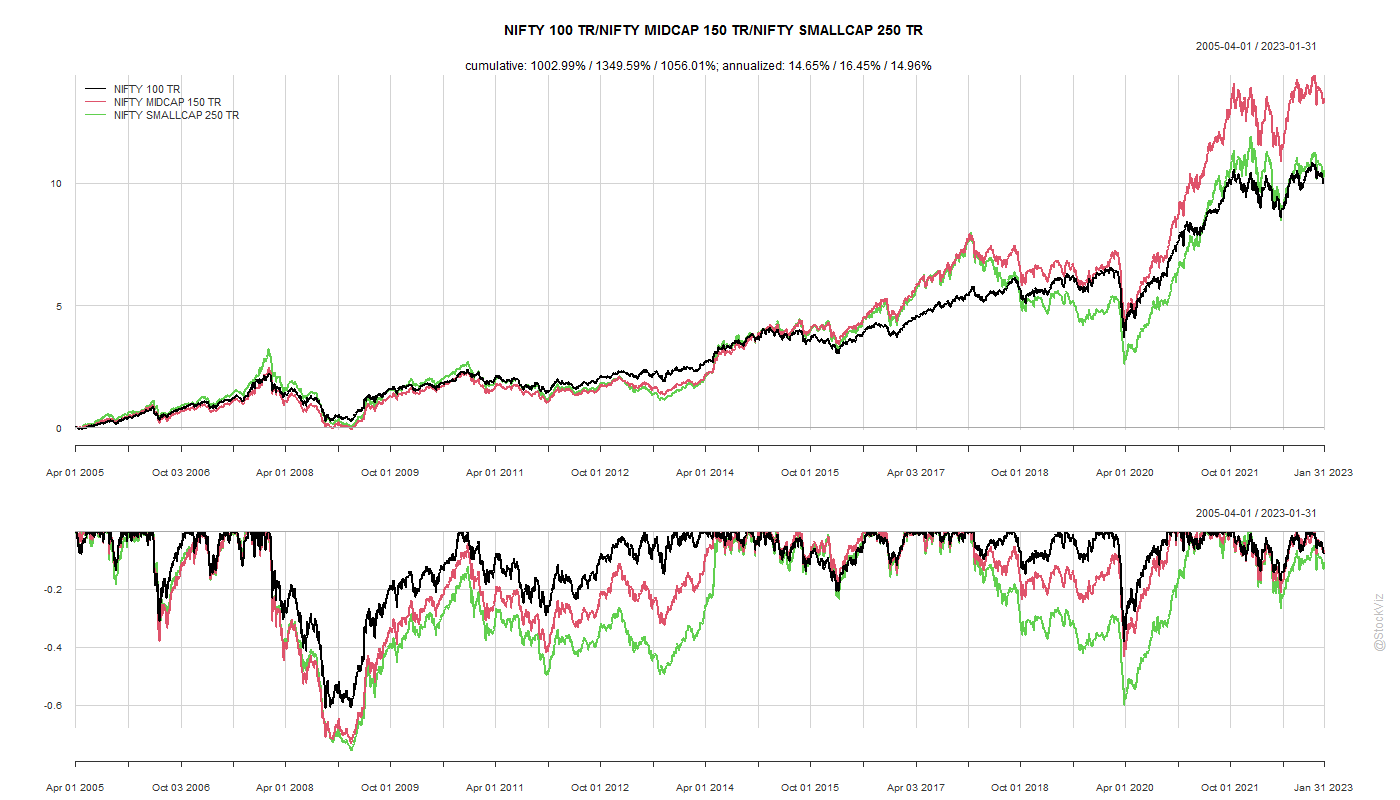

Sharpe Ratios are often used to sort through competing investments. It is the original “risk adjusted returns.” It’s a mathematical expression of the insight that excess returns over a period of time may signify more volatility and risk, rather than investing skill (investopedia, wikipedia).

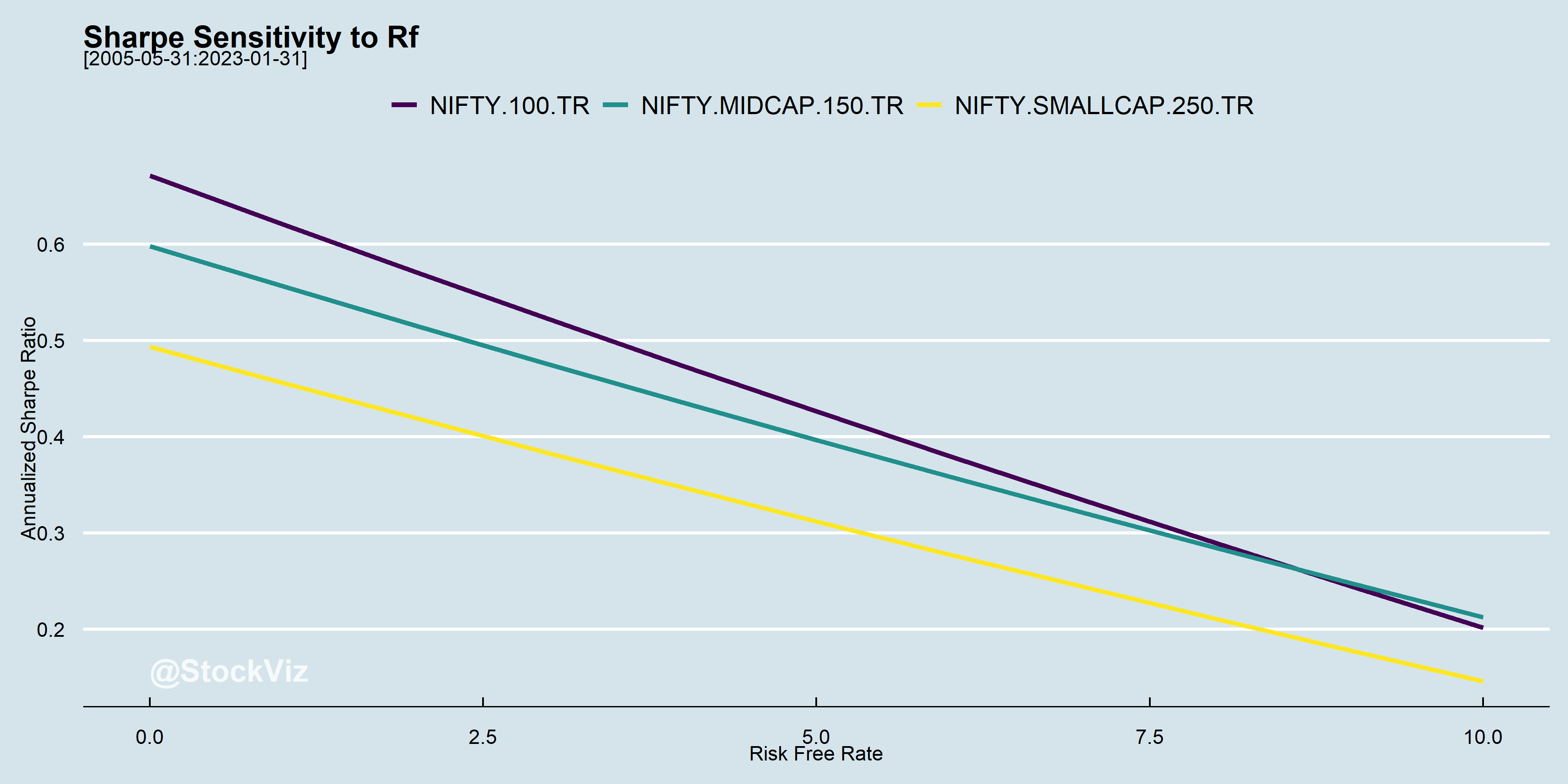

Rb or Rf, the risk-free return, is usually cumbersome to handle. So, typically, it is either set to zero or a constant value. The problem is that rates vary over time and has an impact on the relative ordering of investments.

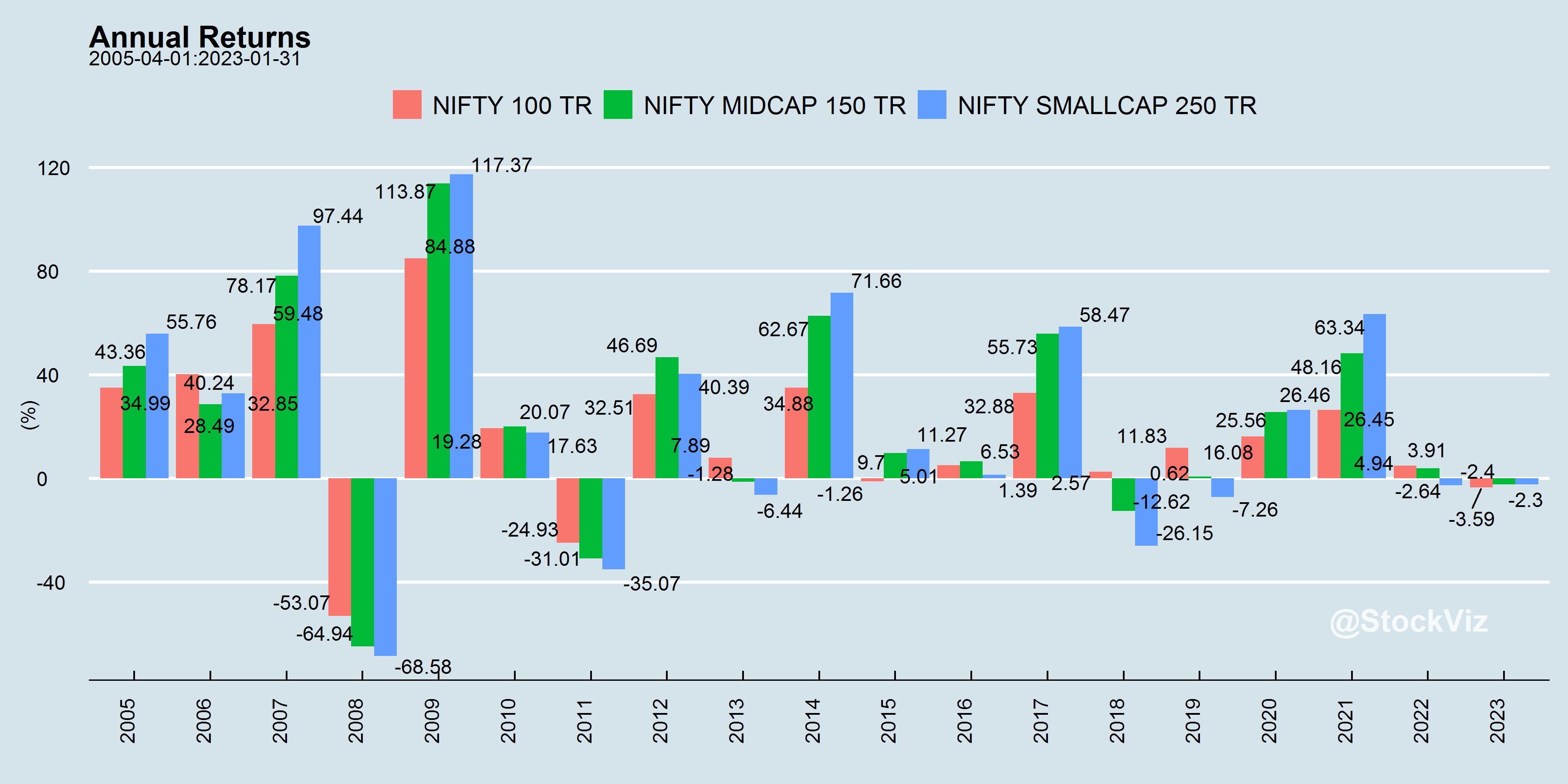

At high interest rates, SR(mid-caps) > SR(large-caps)

Ideally, you want your Sharpes to be positive and stable. Unfortunately, that is never the case.

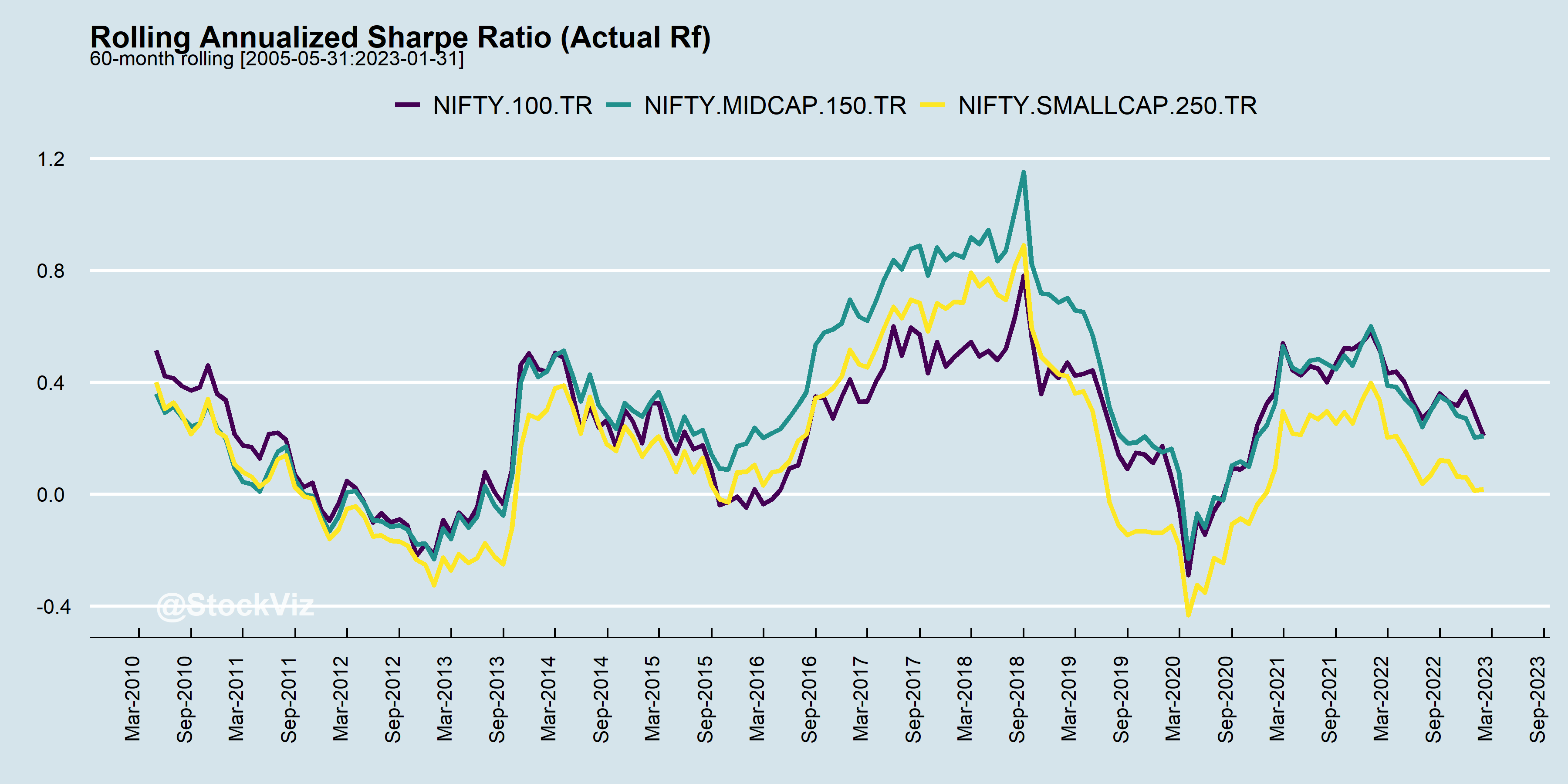

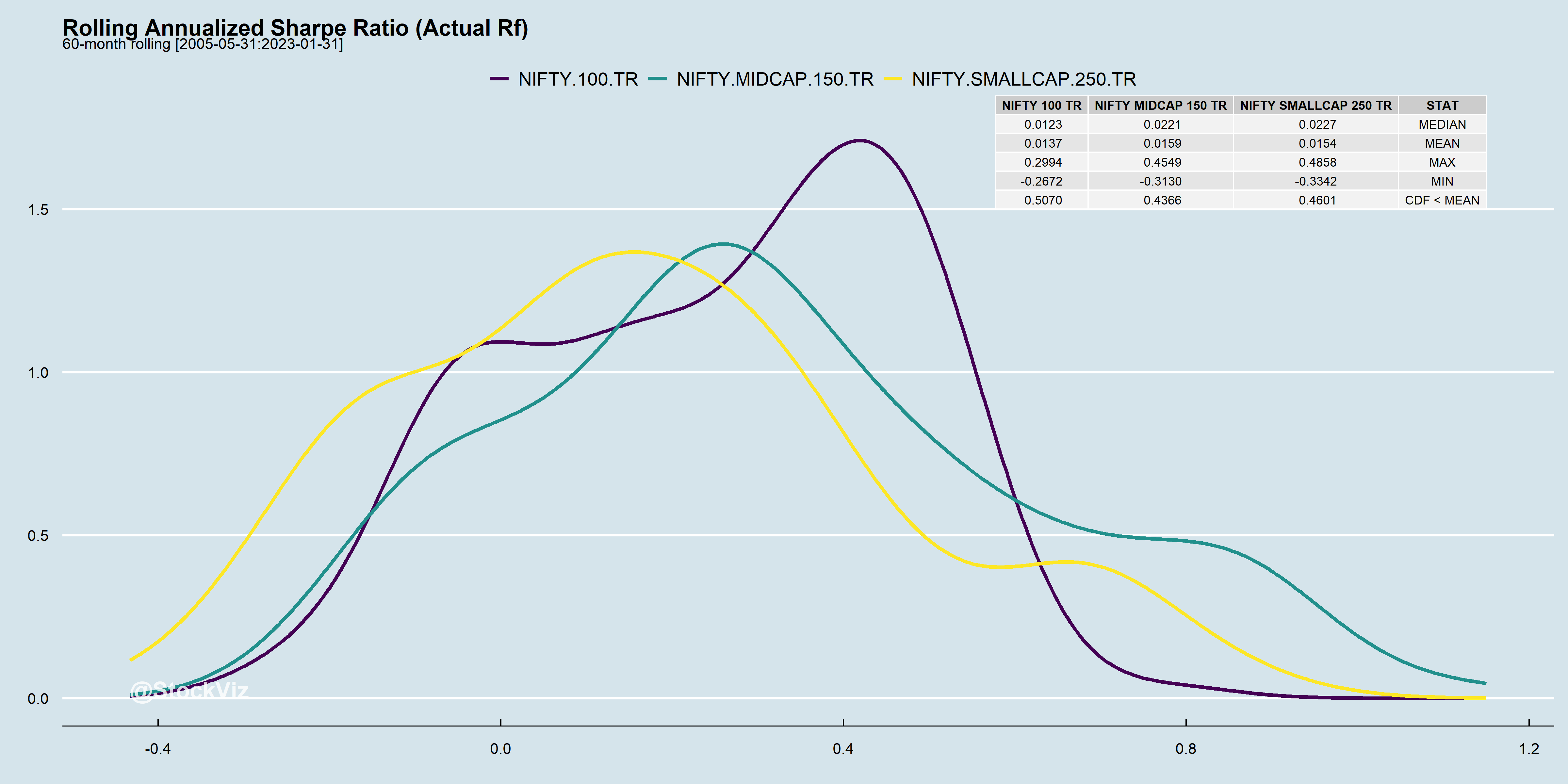

During bull markets, Sharpes trend up and reverse course in bears.

At the end of the day, it boils down to whether the returns are worth the risk.

You might very well be trying to catch lightening in a bottle.

For more index stats, visit our Index Metrics dashboard.

In our introduction to factors, we discussed how portfolio returns are mostly explained by market risk (rm – rf: market risk premium.) Whatever cannot be explained by the market is α, or the portfolio manager’s skill. If you strip away the financial jargon, this is nothing but linear regression.

Also, what exactly is “market risk?” A few years ago, the only index funds on the market were of the NIFTY 50 and MIDCAP 150 indices. However, the number of index funds keep ticking up and there are now several strategy funds covering quality, value, low-volatility, momentum, etc… in the market. So, if an investor can access these vanilla strategies at a low cost, shouldn’t the definition of the “market” expand to incorporate those?

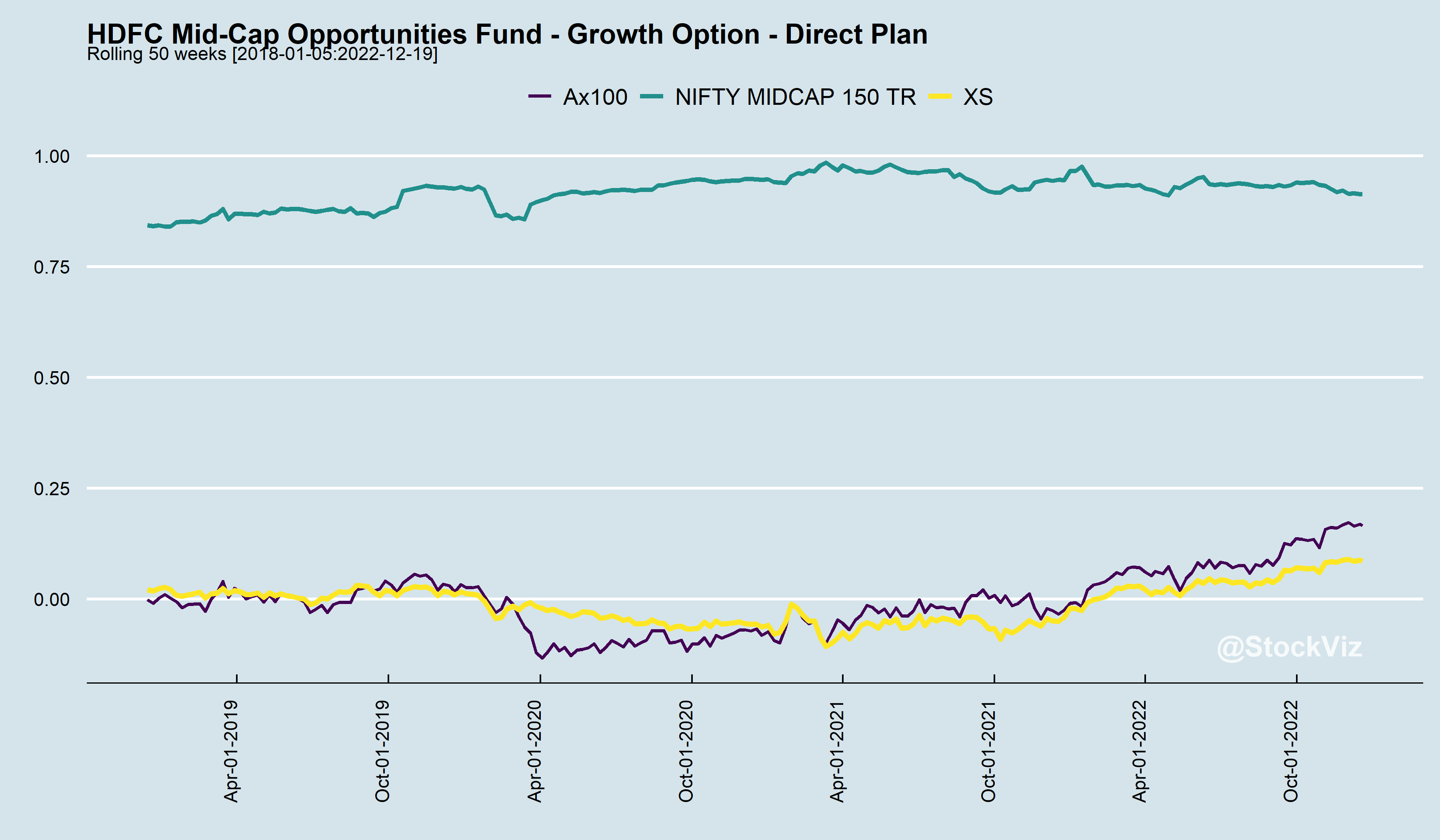

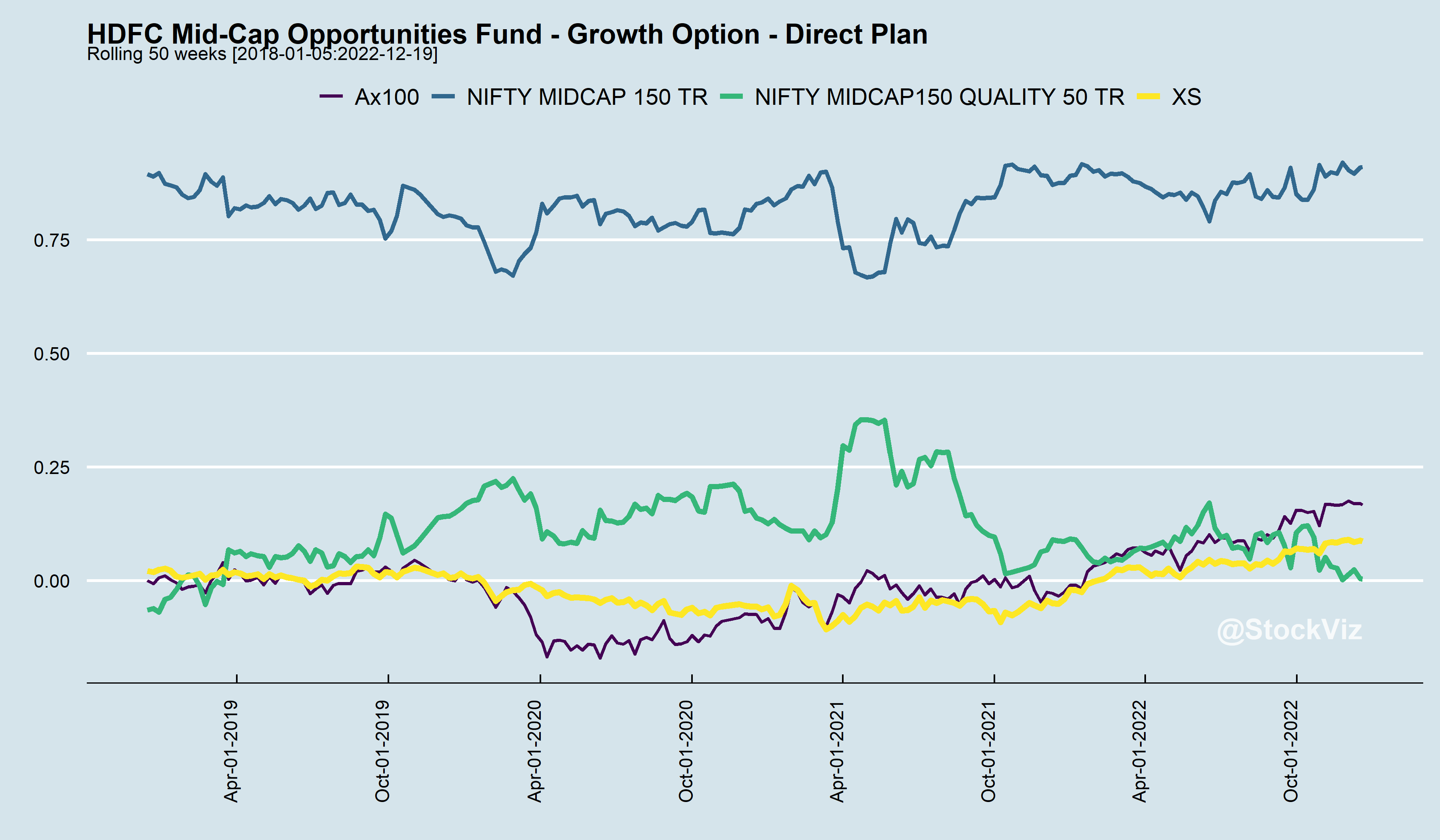

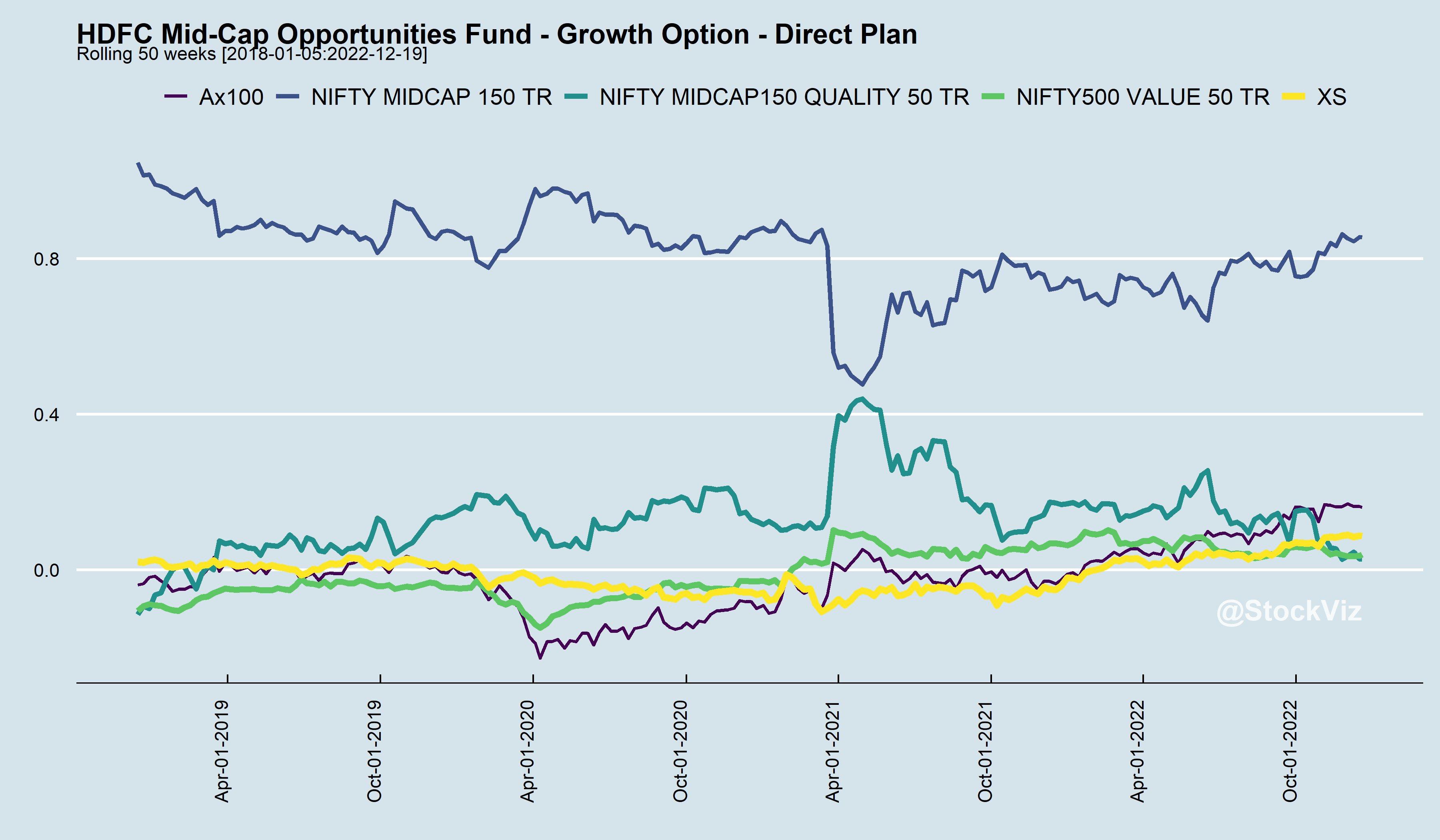

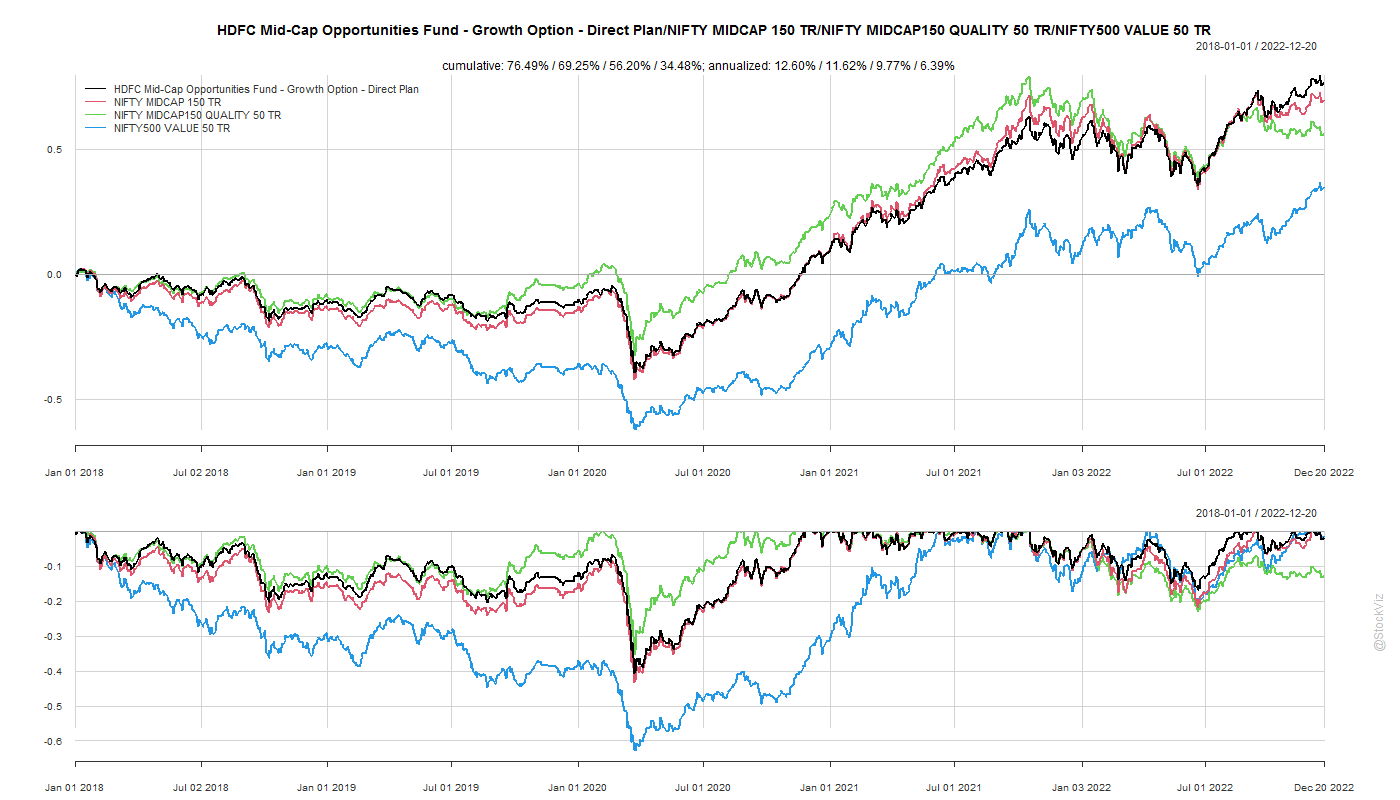

For example, take the HDFC Mid-cap Opp. Fund. You could regress its returns against the NIFTY MIDCAP 150, the NIFTY MIDCAP150 QUALITY 50 and NIFTY500 VALUE 50 indices to get an idea of how its α over them has evolved over time.

Rolling regressions gives you an idea of portfolio tilts and the fluctuating nature of α (Ax100). Also, its worth noting that α is only tangentially related to excess returns (XS). There are periods here where XS was positive in spite of negative Ax100 and vice versa.

Styles go in-and-out of favor. Sometimes Quality performs better than Value and sometimes a simple cap-weighted index will outperform everything else. An actively managed portfolio’s relative performance to these styles change over time as well.

tl;dr:

α is a statistical derivation.

Don’t go chasing α – it keeps fluctuating.

α is not the same as excess returns.

When in doubt, index and forget.

You are always in doubt.

We have setup a script that auto-updates every day with these regressions on select large-cap and mid-cap funds. The report is available here.

Investors love the returns of momentum strategies but hate its crashes. And there have been numerous attempts at making momentum investing smoother. After all, where there is demand, supply will be created. But, what if, momentum and crashes are two sides of the same coin? Is Momentum without crashes even possible? What if Volatility is Nature, not Nurture?

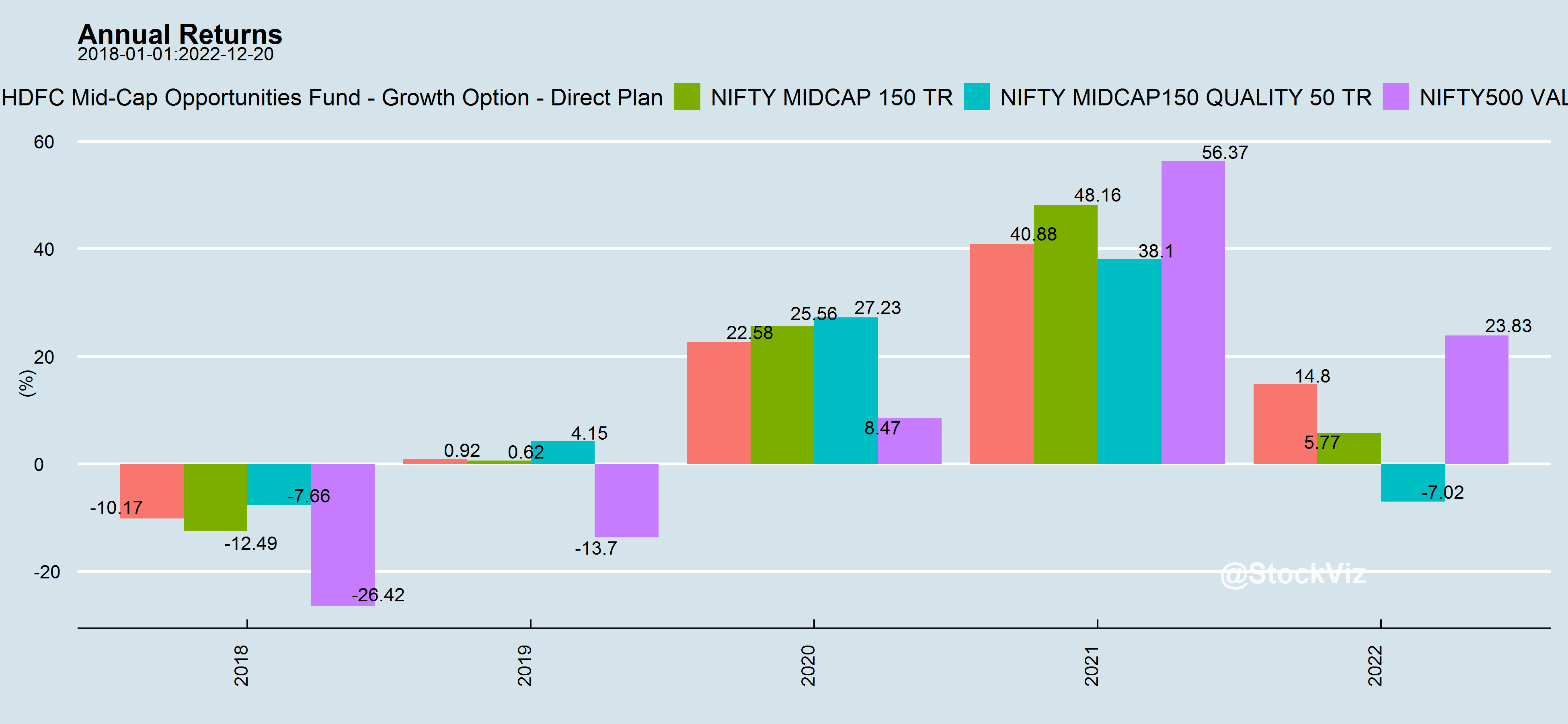

Last year, we had a look at the The High-To-Price (HTP) Momentum Strategy (backtest, live model). It lived up to its promise of low-drawdowns by staying in cash during the most recent market downturn. However, if it ends up being slow to react to market recoveries, then it will underperform at the beginnings of new bull-markets. It is yet to go through a full cycle (bull-bear-bull) for us to be 100% confident about it.

More recently, we back-tested trend overlays on momentum strategies (Part I, II, III). It is still early days.

Broadly, the biggest problem with the momentum strategies is that they are path agnostic – they all look only at asset returns. The raw signal treats a stock making a parabolic move and a stock making a gradual climb the same. The filters come in later. What if there was a way to incorporate the path as well?

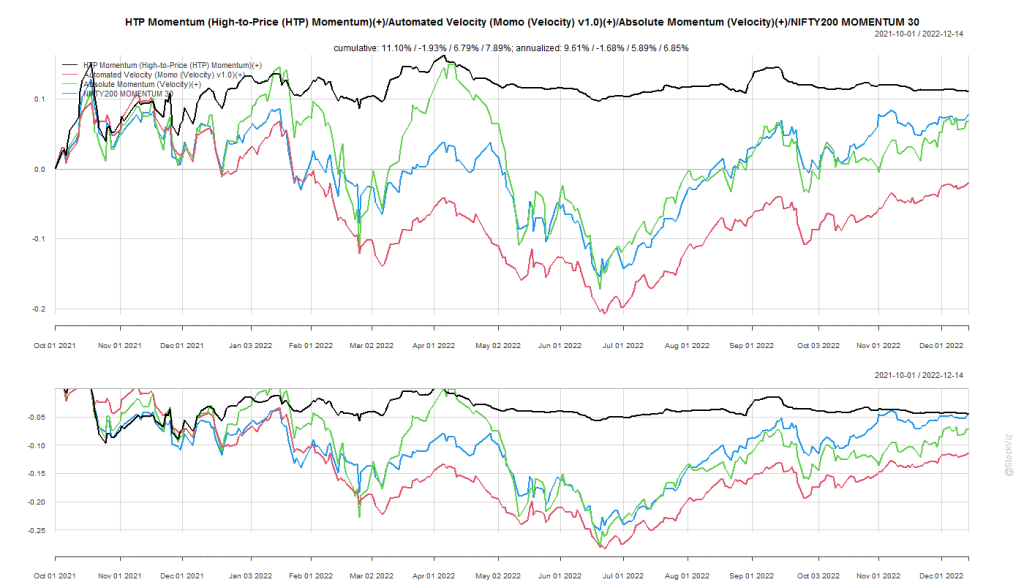

We took a shot at this problem with our Dynamic Linear Model strategy that simply regressed prices to a 45* line and ranked them based on goodness of fit. The performance has been good but not great.

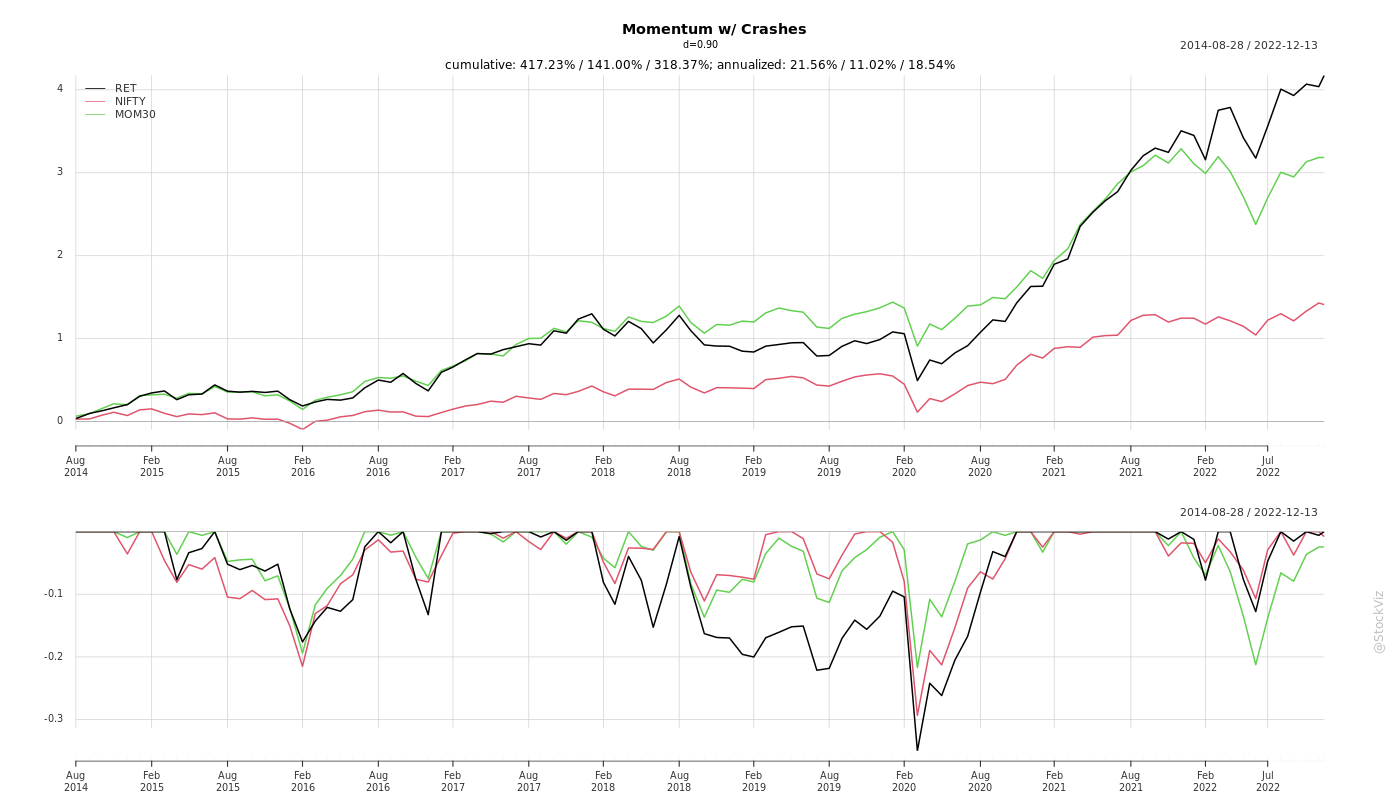

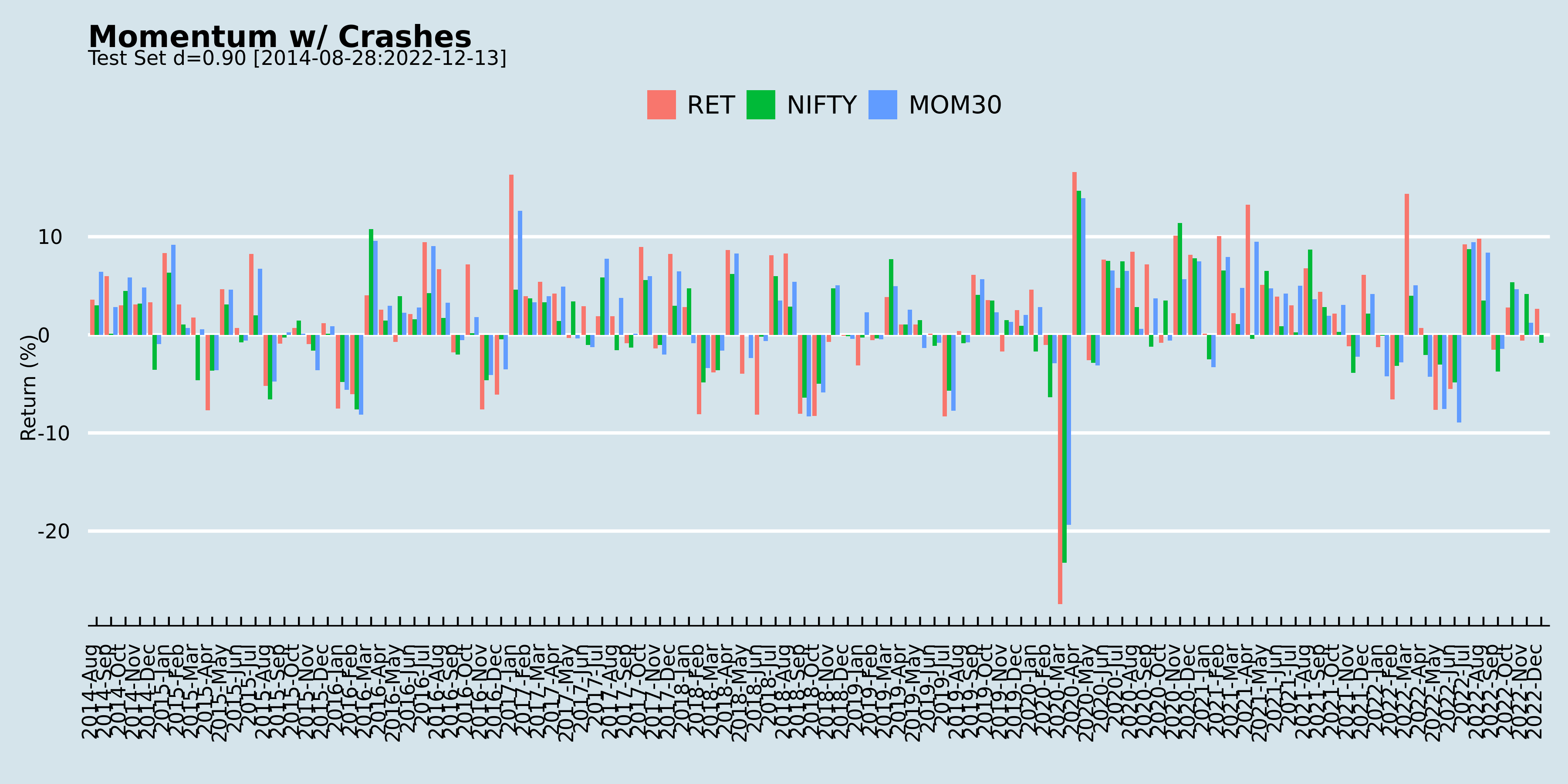

So, it was with great expectations that we teared through Momentum Without Crashes (SSRN). The authors take a fractional differencing approach to overcome the loss of path information. The fractionally differenced log price series is i.i.d. so the next period prediction of the differenced series is simply the mean of the series. This “predicted value” is then inverted to arrive at a prediction for the next-period log return. These predicted log returns are ranked and a portfolio is constructed. The differencing parameter d is computed empirically. Intuitively, d=1 will result in a traditional momentum portfolio and d=0 yields a reversal portfolio. The authors find that d=0.9 is optimal.

Back-test

We did a full-sample back-test on monthly returns for the top 200 stocks by free-float market-cap between 2014 and now for d=0.9.

The Fractional Momentum strategy, as the authors call it, out-performs the NIFTY 50 index and the NIFTY 200 Momentum 30 index. However, it does have its periods of under-performance and it doesn’t quite live up its promise of avoiding crashes.

The approach is pretty interesting and they have tested it across multiple markets so we created monthly-rebalanced and momo versions of this strategy to see how it tracks in the real world.

You can find the charts for d in [0, 1] on github.

Previously, we discussed how applying a trend filter to a midcap momentum index could make sense. Then, we extended that to our homegrown momentum models. In both cases, there are certain situations where trended momentum side-steps deep drawdowns. However, if you are only looking at “raw” returns, you would be better off with monthly rebalanced momentum versions.

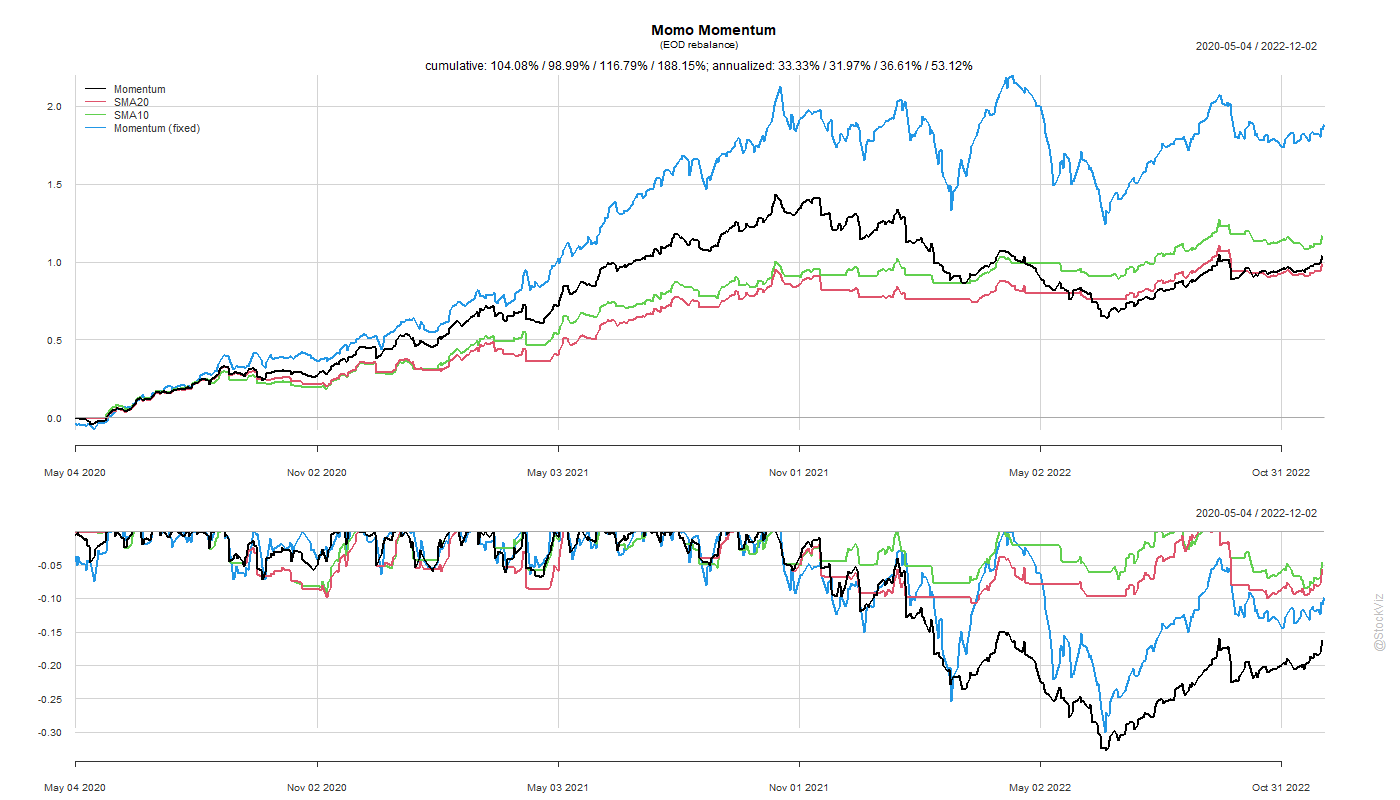

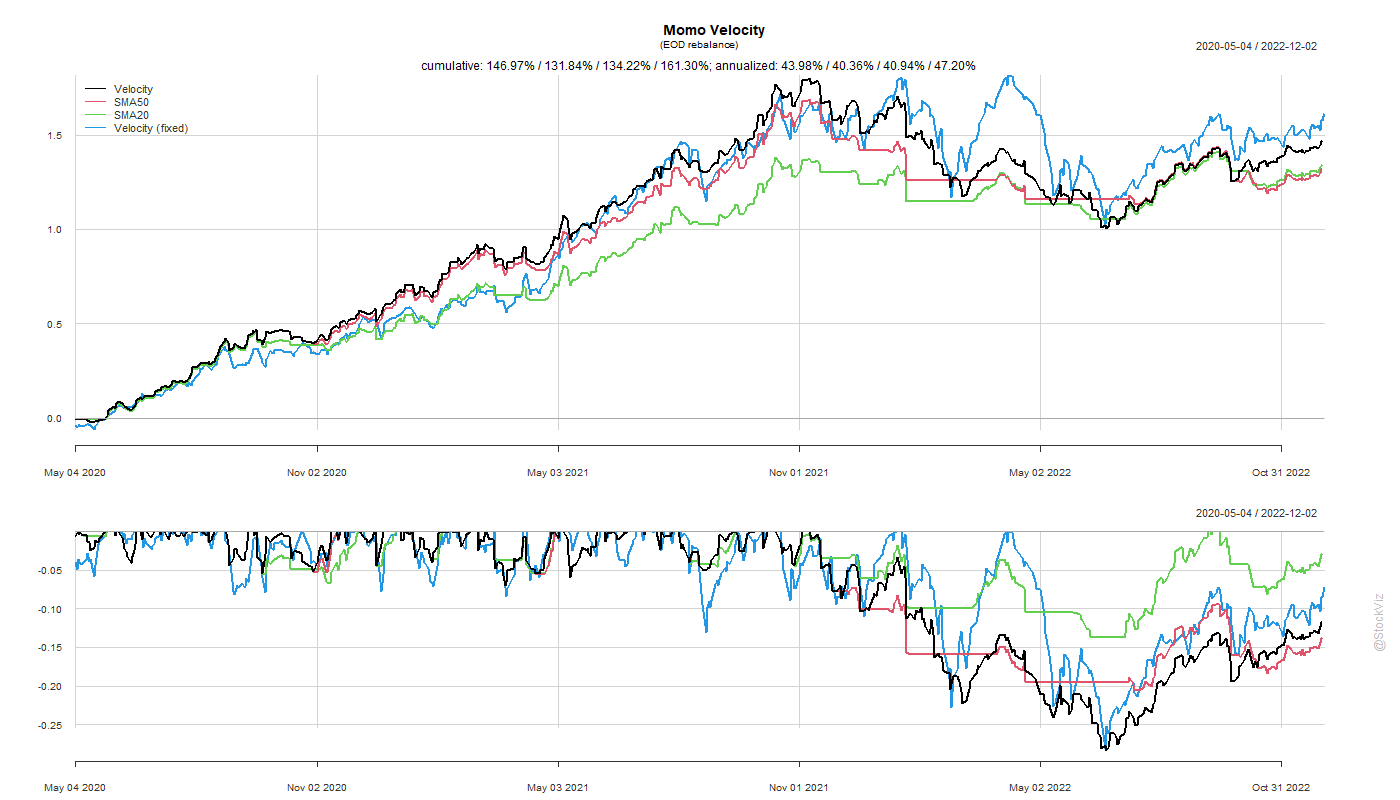

In this post, we run a similar test on the Momo versions of our homegrown momentum models.

Momentum (momo)Velocity (momo)Acceleration (momo)

The problem with high turnover strategies, beyond transaction costs, is the higher operational risk it entails. You could probably get away with postponing trades by a day or two in the monthly rebalance strategies but with these, you need automated trading systems.

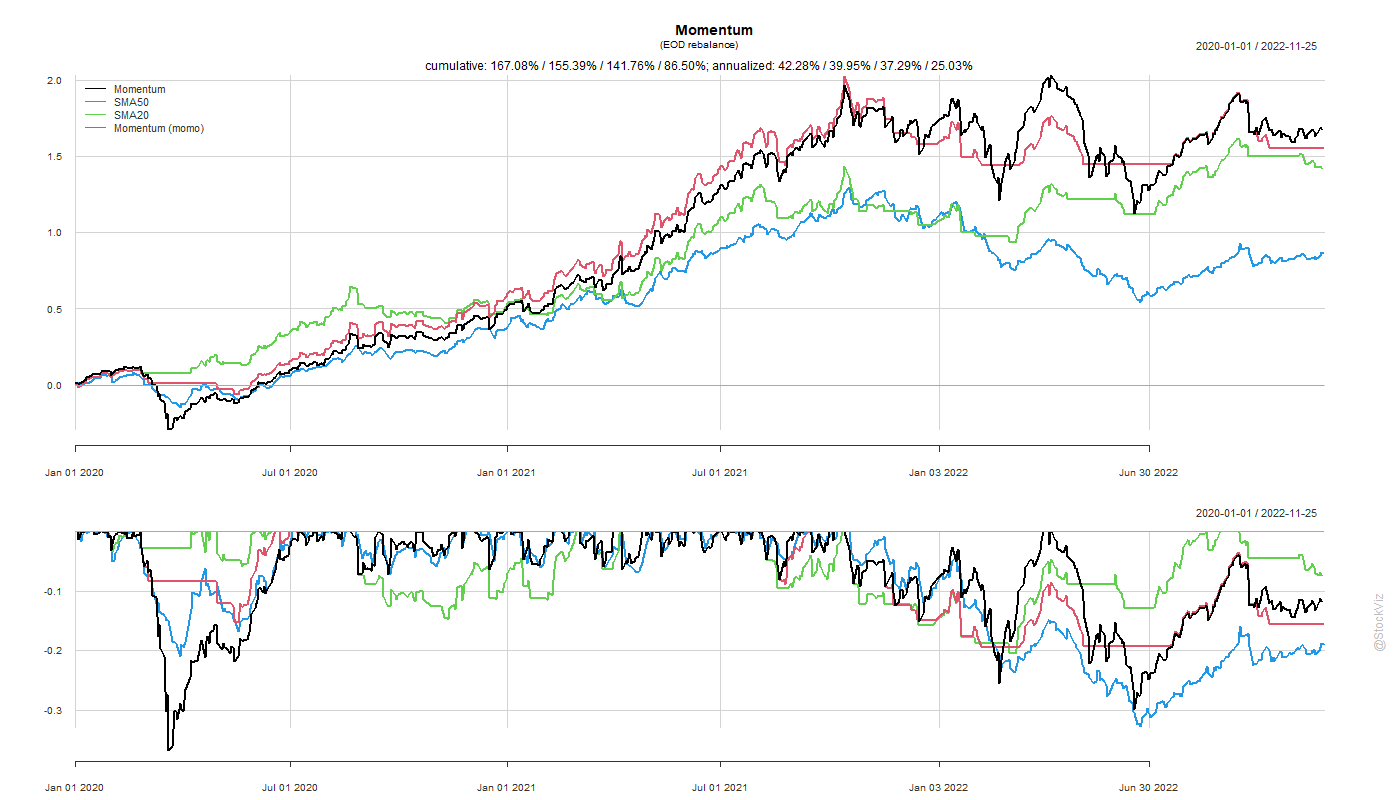

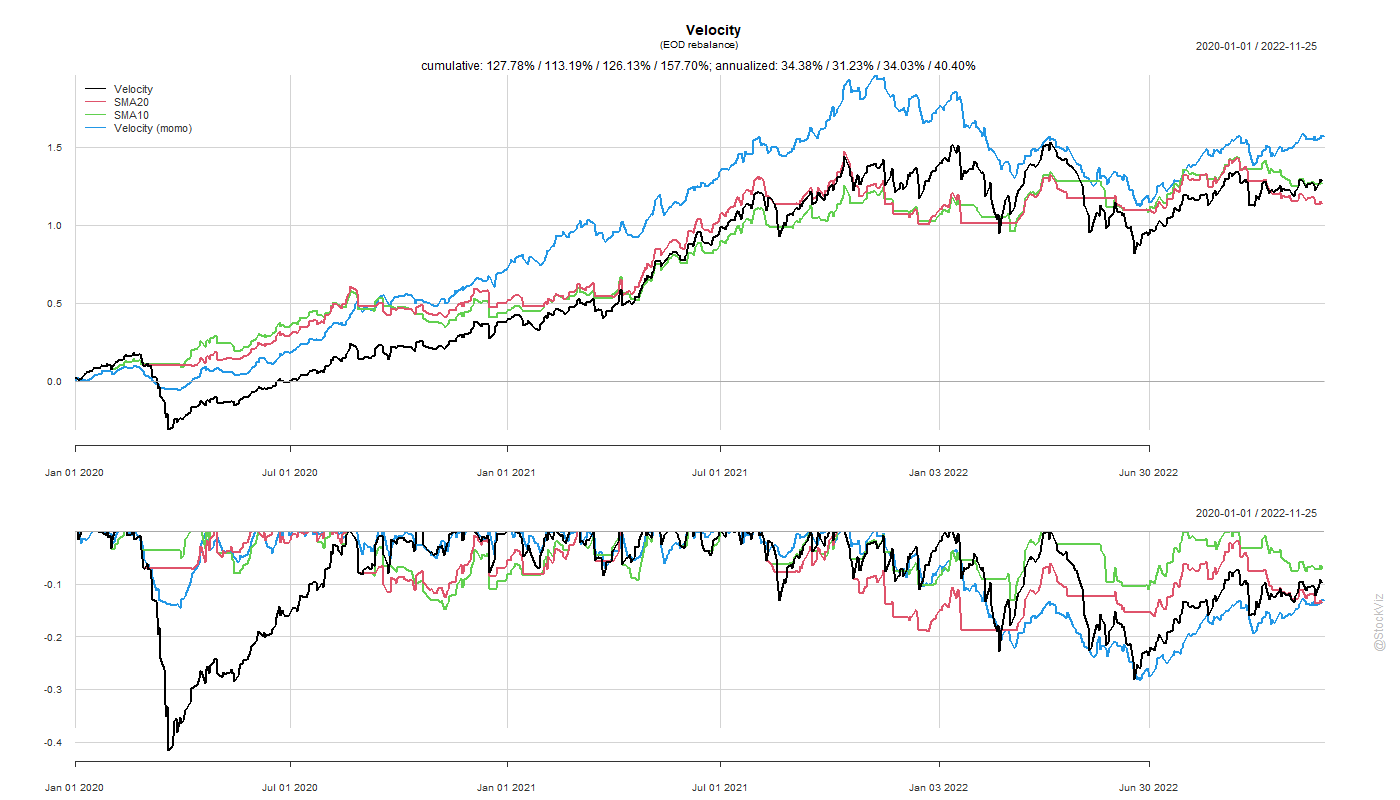

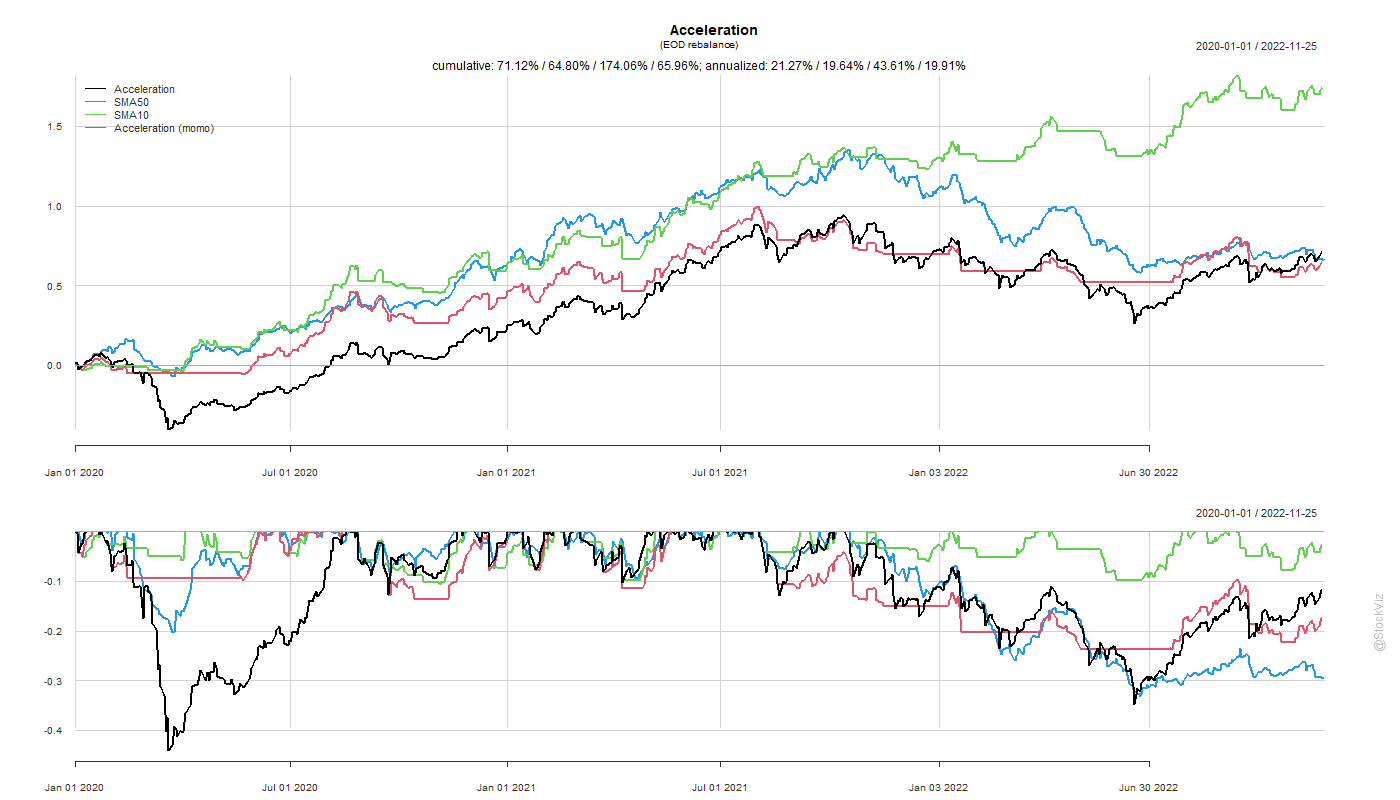

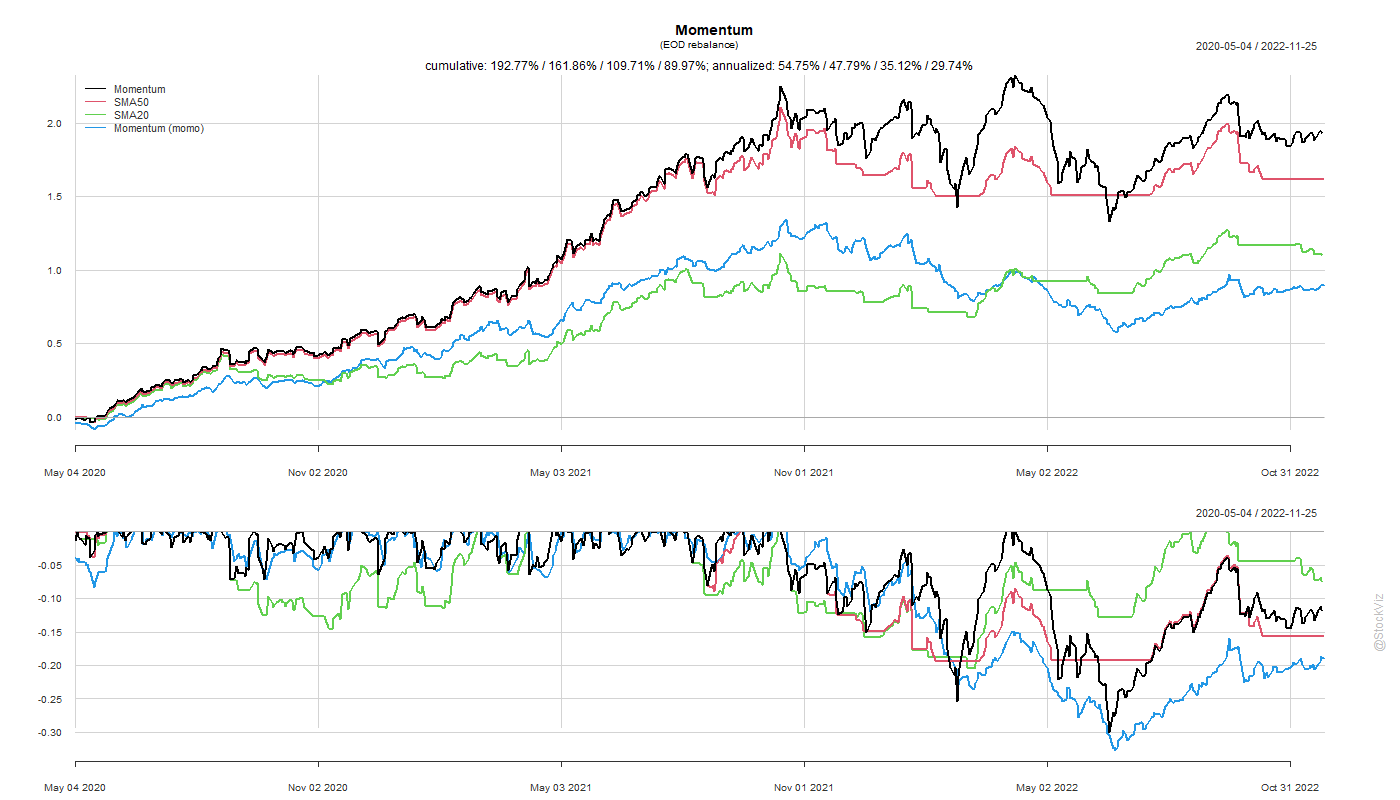

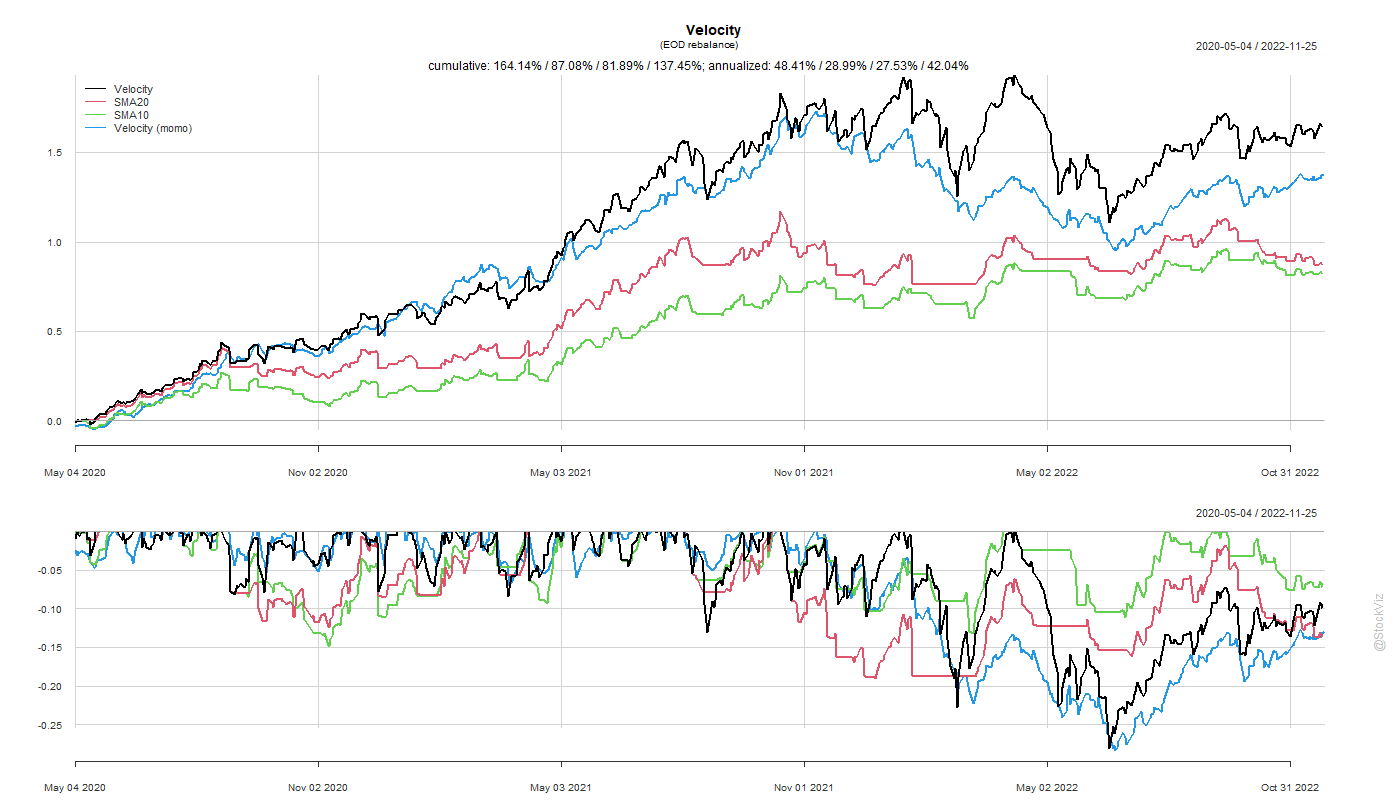

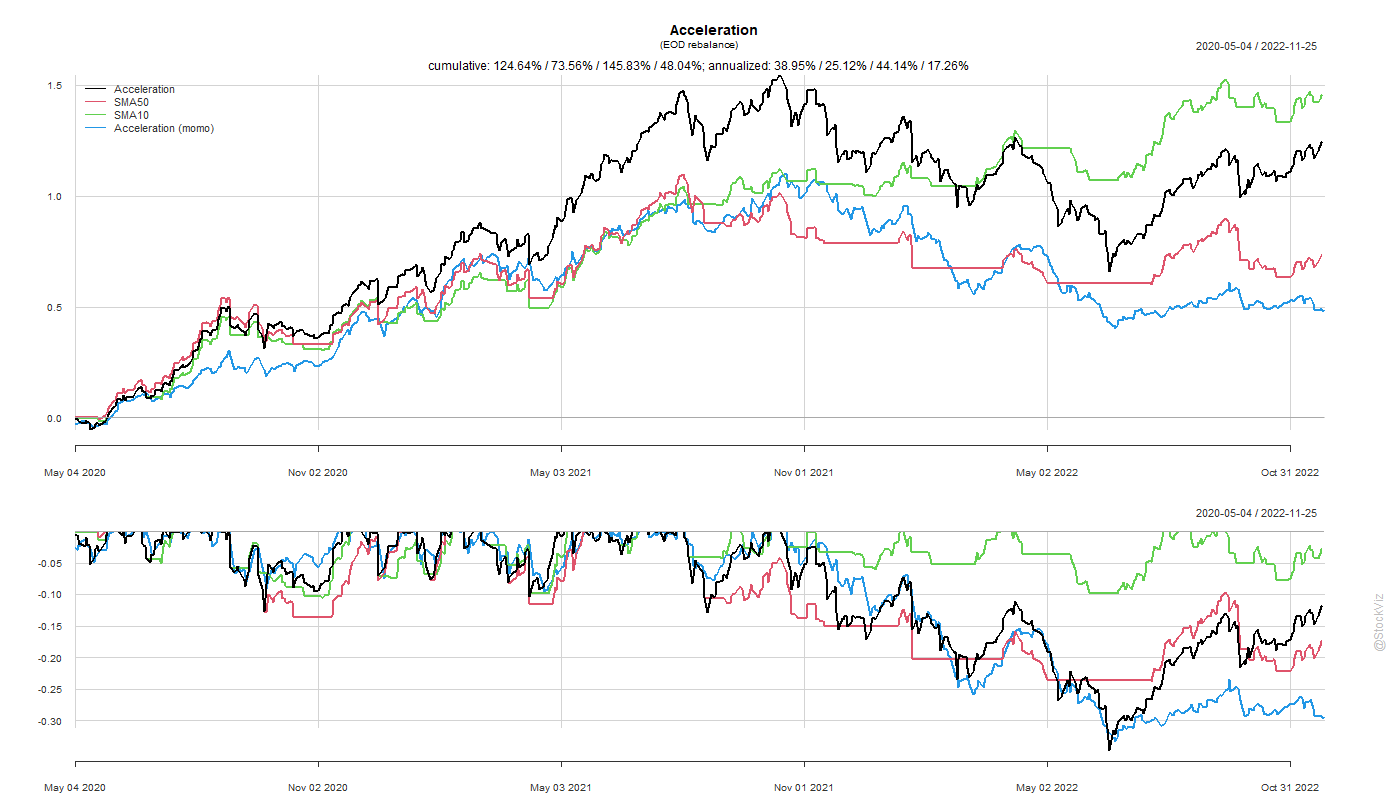

Momentum is known to trend. Our previous post explored trend overlays on momentum indices. The question now is, does it make sense to do the same to our own homegrown momentum models?

While these momo strategies do well with sudden market crashes, the problem has always been markets that grind down. Does a trend overlay on the original strategies perform better than momos after transaction costs?

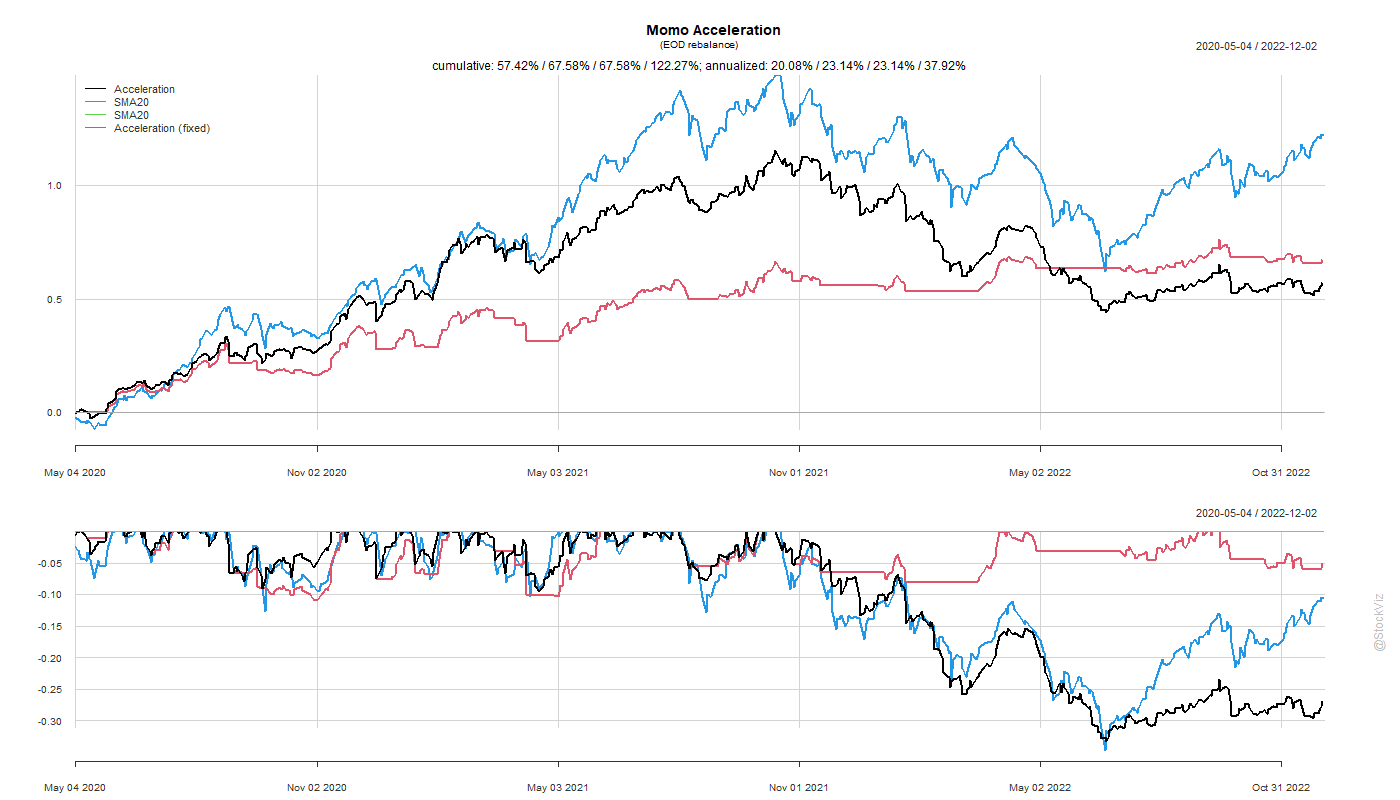

MomentumVelocityAcceleration

The trend-overlay strategies seem to avoid drawdowns and perform better than their momo counterparts. The post-2020 Corona Crash market rally was one for the record books. So, a strategy that sidesteps the crash may not necessarily perform better during the rally but the full dataset will show superior performance. What if we took the crash data out of the picture?

MomentumVelocityAcceleration

It looks like Momentum and Acceleration strategies saw big pickups in performance. A trend overlay on Velocity resulted in lower drawdowns but that came with a big performance penalty.