This is a continuation of Lumpsum vs. Dollar Cost Averaging (SIP) that modeled different return series and concluded that a prudent investor would be better off with a SIP because of a smaller probability of incurring a large loss. However, we stopped short of comparing different indexes to see if the conclusion held.

The ‘average’ return

What happens if we take the average weekly return of an index and create a synthetic index that just gives those average returns without any variance? We end up with a parabolic looking cumulative return profile below:

/cumulative.raw.NIFTY%20SMLCAP%20100.png)

The small cap index was chosen on purpose to illustrate how ‘average’ returns relate to real returns on an extremely volatile index.

The average return series is, of course, a fantasy. What we are interested in is in the probability of getting those returns.

Probabilities

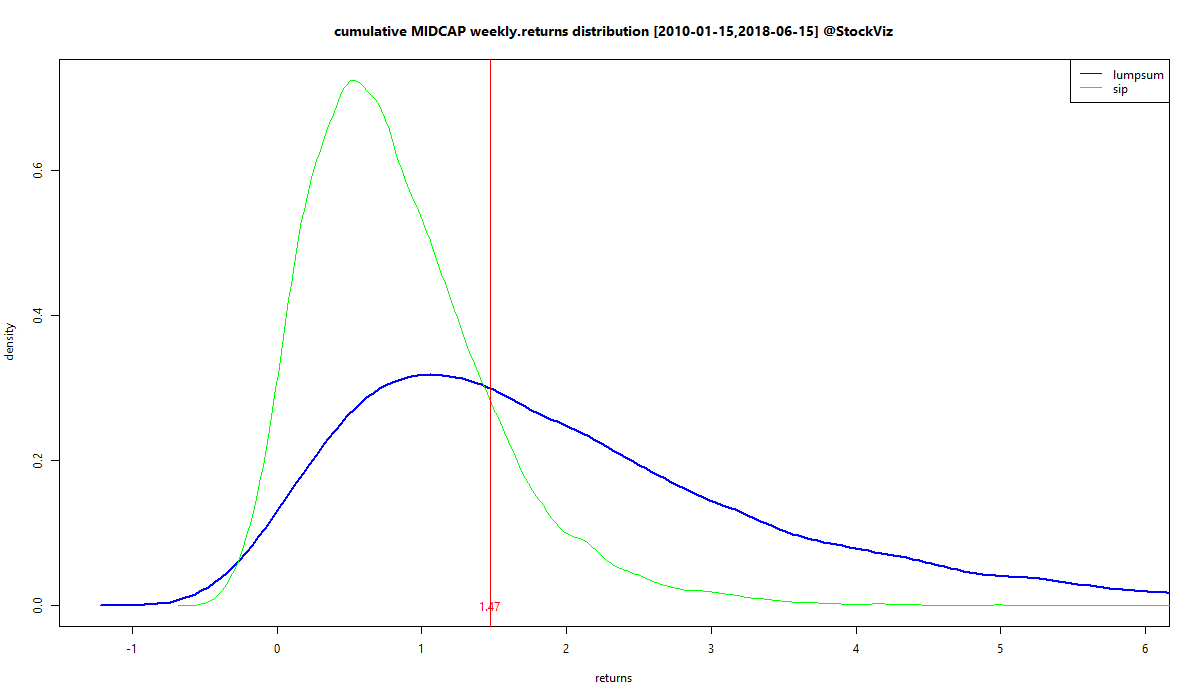

Just like our first post, we start by modeling the returns of the NIFTY 50, MIDCAP and SMLCAP indexes as a Generalised Lambda Distribution and running a 10,000 path simulation to obtain a series of DCA vs lumpsum investment returns. We then feed that into a empirical cumulative distribution function so that we can query it for probabilities under different thresholds. To put that in a picture:

/cumulative.simulation.avg.NIFTY%20SMLCAP%20100.2004-01-09.2018-09-28.png)

The vertical lines mark the different thresholds we are interested in.

- The grey line on the left is at zero. We have SIP showing a 4.44% probability of negative returns and lumpsum showing 3.49%. Yes, there is a non-trivial possibility that SIPs will give negative returns. However, looking at the shapes below zero, SIP losses may not be as large as lumpsum losses.

- The red line in the middle is the start to finish return of the index. Here, we have SIP showing a 22.69% probability of exceeding those point-to-point returns and lumpsum showing 57.50%.

- The orange line on the right is the compounded ‘average’ return. We have SIP showing a 7.82% probability of exceeding that and lumpsum showing 37.20%.

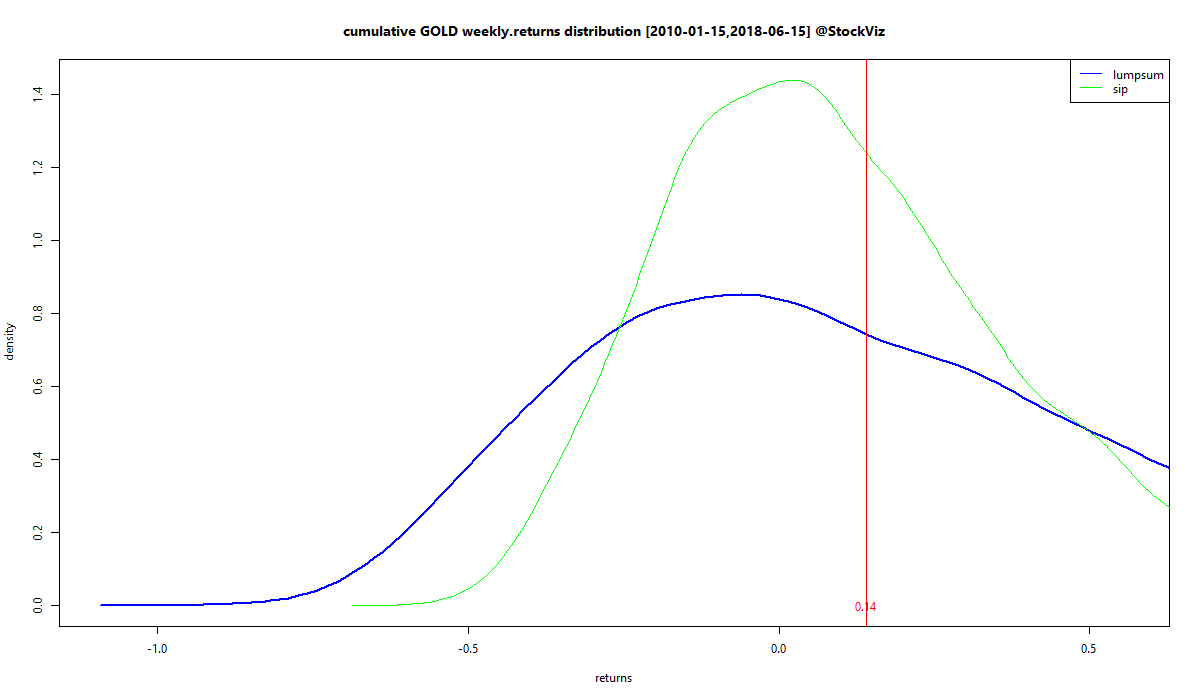

Here is the same MIDCAP:

/cumulative.simulation.avg.NIFTY%20MIDCAP%20100.2001-01-12.2018-09-28.png)

And for NIFTY 50:

/cumulative.simulation.avg.NIFTY%2050.1990-07-13.2018-09-28.png)

What does all this mean?

- It is possible for SIP returns to be negative over large periods of time. Enough to cover your entire investing lifetime. So, if you are investing in small-caps, make sure you are not 100% allocated to it.

- Lumpsum investing gives you a higher probability of higher returns across all indexes. The probability of negative returns are on par with that of SIP’s.

- Lumpsums have fatter left tails. However, if you are looking only at NIFTY 50 and MIDCAP, those probabilities are tiny.

- Lumpsums have a higher probability of achieving ‘average’ returns compared to SIPs.

- Lumpsums seem to be benefiting from “time in the market” on indexes that rise over a period of time.

Code and charts on github.