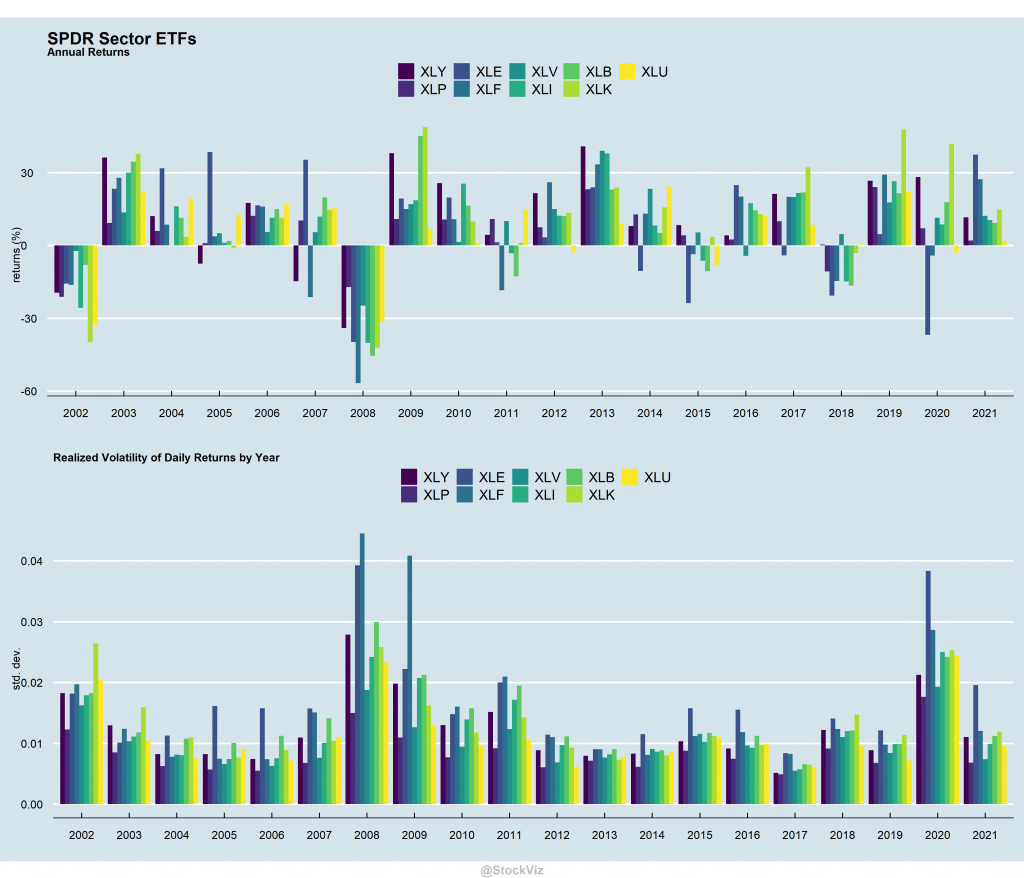

Sector ETFs

These ETFs allow investors to take a concentrated bet on a specific sector and are often used as a benchmark for professionals who specialize in those sectors.

Markets go through cycles where some sectors do well and some don’t. Some sectors are extremely volatile and some barely move.

Cross-correlations are all over the place.

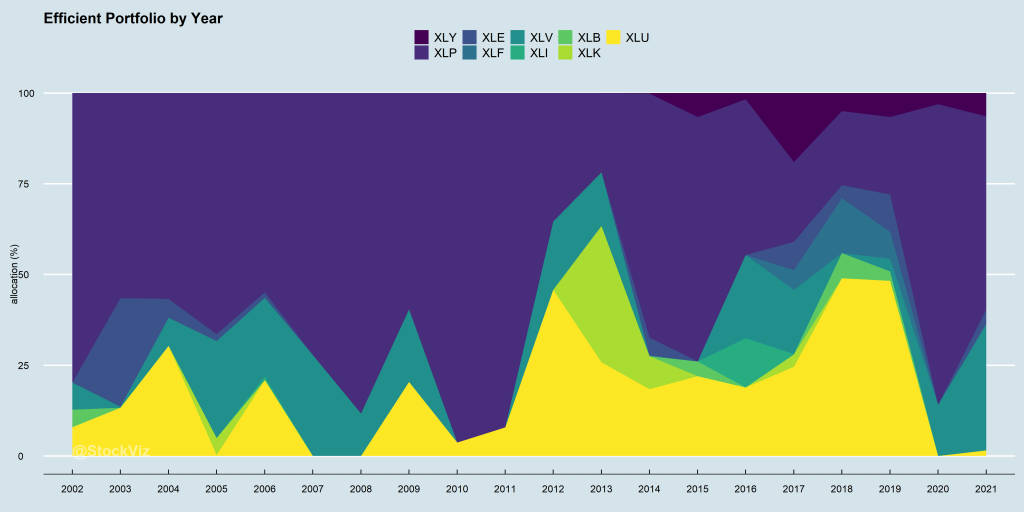

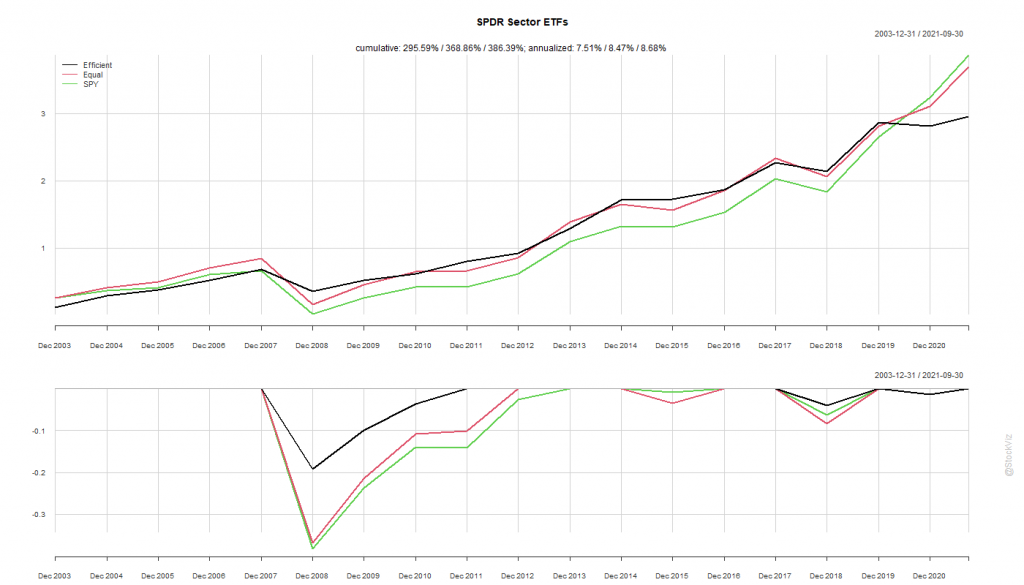

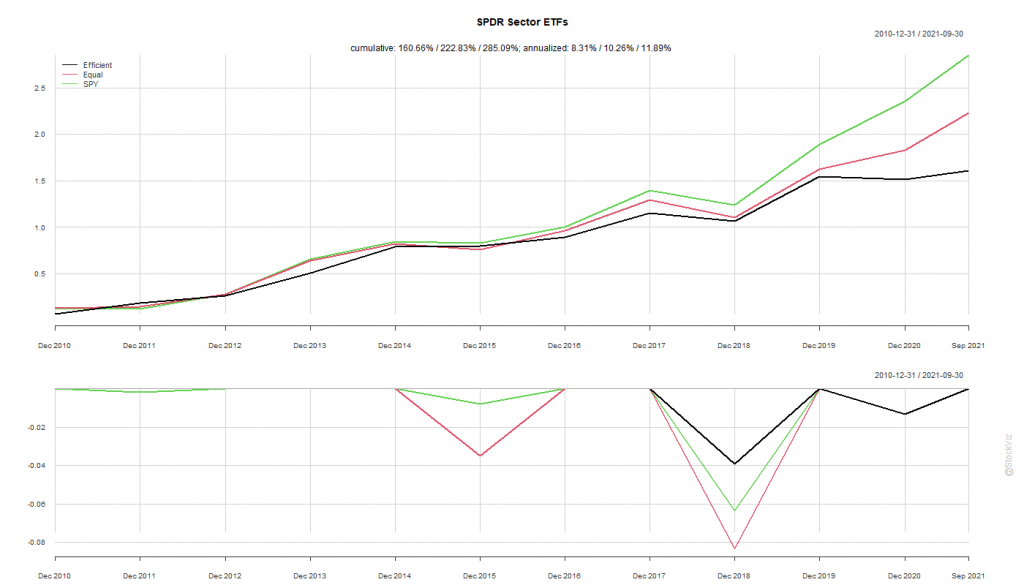

Given unstable cross-correlations and volatility, a naïve use of optimizers is a bad idea. For example, if you use these as inputs to generate an “efficient” portfolio, the weights wary widely from year to year.

Consumer Staples (XLP) ends up gobbling up most of the allocation, followed by Utilities (XLU.) The performance of such a portfolio depends on what you are looking for.

The efficient portfolio, given its large exposure to staples and utilities, has experienced lower drawdowns than both equity-weighted and S&P 500. This shows up in their Sharpe Ratios.

For the longest time in the US, actively managed mutual funds ruled the roost. Then came Jack Bogle with his index fund and the ceaseless mantra of “costs and taxes matter” and the dynamic shifted, slowly at first and then suddenly, in favor of indexing. It was only a matter of time before people figured out the tax loophole of ETFs and now, there are over 2500 ETFs listed in the US.

Unlike in India, where mutual funds are “pass through,” US mutual fund investors pay capital gains tax on assets sold by their funds. When there are large-scale redemptions, say, during a market melt-down, funds are forced to sell their holdings. This generates capital gains taxes, meaning that investors have to pay tax on assets that had fallen sharply in value1.

ETFs, on the other hand, don’t have to subject their investors to such harsh tax treatment. ETF providers offer shares “in kind,” with authorized participants serving as a buffer between investors and the providers’ trading-triggered tax events.

A Plethora

Of the ETFs that survive today, the number of launches every year has trended higher.

While Equity ETFs dominate launches, the share of fixed income, alternatives, etc. has increased as well.

Most of the AUM resides in “vanilla” strategies – typically market-cap based.

The winner HAS taken all

Plot the assets of each ETF, in billions, in log-scale and you can tell that this is a game of scale.

Of the total 2577 ETFs, 2022 (78.5%) have less than a billion dollars in assets. You need to filter for $10 billion and up to just see the x-axis.

The top 3 issuers: Blackrock, Vanguard and SSGA manage ~80% of all ETF assets.

Where there is an ETF, there’s an Index

Until last year, ETFs were supposed to be a “passive” entity. There were no “actively managed” ETFs. In order to be passive, an ETF needed to follow an index. And indices had to be rules based – however convoluted the rules. And issuers needed a third-party to provide the index.

The rise of ETFs (and passive investing, in general) put index providers in the middle of all the a action. They became a crucial cog in world finance that can make or break entire economies. So powerful, in fact, that China blackmailed MSCI to include its domestic stocks in its Emerging Markets Index, which is tracked by close to $2 trillion in assets2. And India has been working on inclusion of Indian sovereign bonds in global bond indices3.

We can see industry consolidation here as well. The top 5 index providers control ~75% of ETF AUM (more if you include index funds.) S&P Global and MSCI are as close to “pure-play” index providers as you can get and their stock market performance is off-the-charts.

Fee Squeeze and Innovation

The problem with index ETFs/funds is that buyers only care about two things: expense ratio and tracking error. This resulted in a massive fee war that saw the vanilla-passive industry consolidate around Blackrock and Vanguard. For example, Vanguard’s S&P 500 ETF’s expense ratio is 3bps.

So, what next?

International ETFs

The first wave was ETFs providing international diversification. However, the “home-bias” is pretty strong with AUM under international ETFs barely making a quarter of the total.

On a weighted average basis, these ETFs charge about 30bps. However, since these are mostly cap-weighted, the fee-war is just as intense here.

Leveraged/Inverse ETFs

Many investors have mandates that prevent them from trading derivates outright. This is especially true for Indian investors taking the LRS route to invest in the US. However, Wall Street has your back.

Leveraged ETFs give you 2x or 3x the daily returns of a benchmark index like the S&P 500 or the Nasdaq 100. Feeling bearish? Inverse ETFs do the opposite.

Caveat: These are NOT buy-and-hold investments and are more suitable for day-traders. The discussion requires a separate post.

On a weighted average basis, these ETFs charge about 100bps. While lucrative, they are mostly niche.

Active ETFs

An ETF’s tax-free wrapper make it an order of magnitude more attractive than an identical mutual fund. New issuers/managers have taken advantage of this and launched actively managed ETFs.

On a weighted average basis, active ETFs charge about 50bps. These are still early days for this category – they barely make 5% of total ETF assets. Liquidity and tracking errors during market crisis are yet to be tested.

Conclusion

There is a plethora of choices when it comes to ETFs in the US. If you plan to wander away from the plain-vanilla stuff, please take the time to read the prospectus and understand how it works.

If you are looking for simple, pre-canned investment strategies to invest in the US, check out freefloat.us