I recently listened to this a16z podcast, A Guide to Making Data-Based Decisions in Health, Parenting… and Life, that got me thinking on how common personal finance and investing is with diet, exercise and parenting.

They all defy attempts at formulating universal laws.

Take the case of breast-feeding, for example. A truly scientific study on its benefits cannot be done. The data-set of identical or fraternal twins where the mother decided to breast-feed one and not the other for no particular reason (i.e., randomly) is simply not big enough to draw meaningful conclusions. We cannot isolate effects. What we observe are correlations. But correlation is not causation and most of them end up being spurious.

In parenting, oftentimes, we only have a sample-size of one. Most parents are guided by what their parents did and them their’s and so on. Most parenting “rules” are driven by societal norms rather than data. When I was a kid, the doctor advised by parents to substitute water with Coke or Pepsi when they traveled, which was quite often. The rationale was that water could be contaminated whereas bottled drinks are safer. Now, as a new parent, I find myself spending an inordinate amount of time trying to keep my kid away from food with added sugar. So, were my parents or doctor wrong? Should they have rolled the dice on possibly dirty water rather than sugar-water? There is simply no way to know for sure – there is no counterfactual. They simply made the best choice they could with the data that they had. Just like how I am doing with mine.

Try changing your diet. It is possibly the most difficult thing to do. We all know that vegetables are good, processed food is bad, and that we should stay away from sugar and deep-fried food. And yet, most of us will fail at being 100% healthy eaters. Why? Because a diet is a habit. In order to change it, you have to first change the environment, get rid of triggers and replace old shopping and consumption patterns with entirely new ones. A challenge that many of us find insurmountable.

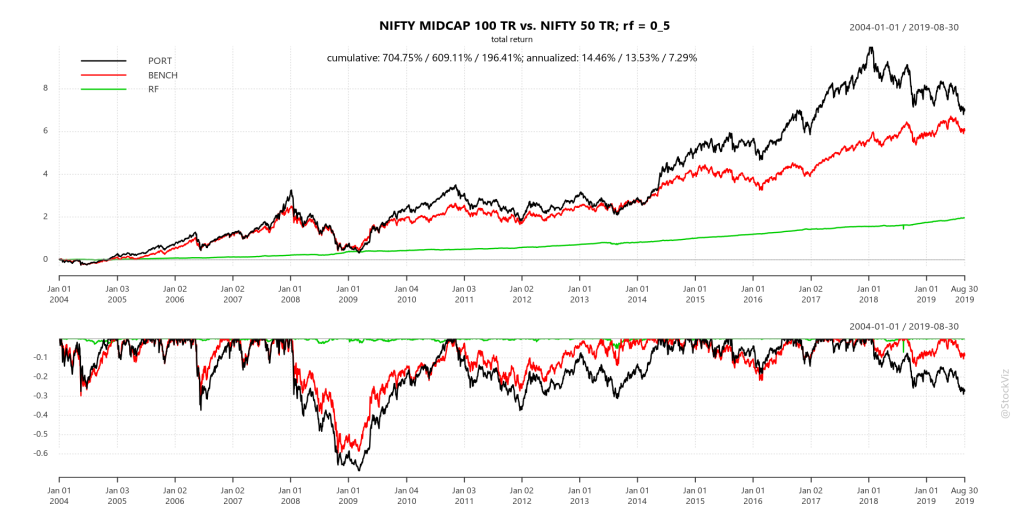

Personal finance and investing have the same problems: more data is not necessarily better, there is no easy way to isolate effects, there is no counterfactual and people have hard but unstated preferences.

Your savings rate is like your diet. An advice to “save more” is as useful as “eat healthier.”

It is easier to believe that vaccination causes autism – a false but bold claim, made authoritatively – than to dive in to the messy data and statistics that back the benefits of vaccination. Just like it is easier to believe in “risk-free” trading strategies than to study one’s probabilities and sequence of returns.

Leading a healthy lifestyle only means that there is less of a risk that you will develop diabetes or get cancer decades later in life. Not zero. And neither is that risk quantifiable. Just like it takes decades for even the strongest investment strategies to play out.

It is also a lot like parenting. You will never know for sure whether you are making the “best” choice for your kids. You are only kind of sure of it once they grow up and start making their own choices.

But thankfully, there is a spectrum of good choices that can be made. The rest is up to the complex-dynamic beast of a system that we call markets… and life.