Popular indices, like NIFTY 50 & MIDCAP 150, are useful if you are benchmarking long-only portfolios. However, if you have a long-short portfolio, then you need a long-short benchmark.

When Are Contrarian Profits Due To Stock Market Overreaction? (Lo, MacKinlay, 1990) describes a naïve portfolio construction process that is fit for purpose.

For momentum, portfolio weights are in proportion of excess returns over an equal-weighted index and for mean-reversion, they are the inverse.

For example, if you subtract the returns of each of the components of the NIFTY 50 index with the returns of NIFTY 50 EQUAL-WEIGHT index and divide by 50, you end up with the portfolio weights for the next day. Each look-back period used to calculate returns will produce a different set of weights (and a different synthetic index.)

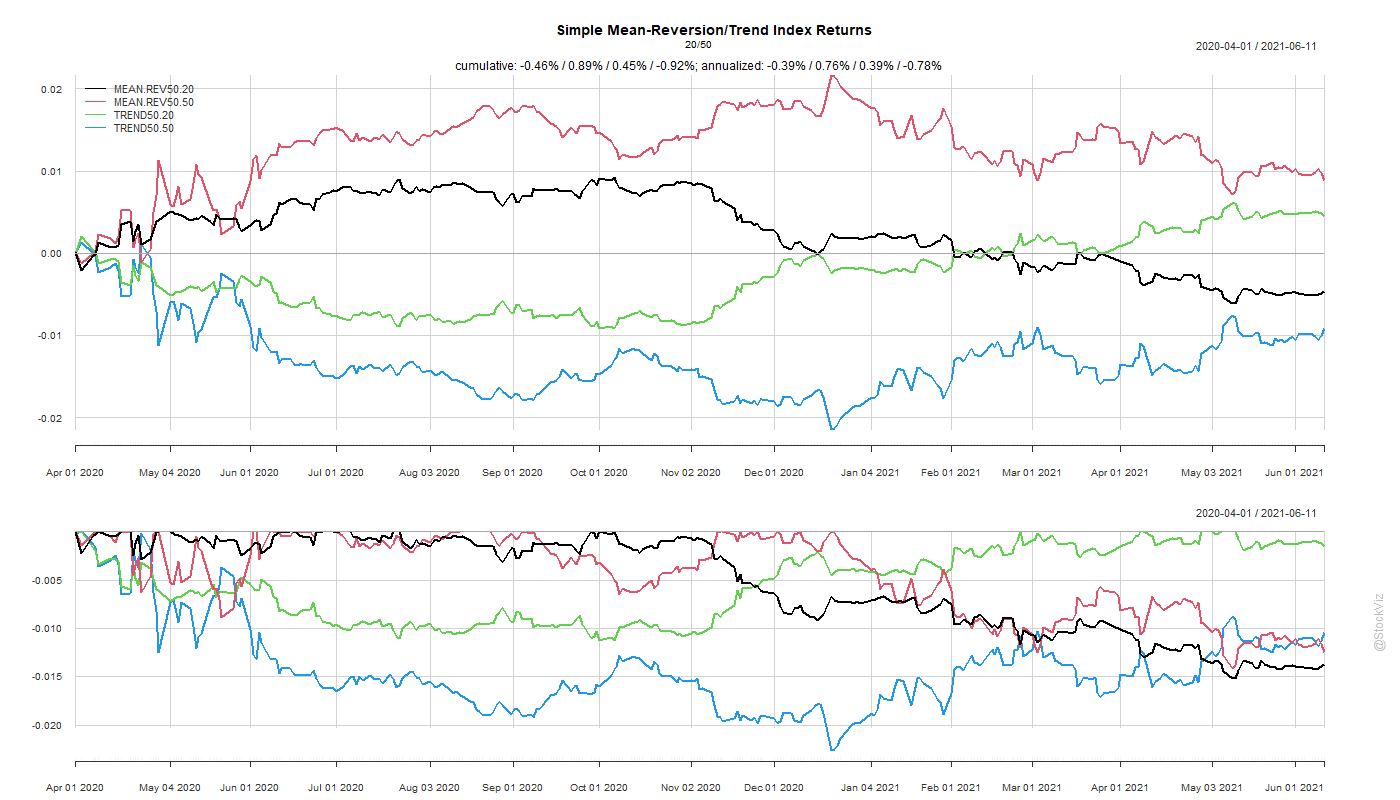

As impractical as constructing such a portfolio may seem, they are useful as a benchmark for long-short mean-reversion/momentum portfolios. Here are index returns since April 2020 with 20- and 50-day look-backs.

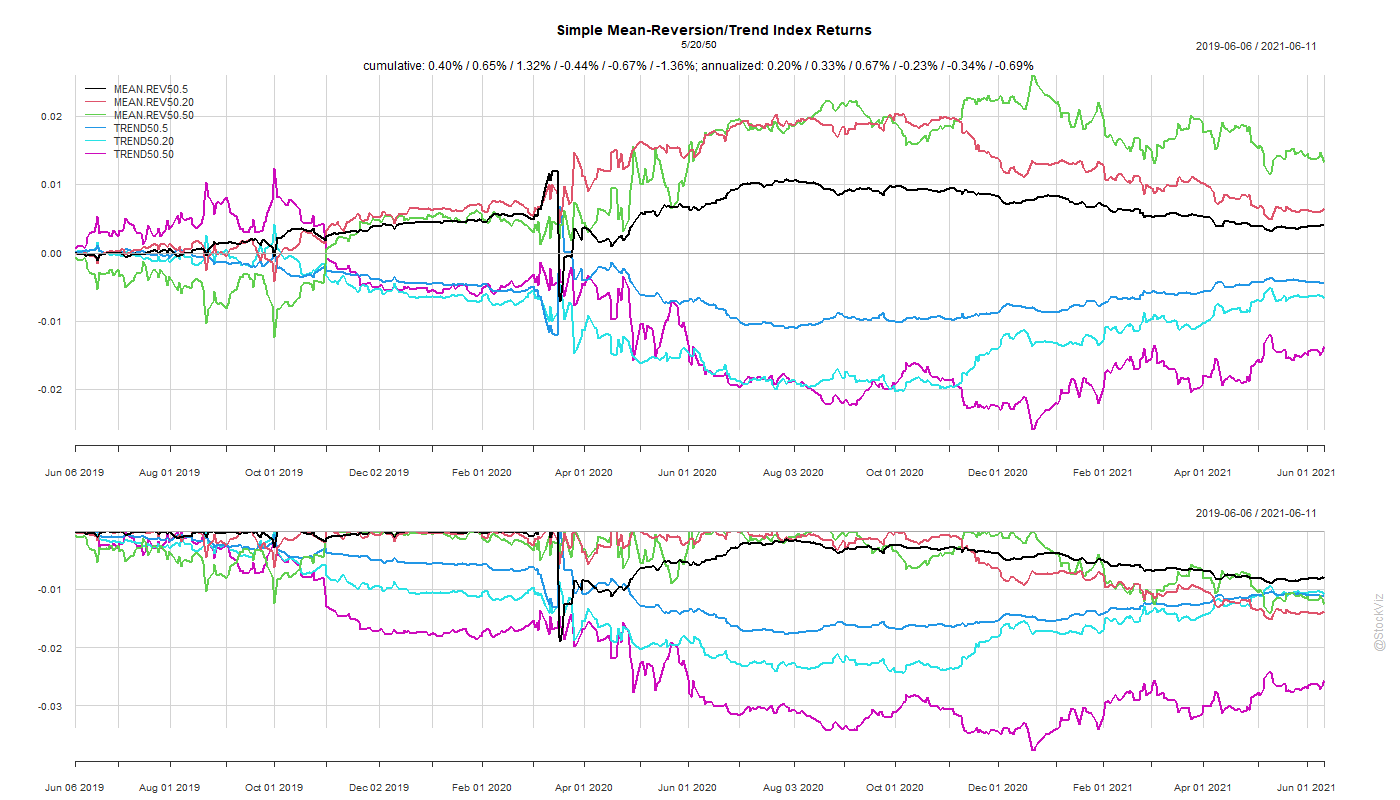

This is especially interesting if you are looking at market dislocations and subsequent recoveries. Here are indices since June 2019 with 5-, 20- and 50-day look-backs.

Counter-intuitively, naïve mean-reverting long-short seems to out-perform momentum.