The book Following the Trend: Diversified Managed Futures Trading, Andreas Clenow, describes a simple “breakout” strategy:

If today’s close is higher or equal to the highest close in the past 50 days, we buy tomorrow; if the close is below or equal to the lowest close for the past 50 days, we sell open tomorrow and go short. A similar logic is used to get out of positions, where a long trade is sold when the close reaches the lowest point in 25 days and a short trade is covered when the price makes a 25-day high.

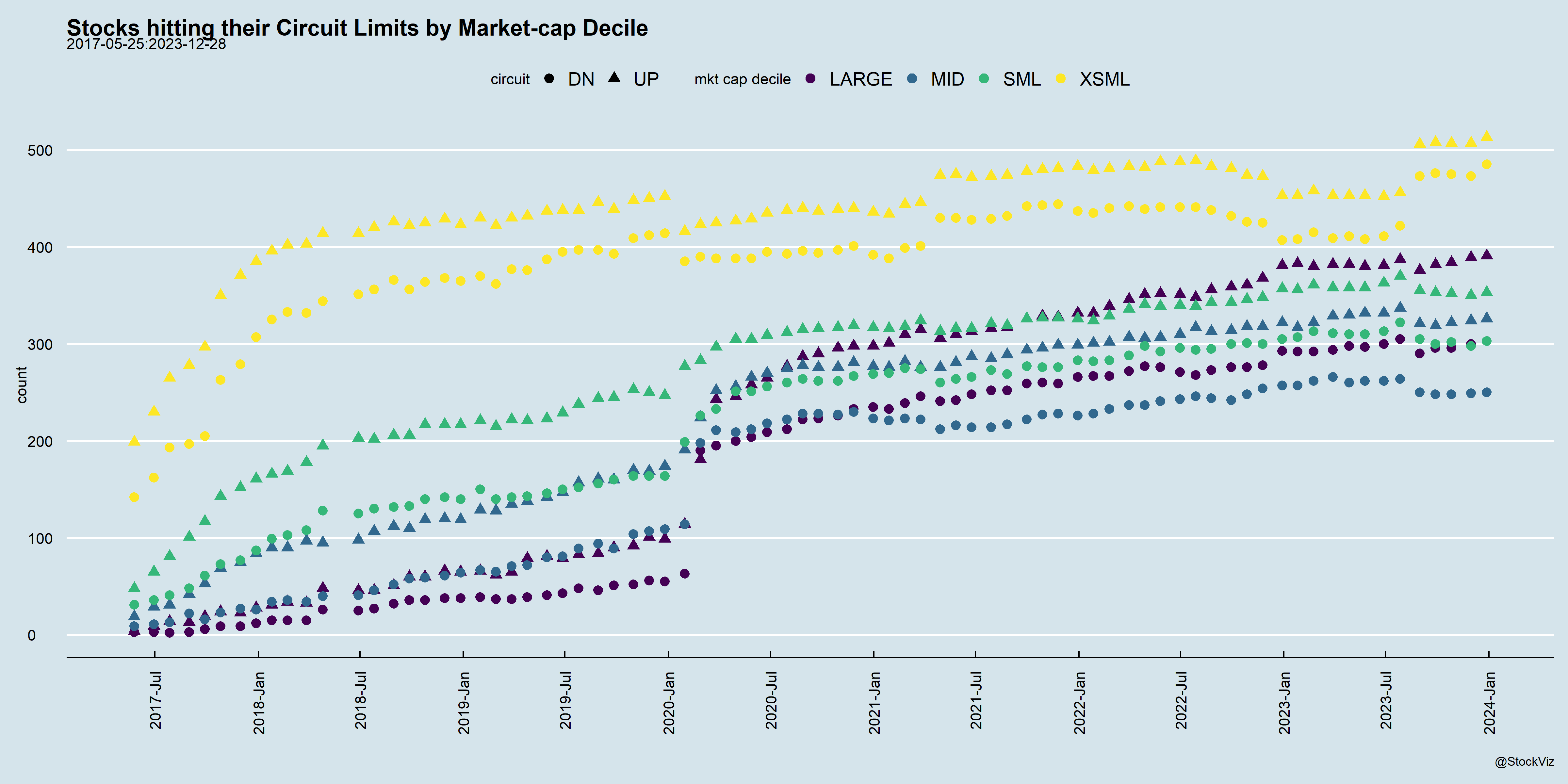

The book was published more than a decade ago and traders would’ve moved on from the basic strategy it described. However, we were curious if it ever worked at all on Indian indices. So, we ran a backtest.

Turns out, it never did.

Layering a trend filter seems to help a little.

While the strategy avoids some really steep drawdowns, the backtest doesn’t consider trading costs, taxes, etc.

While you could data-mine and get to a bunch of parameters that might work for “trading breakouts”, there is no reason why it should continue to work in the future.

Code and charts for other indices are on github.