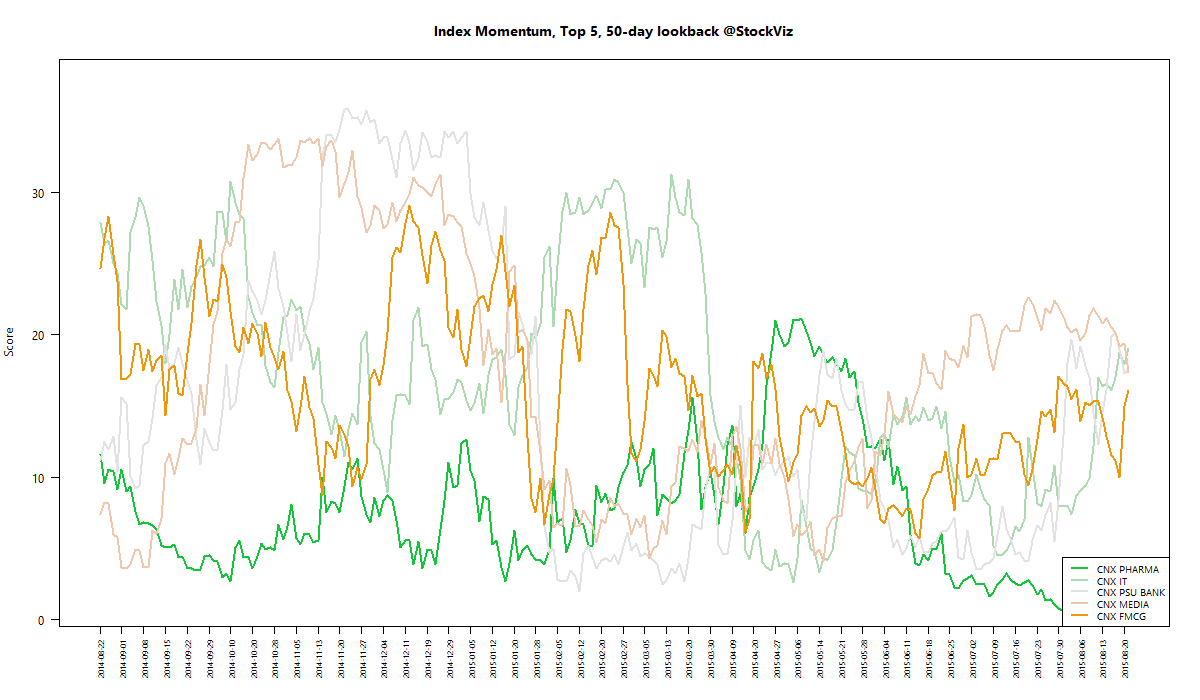

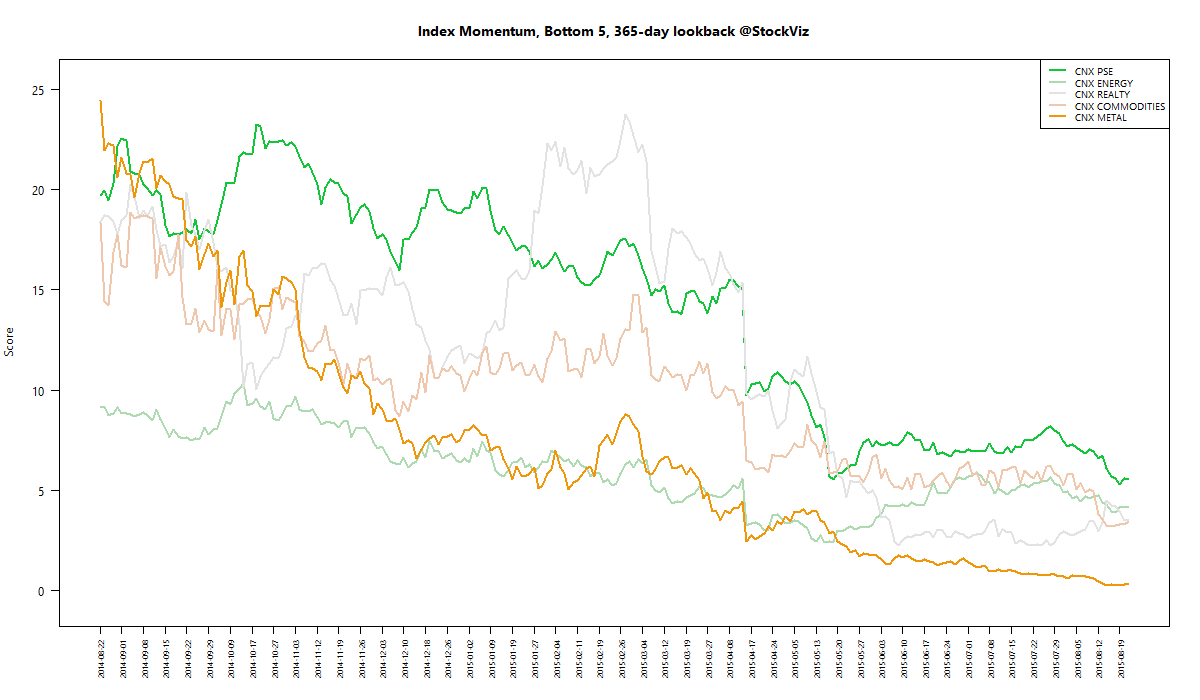

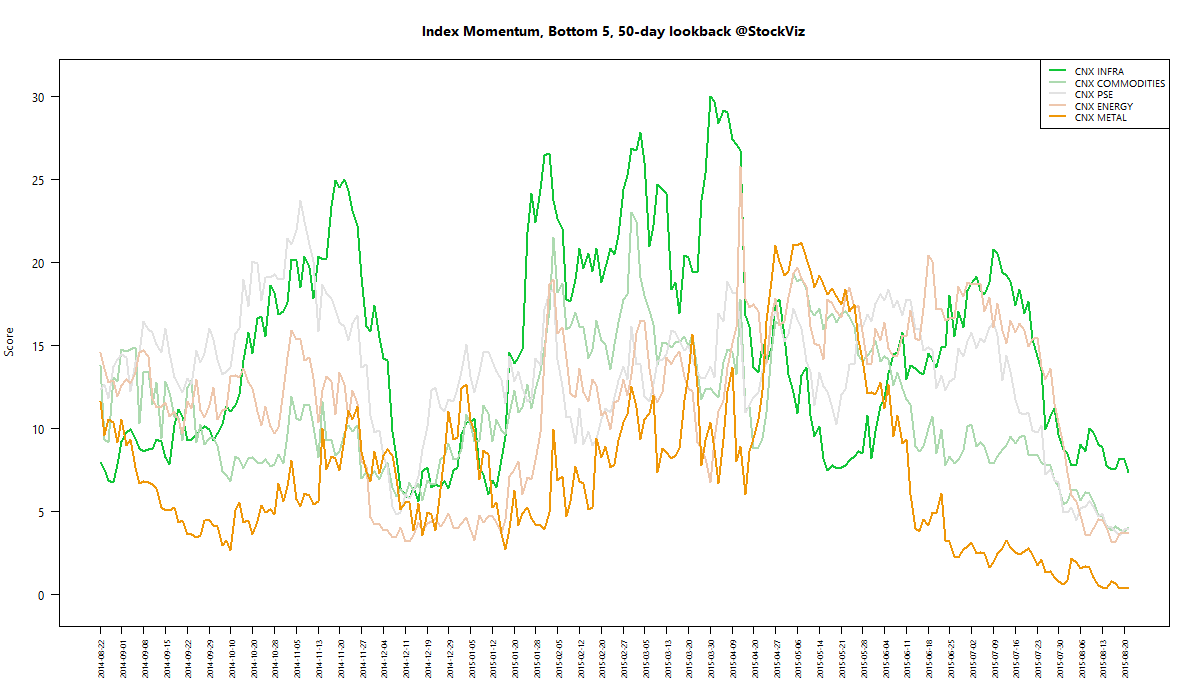

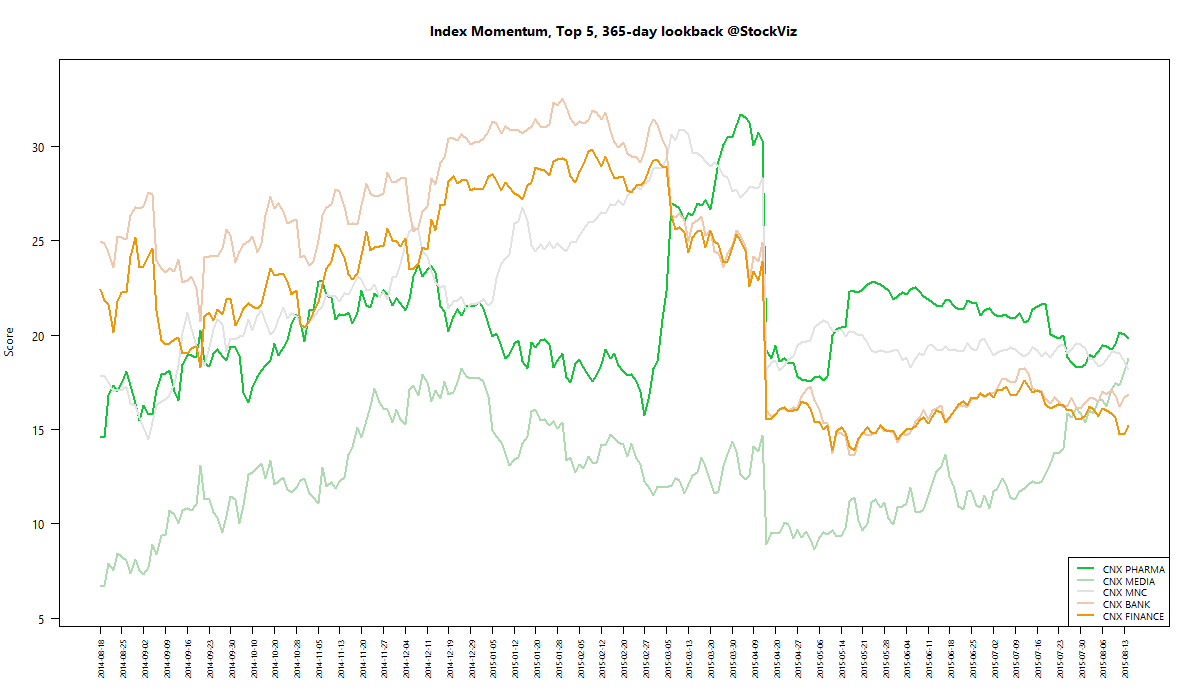

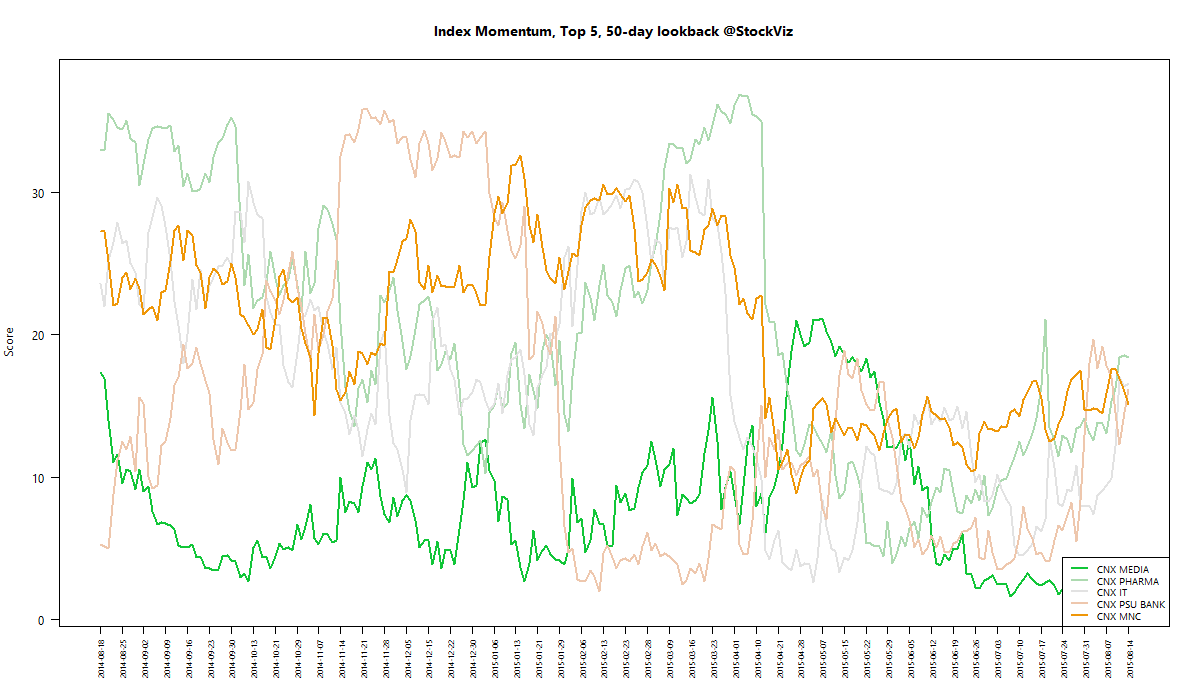

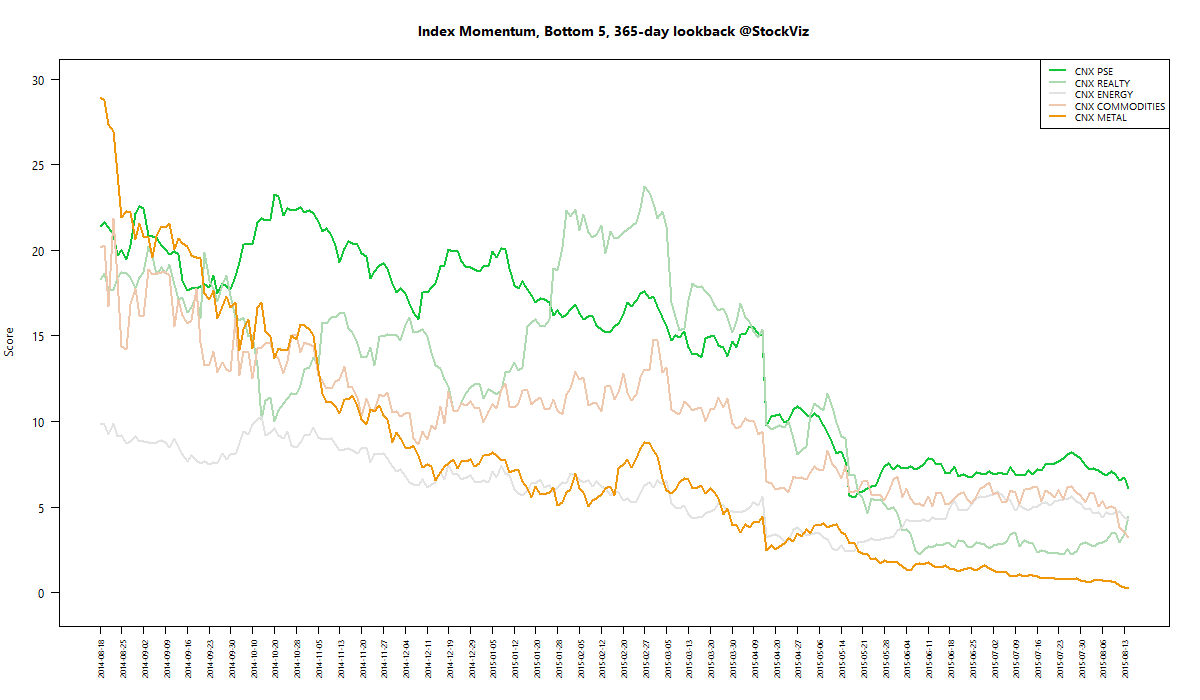

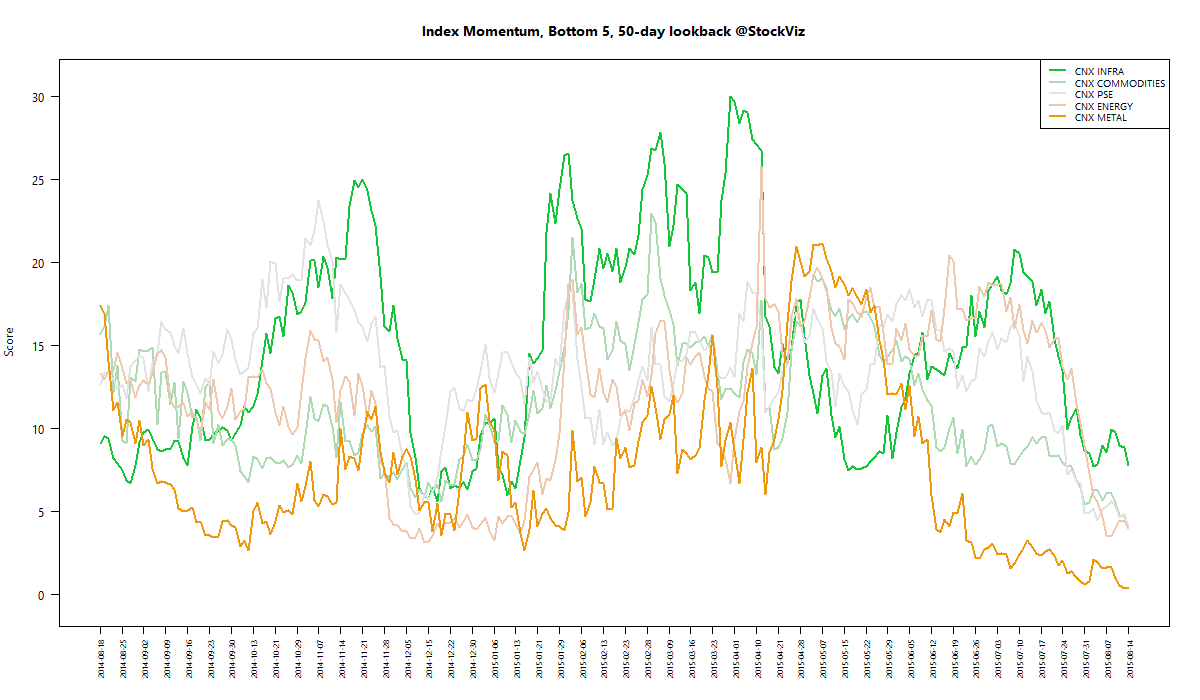

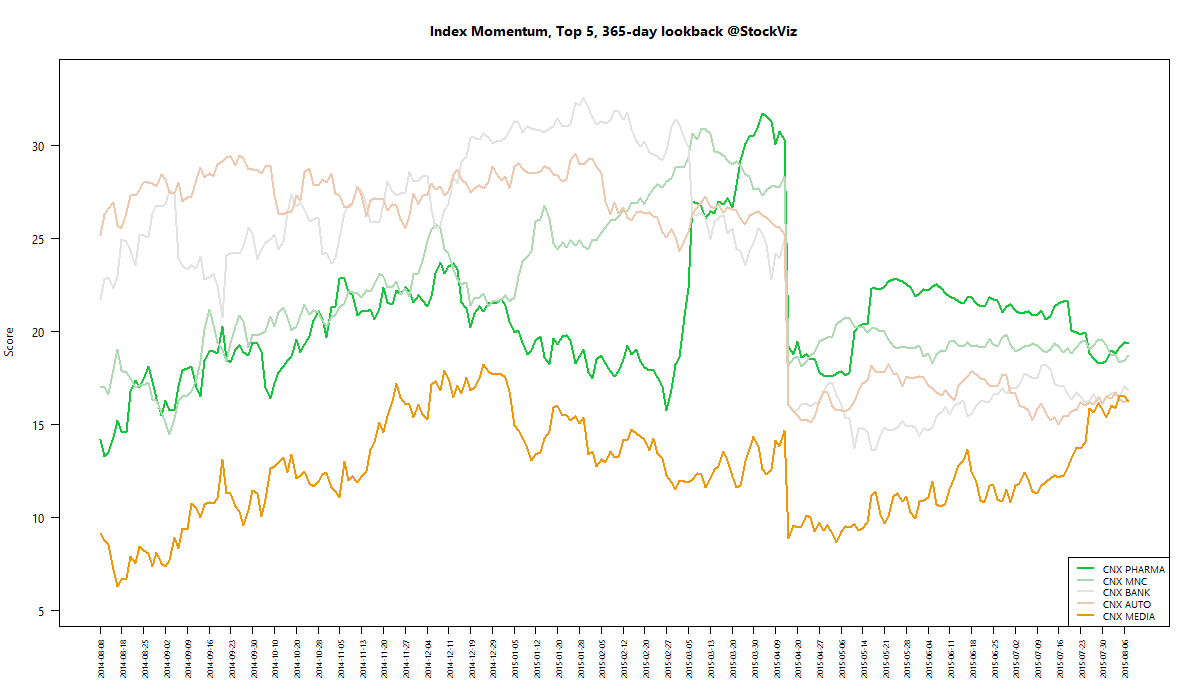

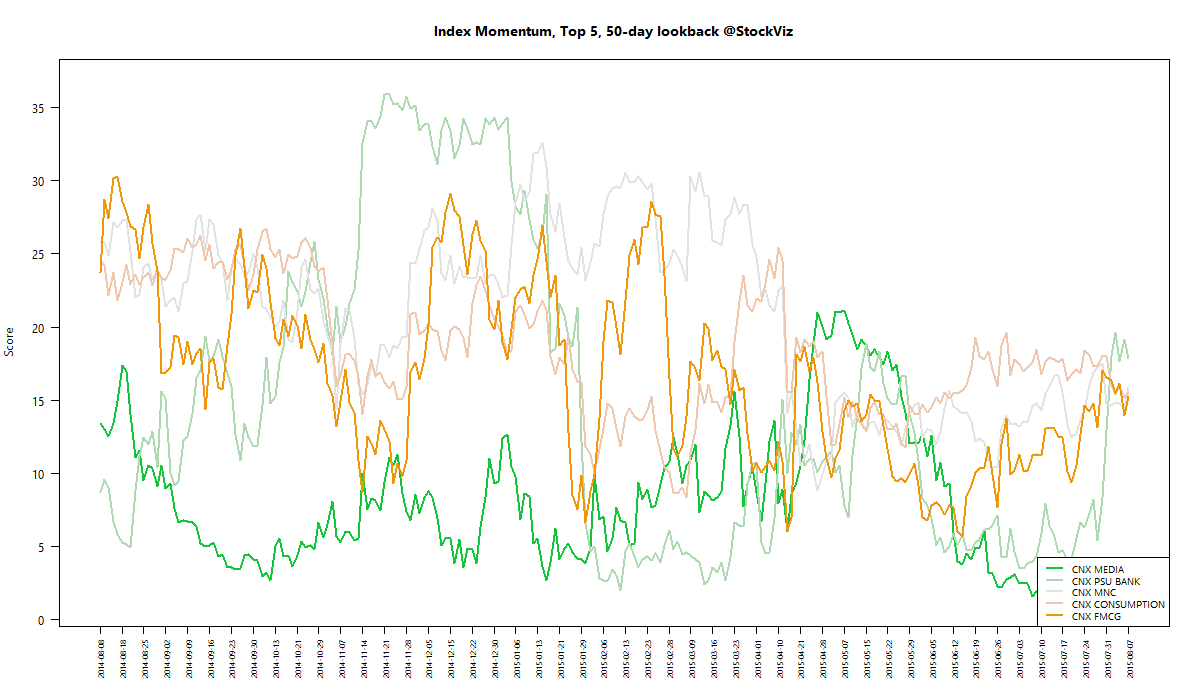

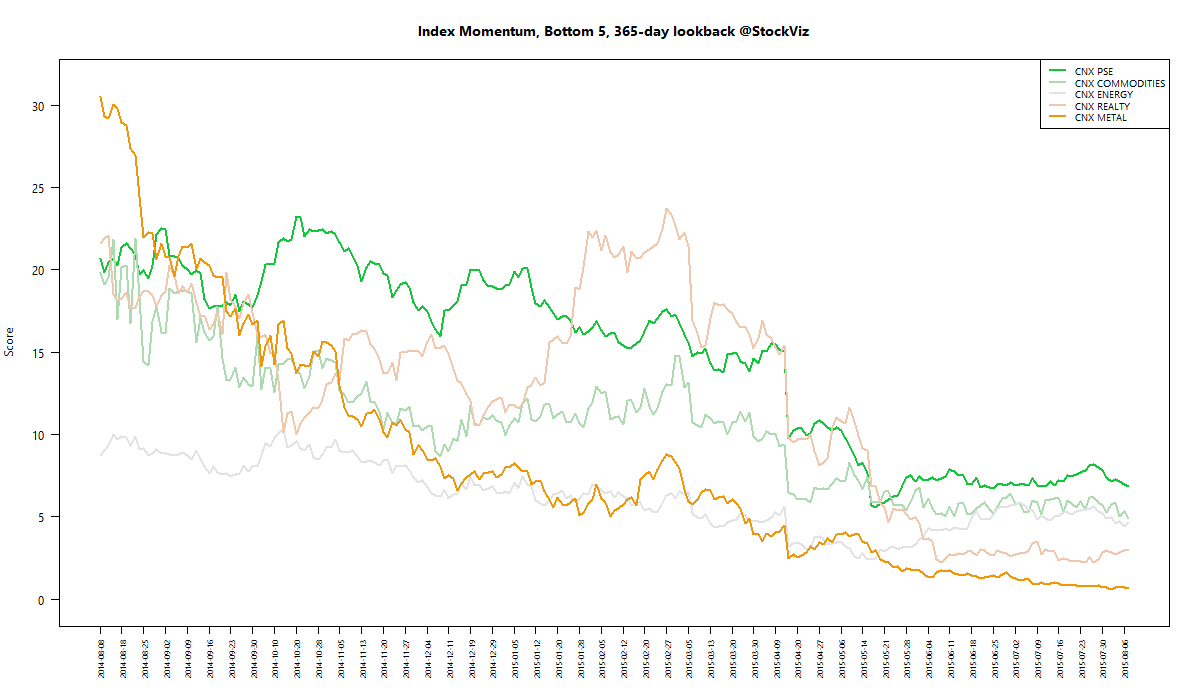

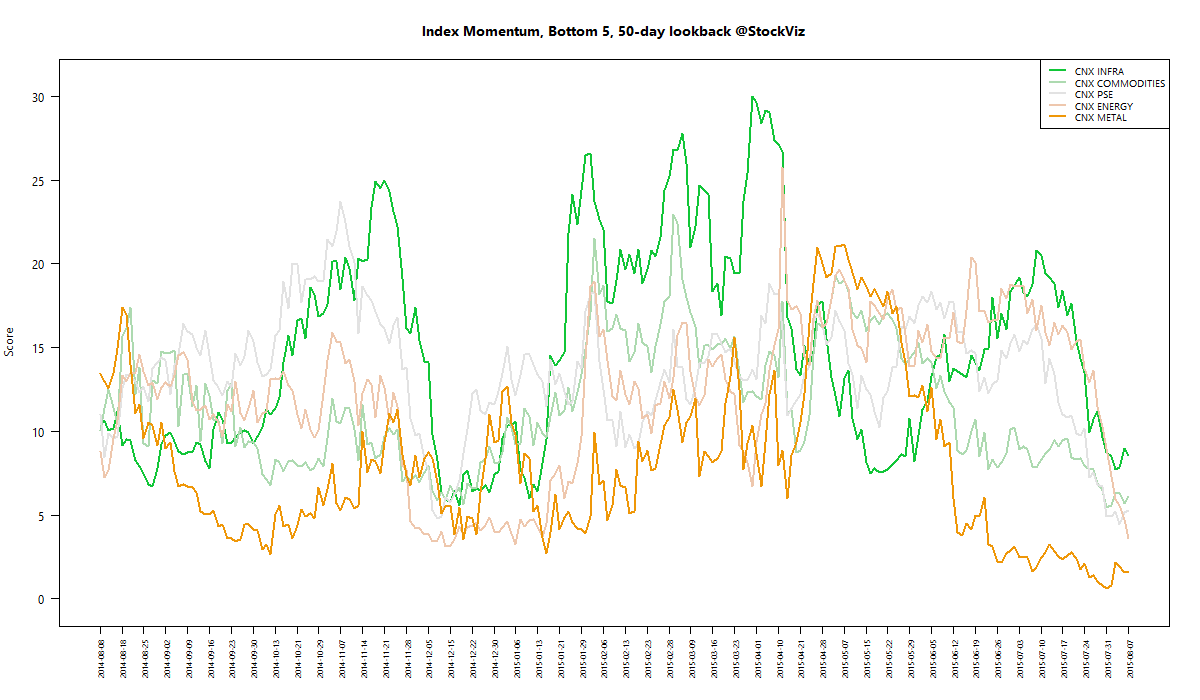

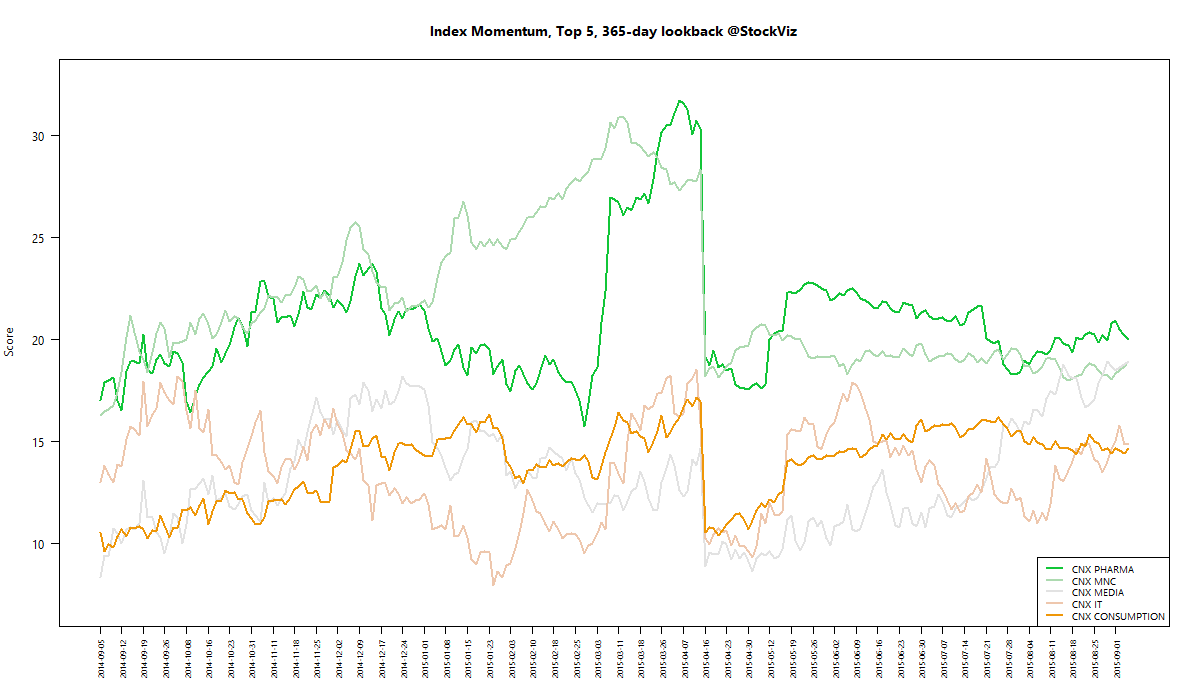

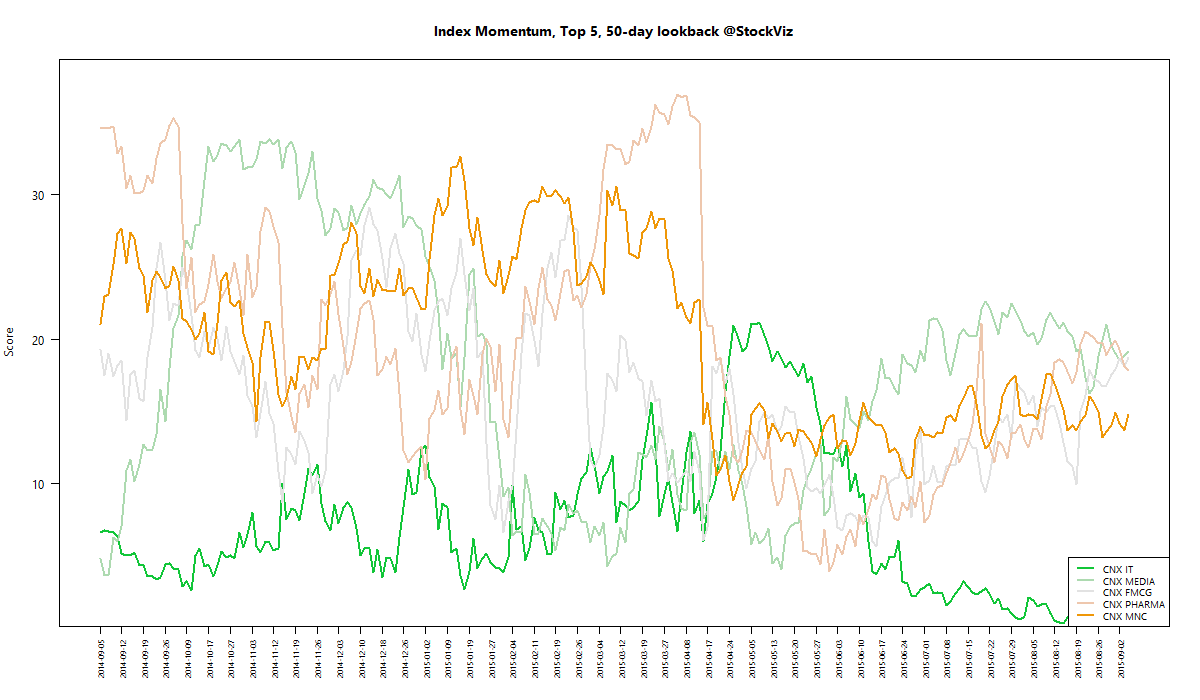

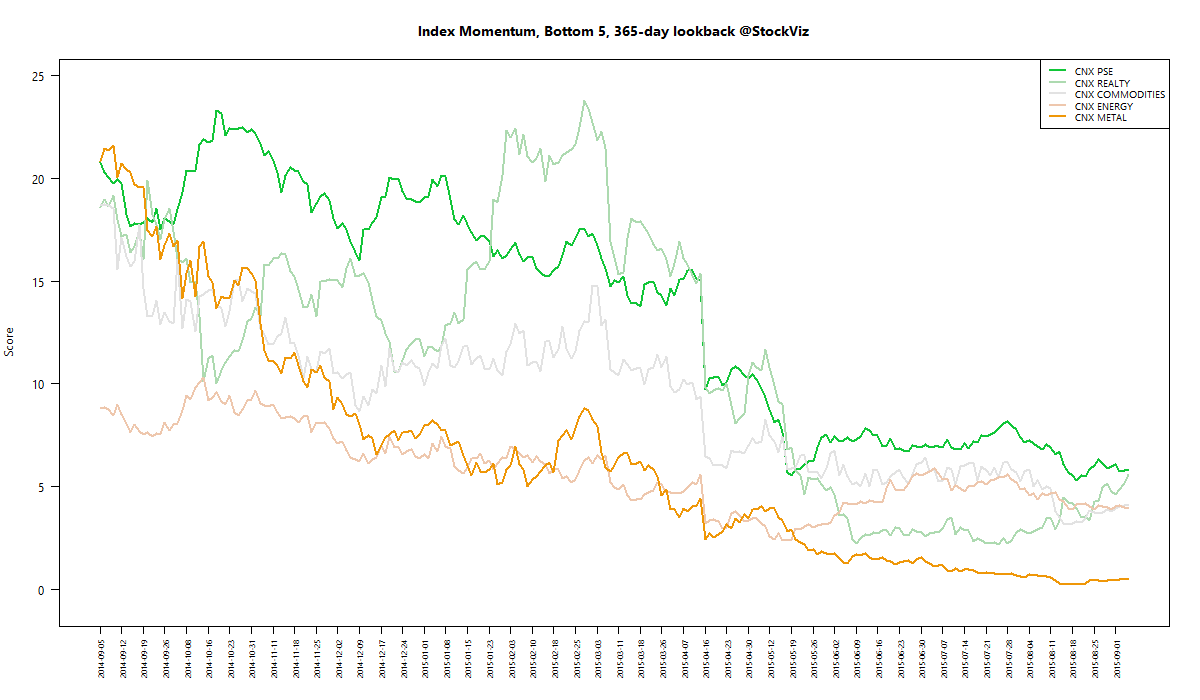

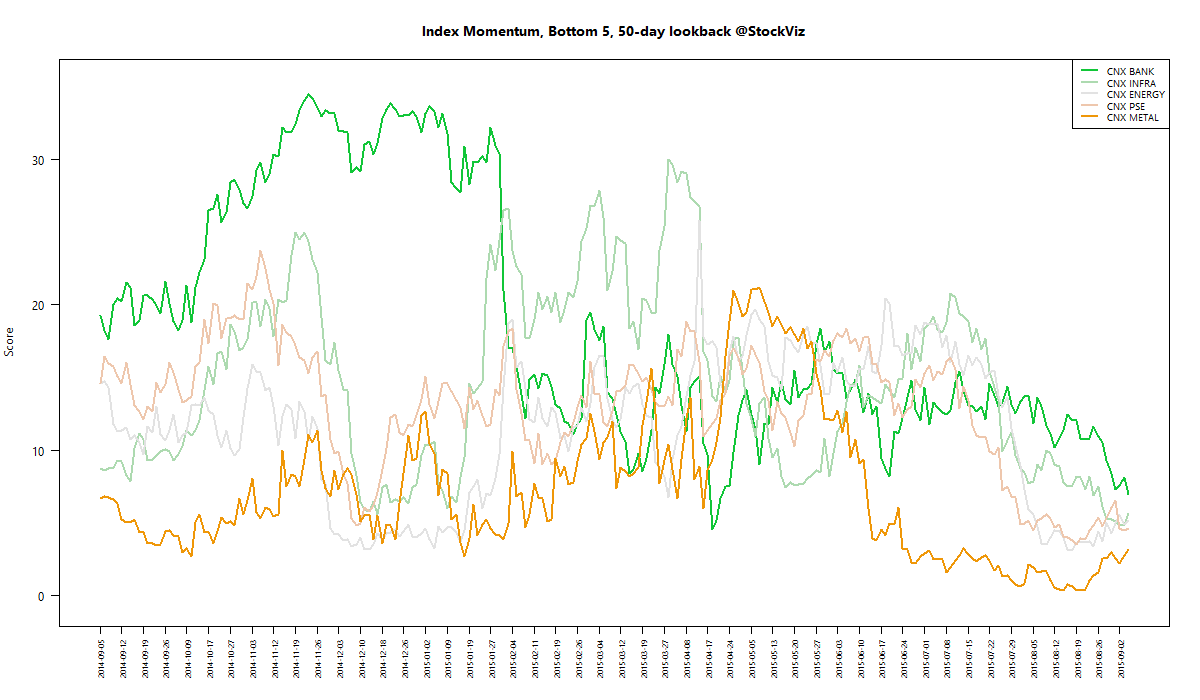

MOMENTUM

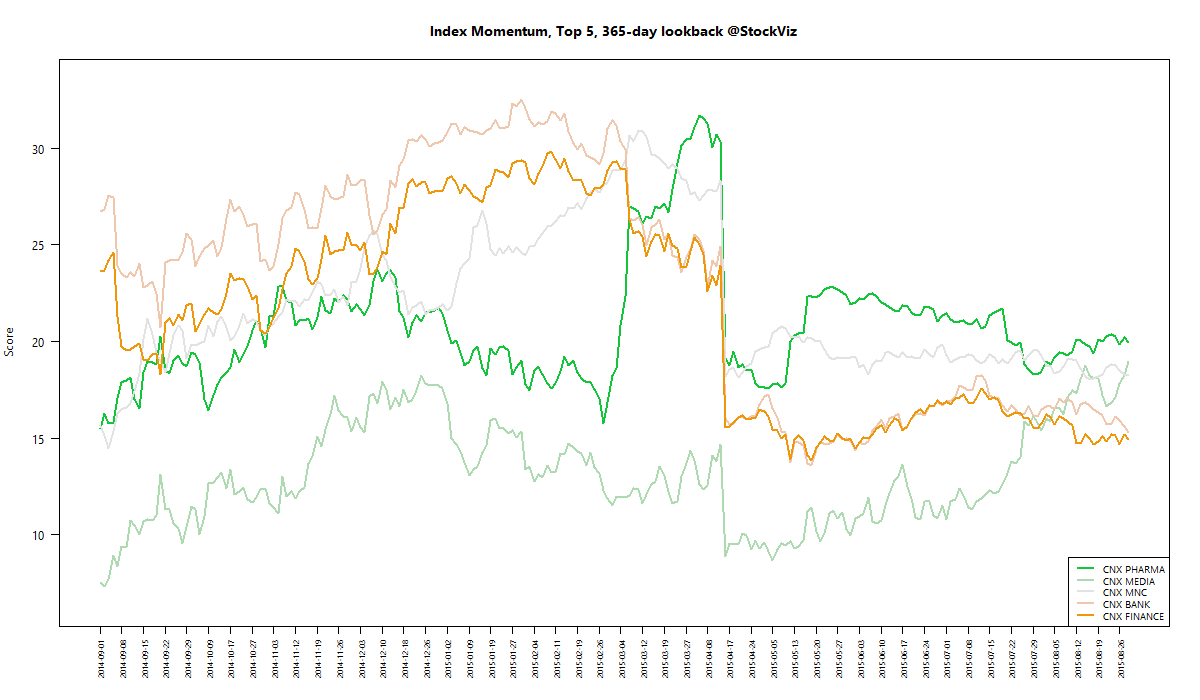

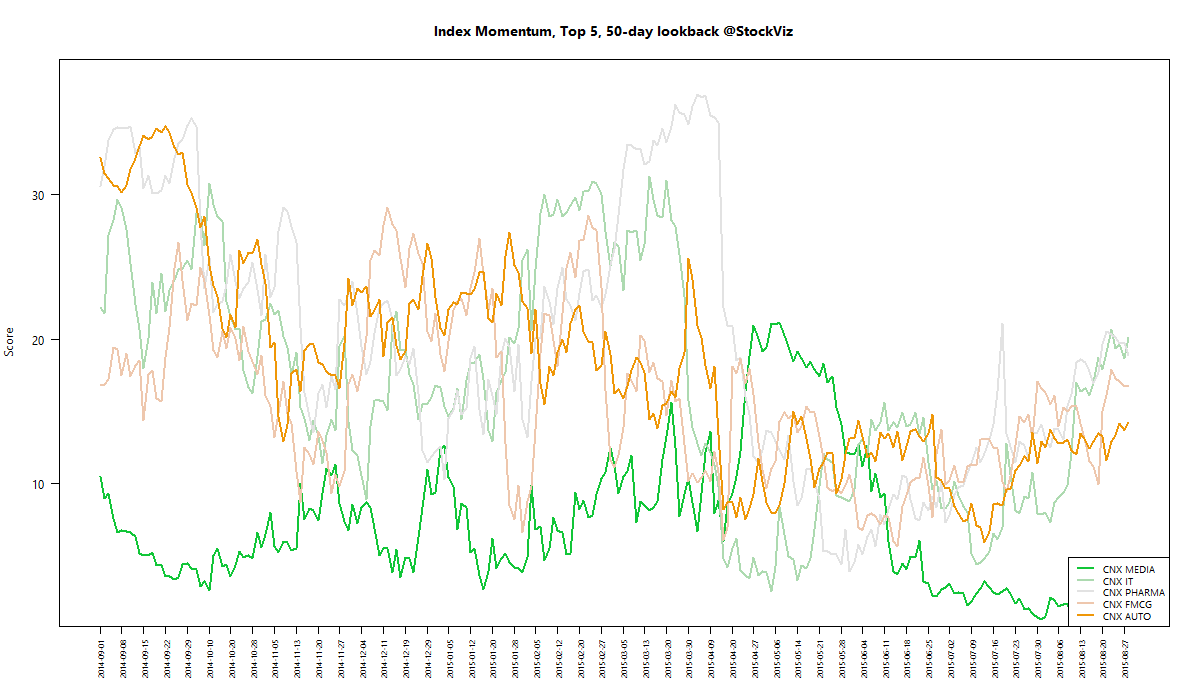

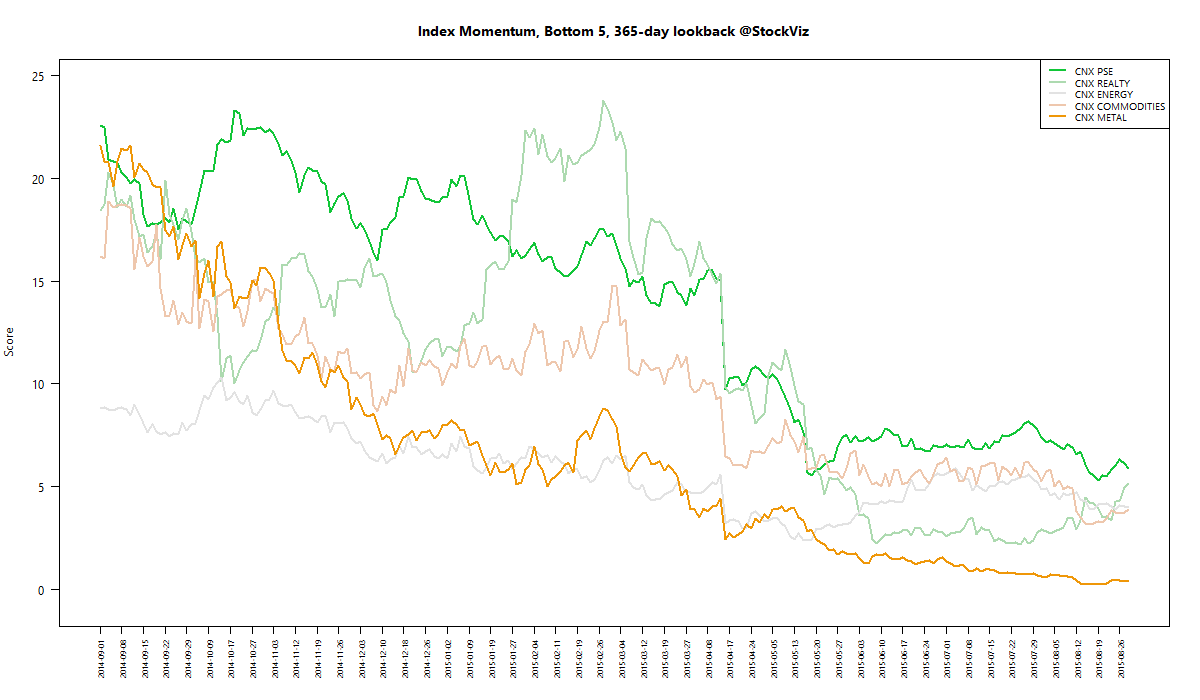

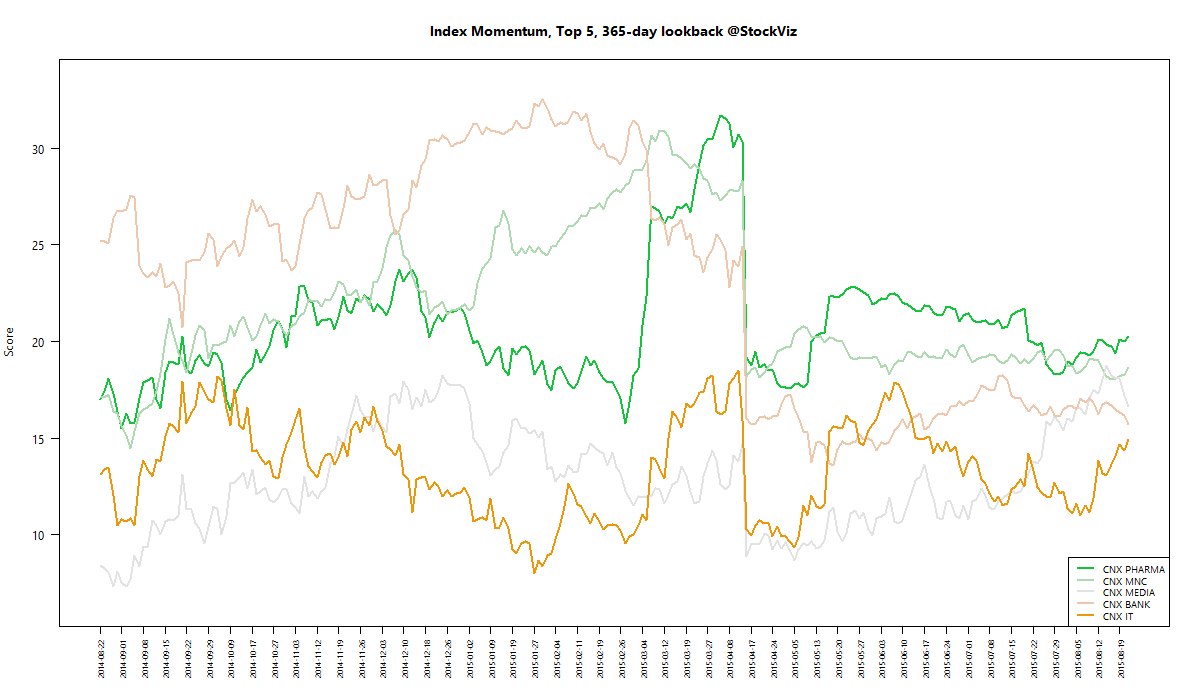

We run our proprietary momentum scoring algorithm on indices just like we do on stocks. You can use the momentum scores of sub-indices to get a sense for which sectors have the wind on their backs and those that are facing headwinds.

Traders can pick their longs in sectors with high short-term momentum and their shorts in sectors with low momentum. Investors can use the longer lookback scores to position themselves using our re-factored index Themes.

You can see how the momentum algorithm has performed on individual stocks here.

Here are the best and the worst sub-indices:

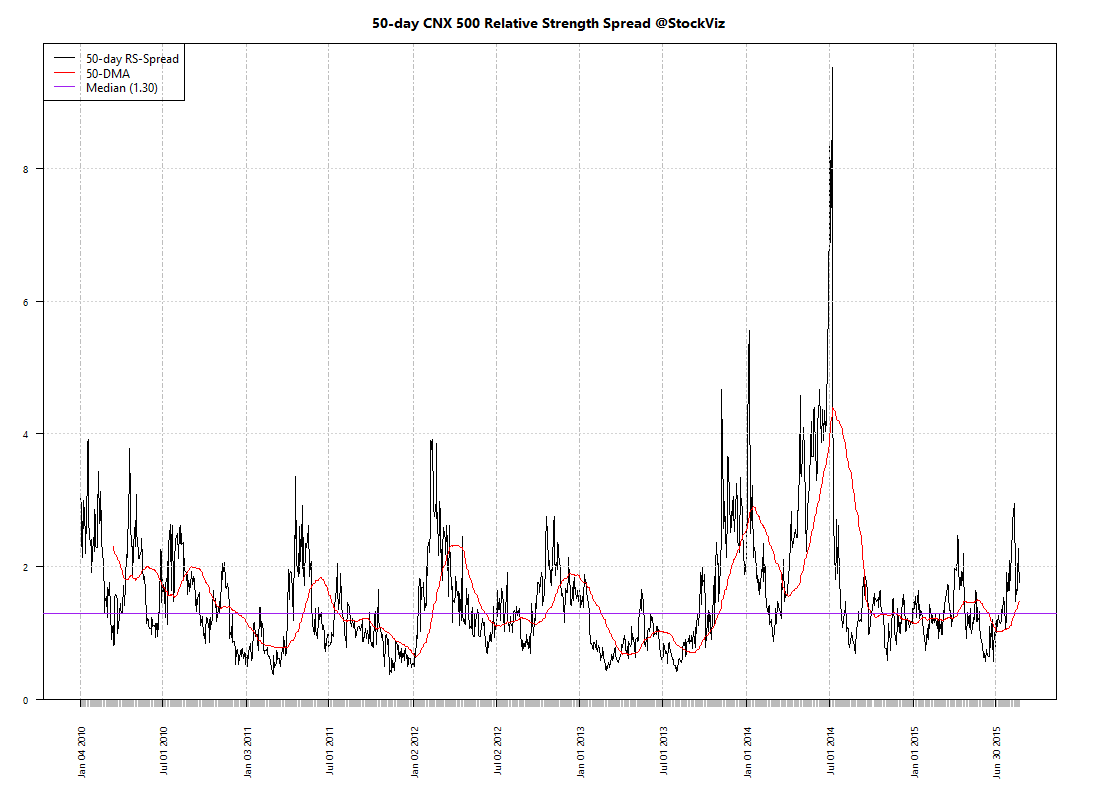

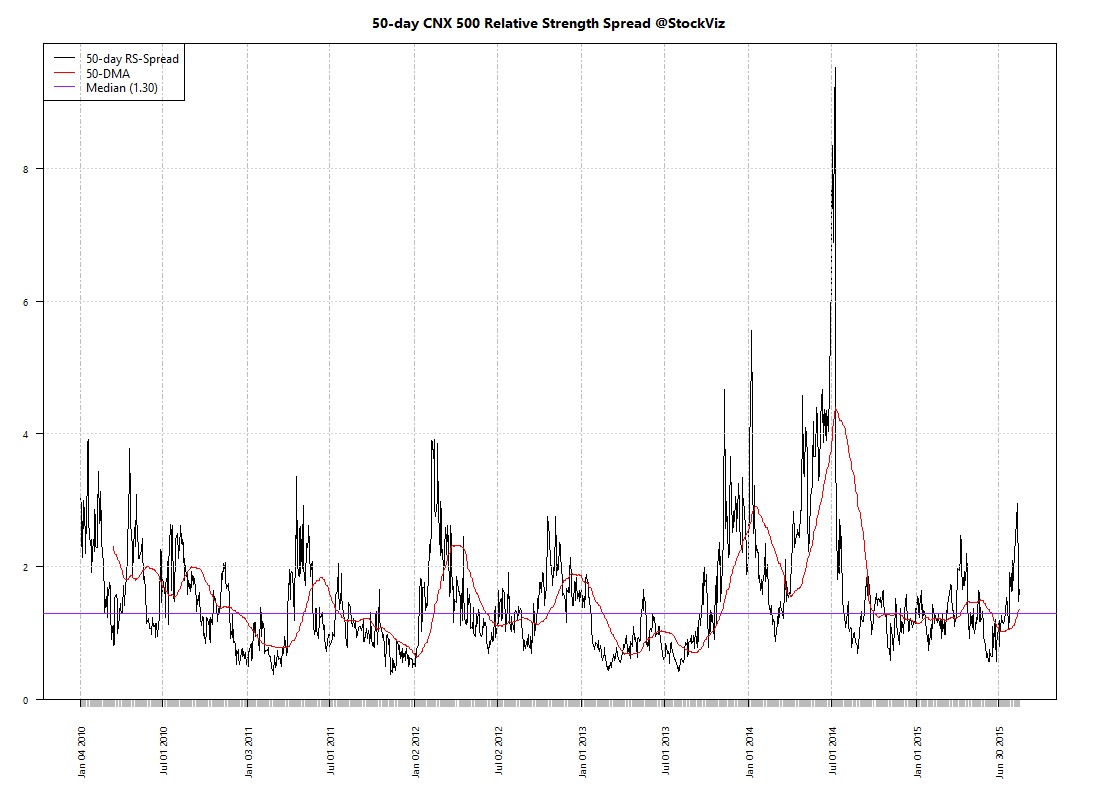

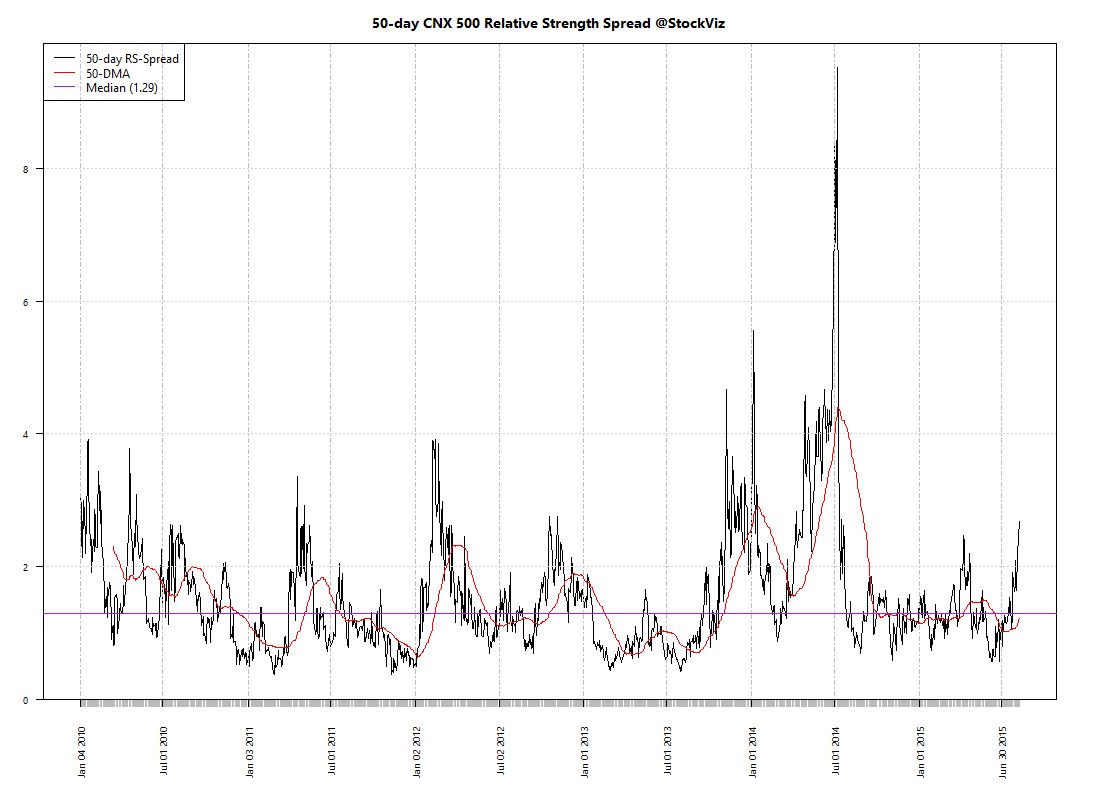

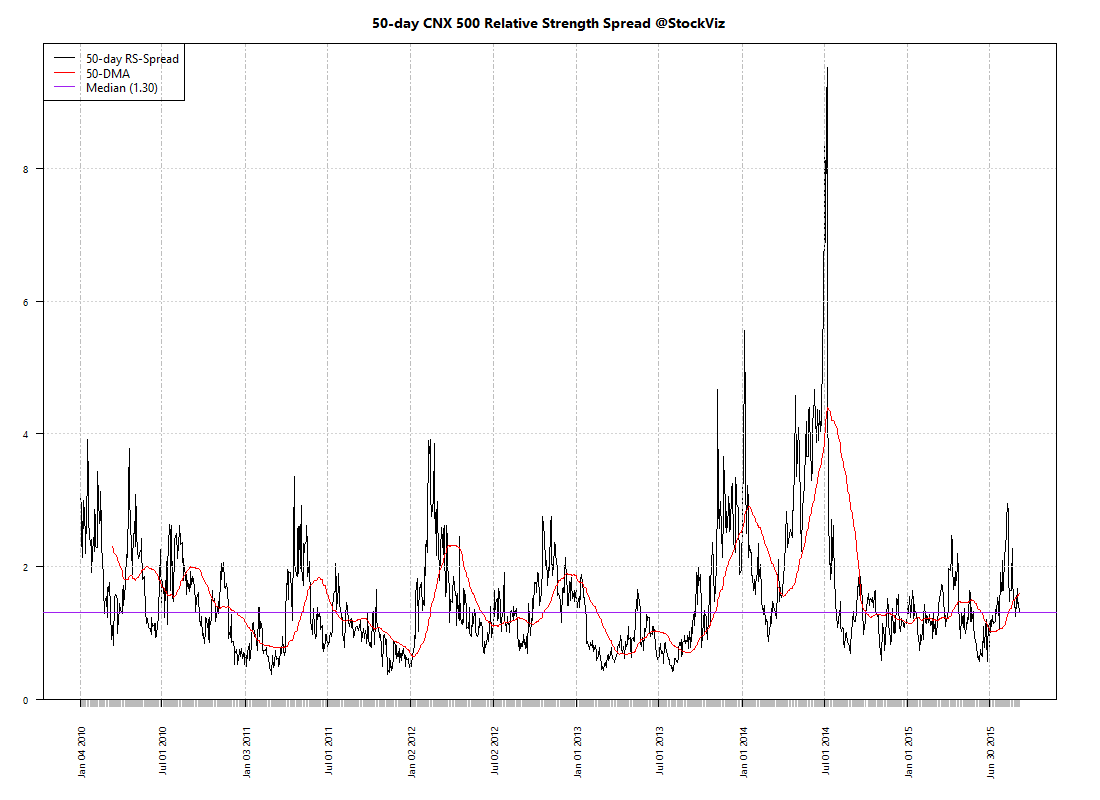

Relative Strength Spread

Refactored Index Performance

50-day performance, from June 29, 2015 through September 04, 2015:

Trend Model Summary

| Index | Signal | % From Peak | Day of Peak |

|---|---|---|---|

| CNX AUTO | SHORT |

16.93

|

2015-Jan-27

|

| CNX BANK | LONG |

21.53

|

2015-Jan-27

|

| CNX COMMODITIES | SHORT |

38.49

|

2008-Jan-04

|

| CNX CONSUMPTION | SHORT |

11.06

|

2015-Aug-05

|

| CNX ENERGY | SHORT |

38.72

|

2008-Jan-14

|

| CNX FMCG | SHORT |

11.77

|

2015-Feb-25

|

| CNX INFRA | SHORT |

55.03

|

2008-Jan-09

|

| CNX IT | SHORT |

88.05

|

2000-Feb-21

|

| CNX MEDIA | LONG |

23.79

|

2008-Jan-04

|

| CNX METAL | SHORT |

68.17

|

2008-Jan-04

|

| CNX MNC | SHORT |

11.03

|

2015-Aug-10

|

| CNX NIFTY | SHORT |

14.91

|

2015-Mar-03

|

| CNX PHARMA | SHORT |

9.47

|

2015-Apr-08

|

| CNX PSE | SHORT |

36.96

|

2008-Jan-04

|

| CNX PSU BANK | LONG |

45.62

|

2010-Nov-05

|

| CNX REALTY | SHORT |

91.56

|

2008-Jan-14

|

| CNX SERVICE | SHORT |

15.70

|

2015-Mar-03

|

A brutal selloff across the board…