What is the difference between buying gold through an ETF over buying the front-month futures contract and constantly rolling it over?

When you buy physical gold, there is a cost of carry involved (funding rate + storage), plus an ETF will charge an asset management fee.

Futures also have a similar cost of carry plus a rollover cost. At expiry, the price at which you sell the expiring contract and buy the next month contract is not the same. The differential is the rollover cost.

Typically, the farther you go out on the futures termstructure, the higher the premium to spot – the commodity needs to be financed and stored for longer. This is called contango.

Currently, gold futures (GC) traded on COMEX has the following termstructure:

However, sometimes, the demand for near delivery is much higher than future delivery. This typically happens during a supply shock. When the near expiry futures trade at a premium to later expiries, the termstructure is said to be in backwardation.

Currently, oil futures (CL) traded on NYMEX has the following termstructure:

During contango, rolling over long futures incurs a positive rollover cost, negative otherwise.

For Gold Minis (GOLDM) traded on the MCX, the historical rollover cost at expiry has fluctuated within a wide band:

What this means for our analysis is that if we merely lined up the closing prices of the front-month contract and calculated returns, we will be off by ~2.5% (not considering brokerage, fees and CTT):

So, to answer the question we posed at the beginning of this post, GOLDBEES or GOLDM?

GOLDBEES, definitely.

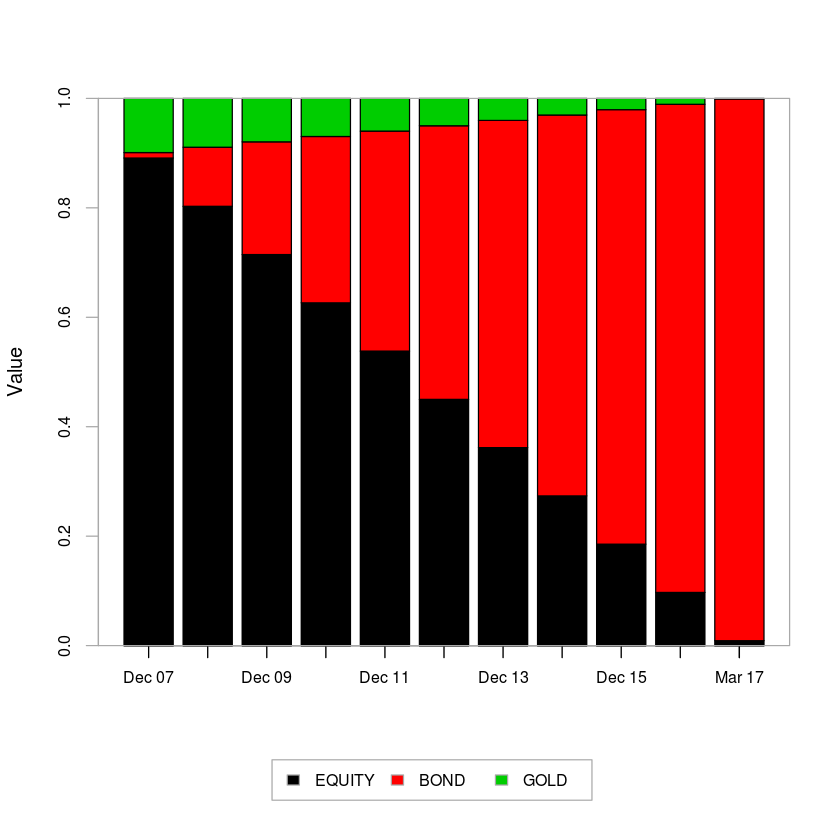

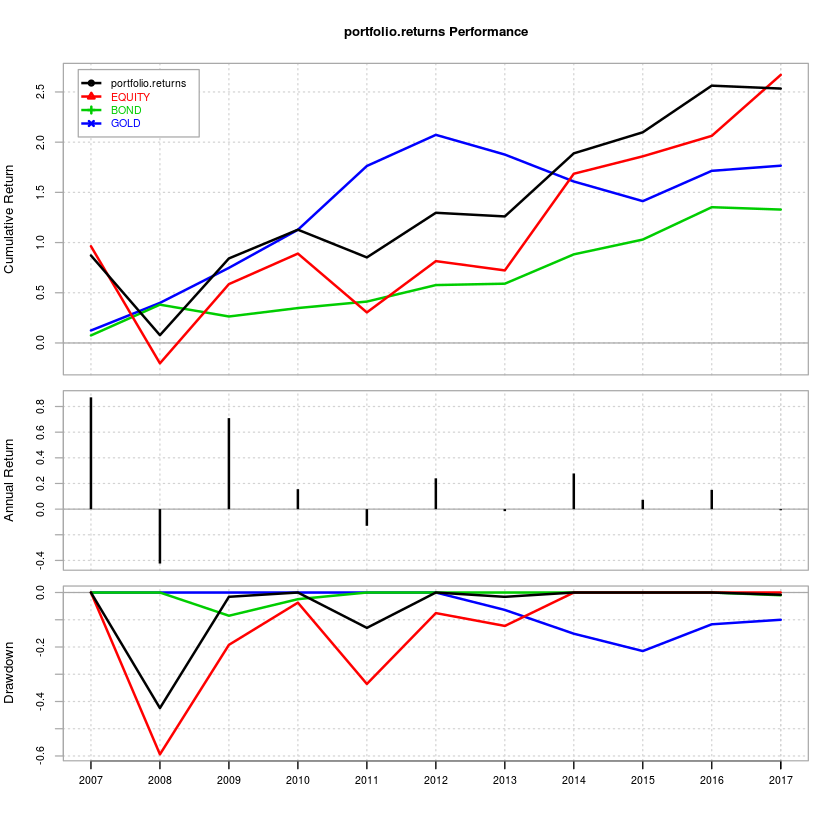

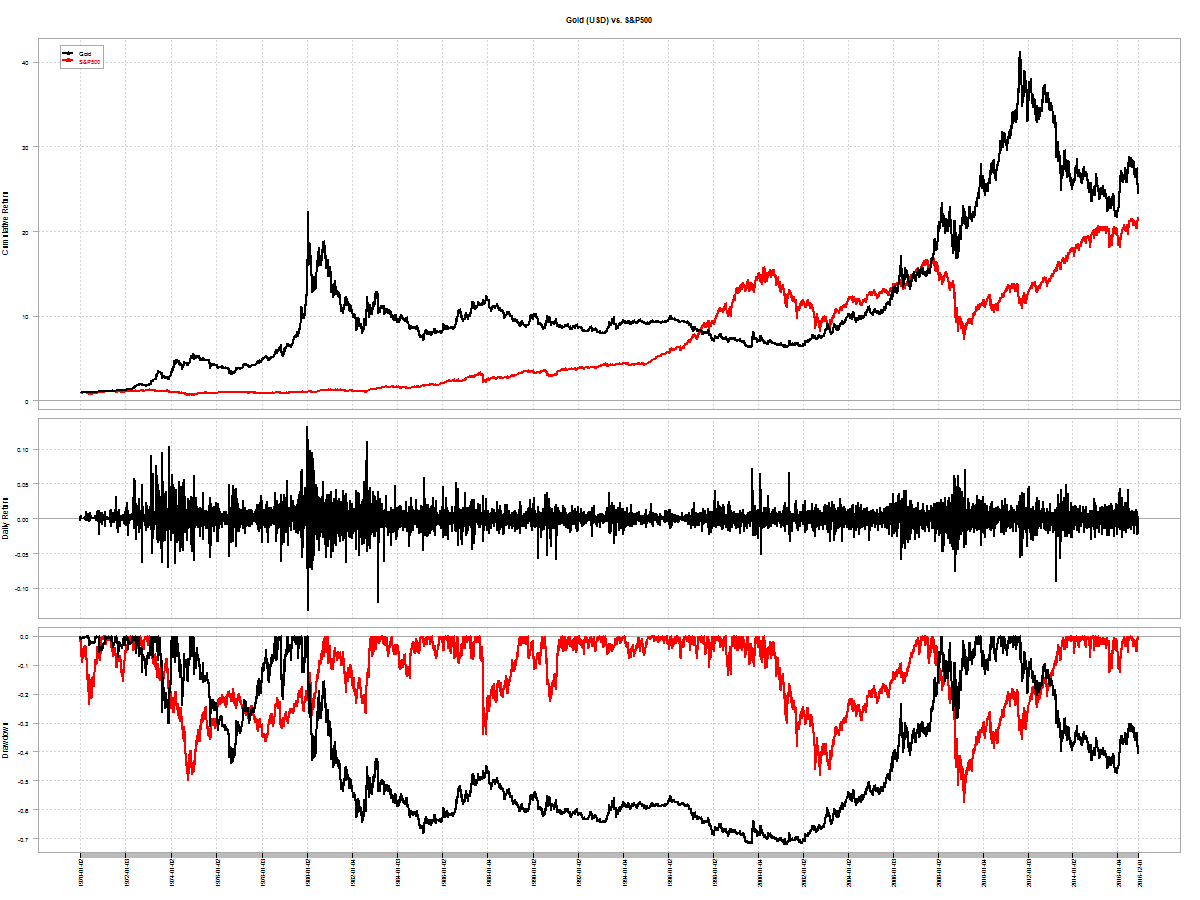

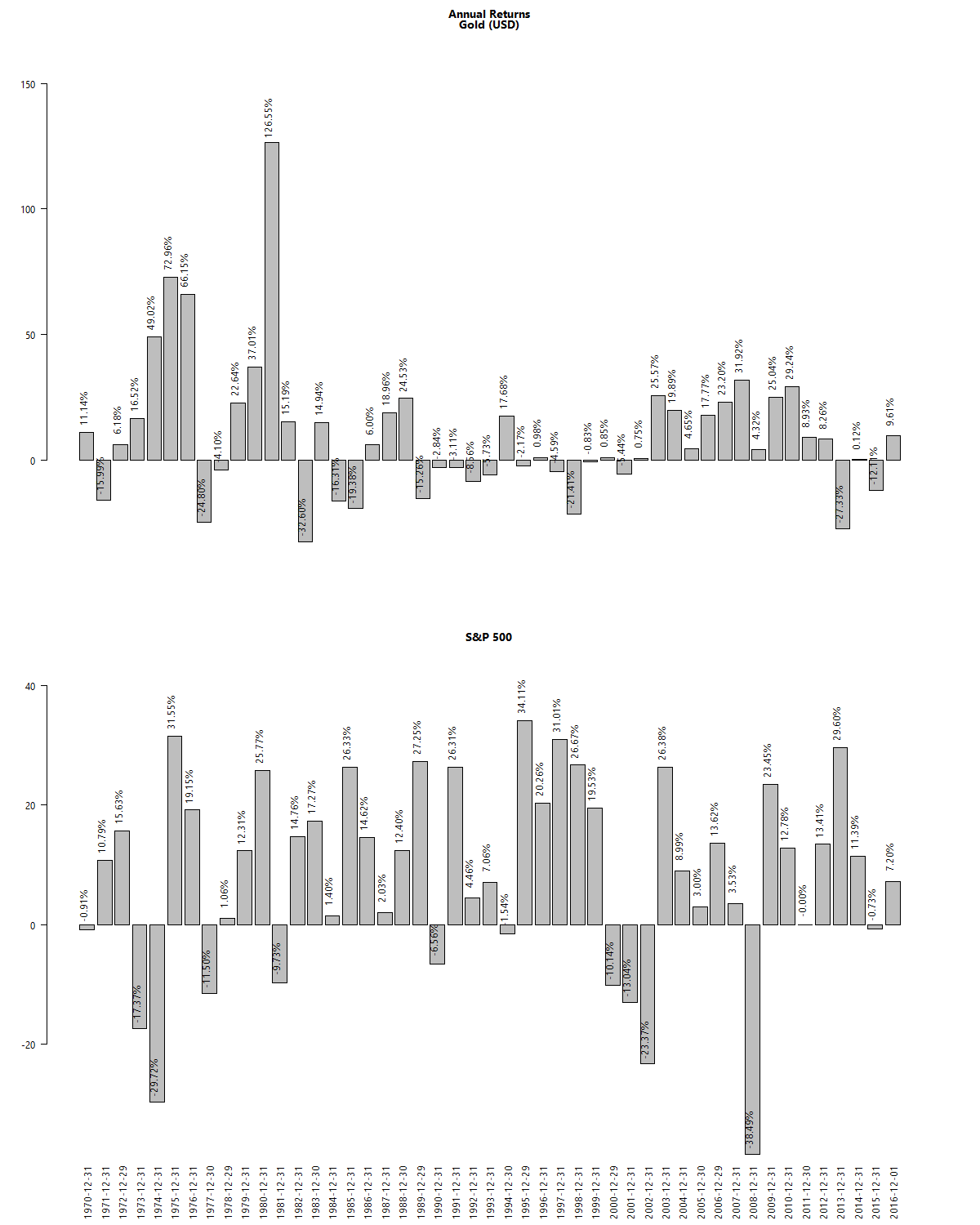

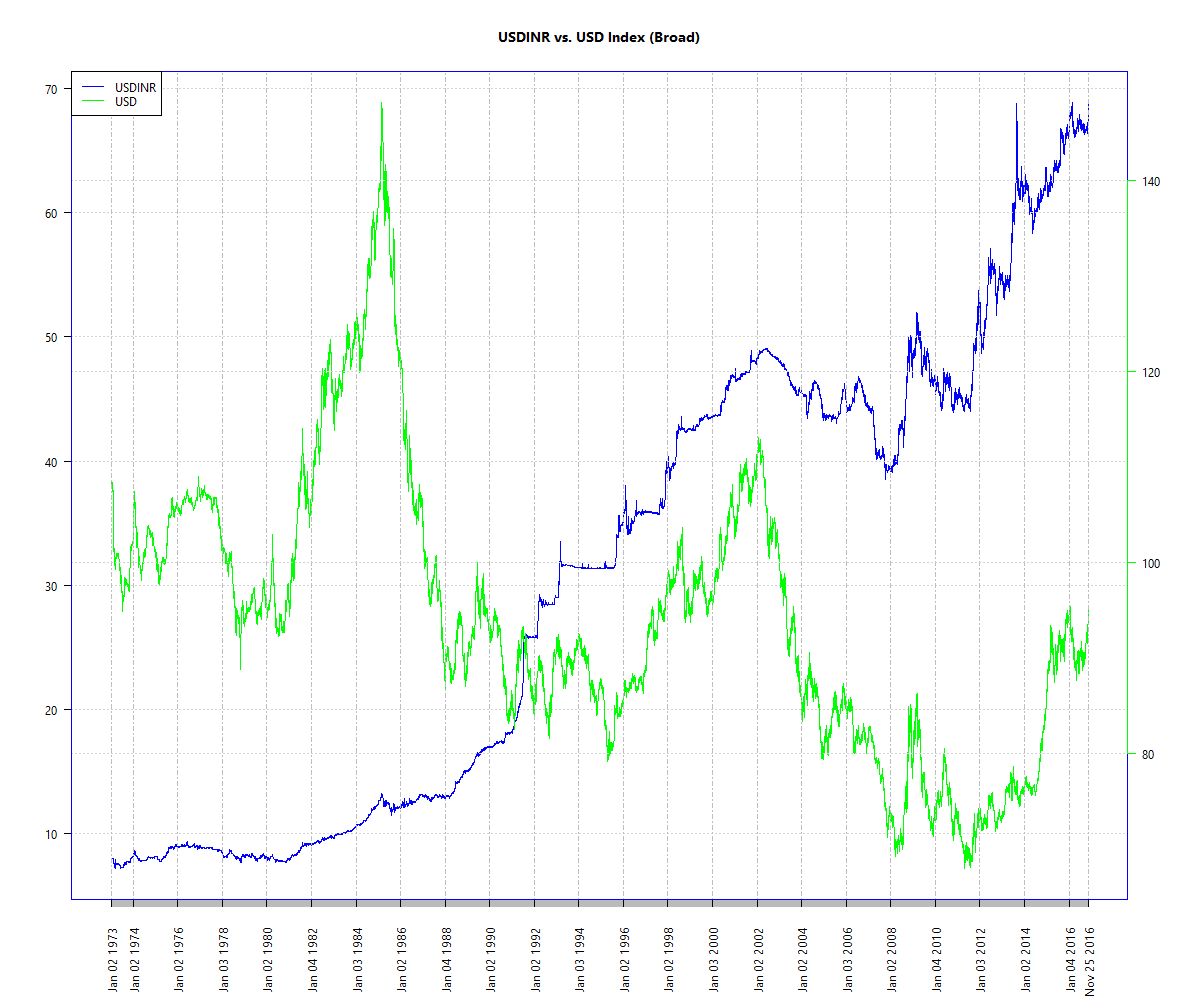

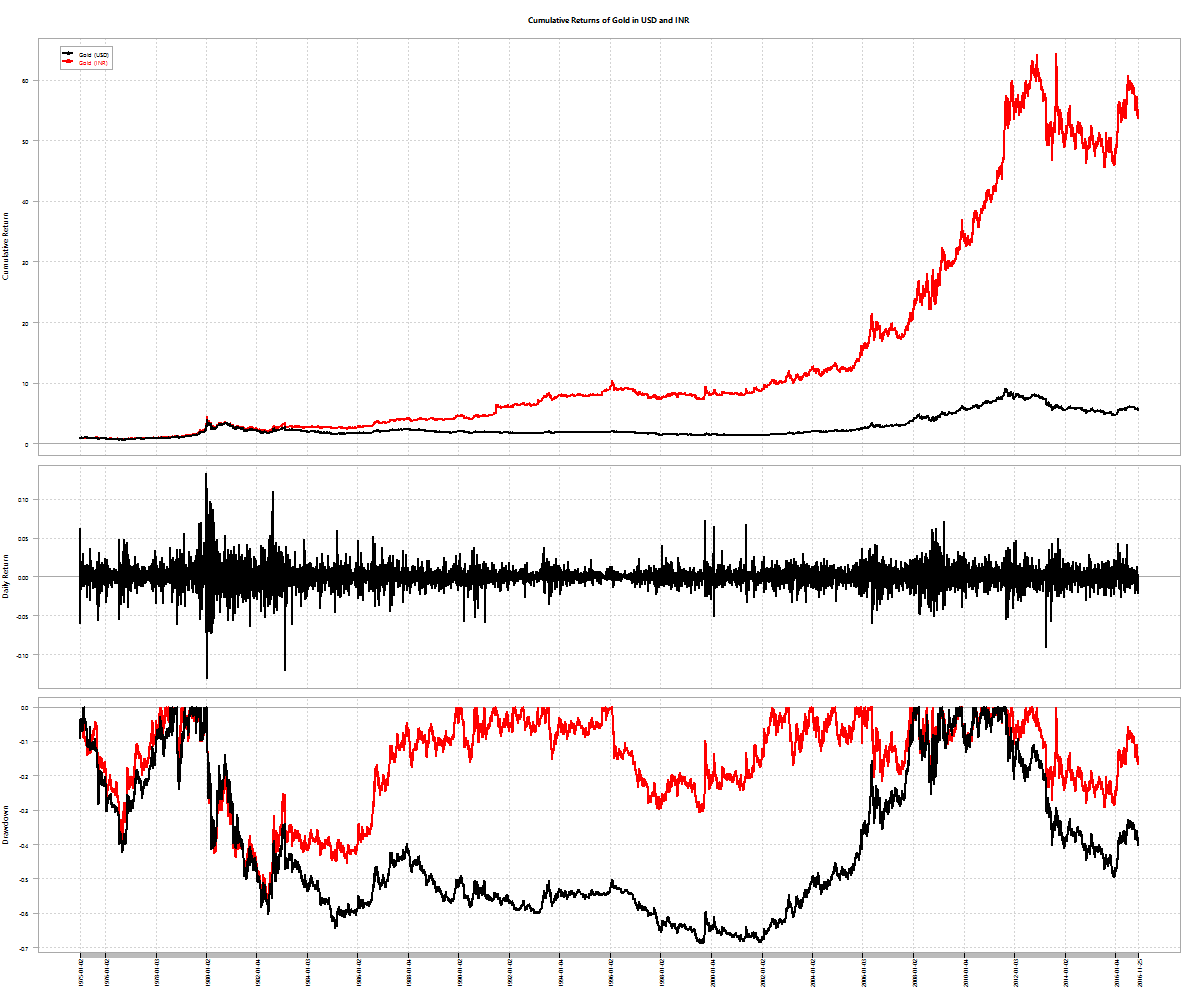

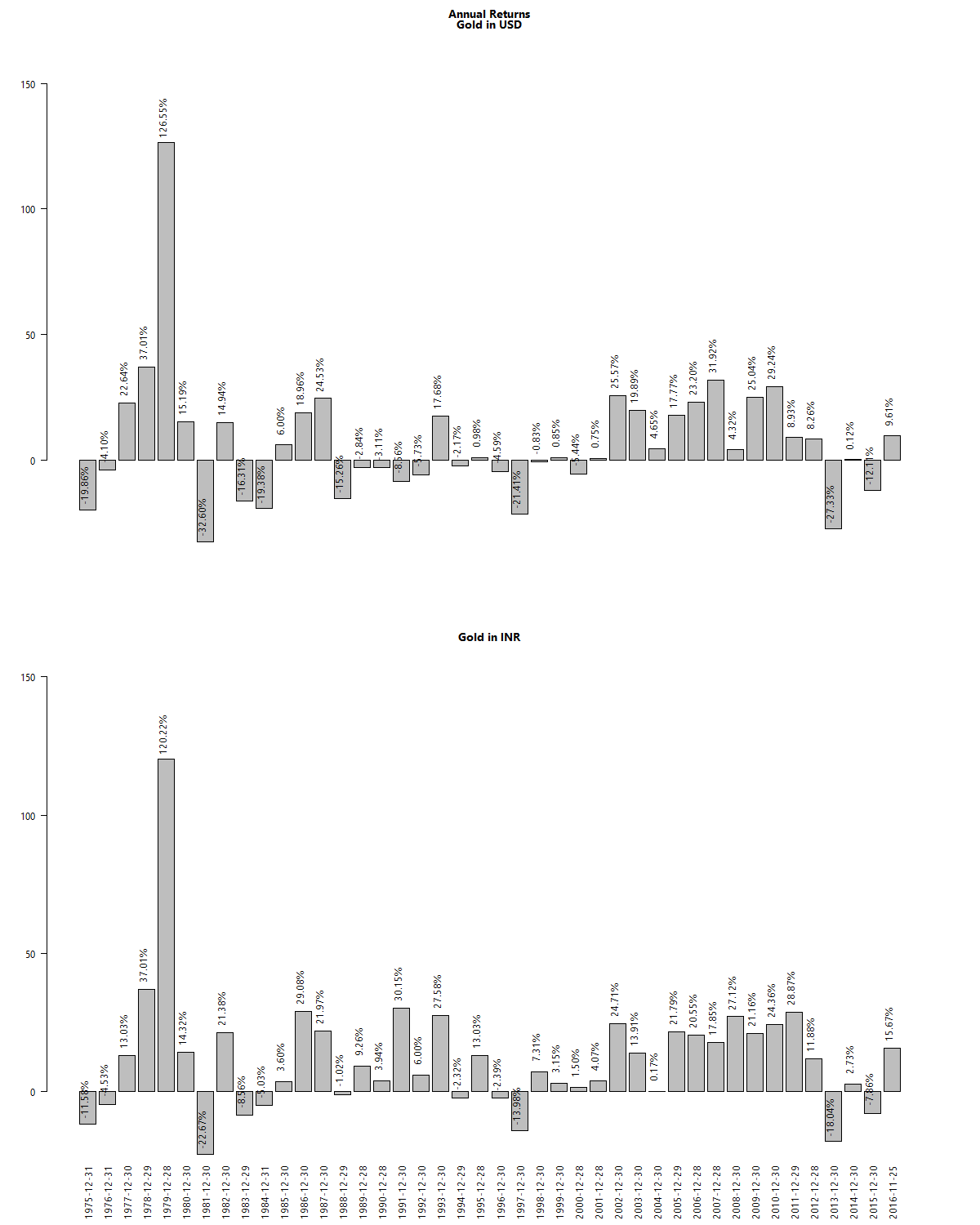

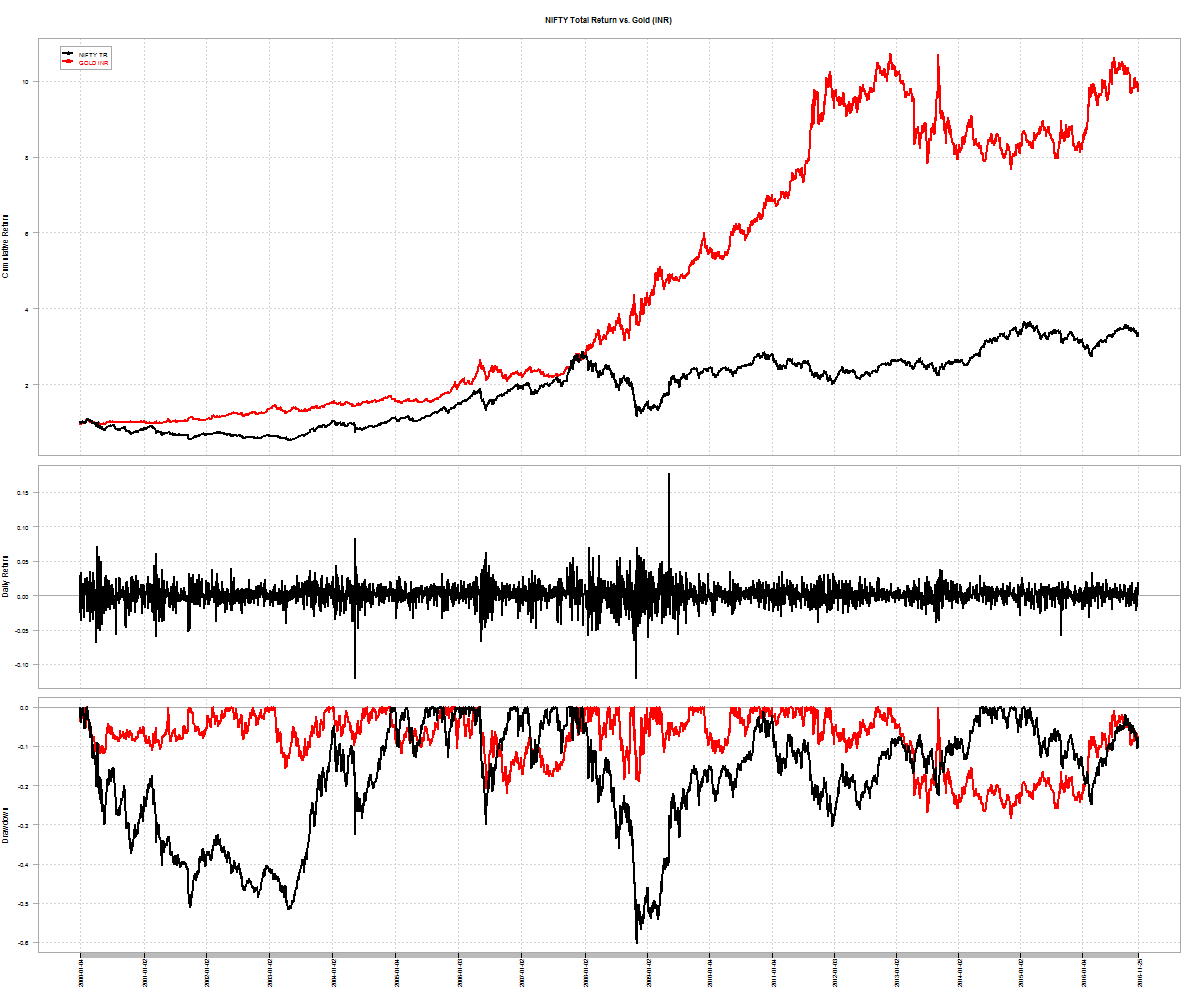

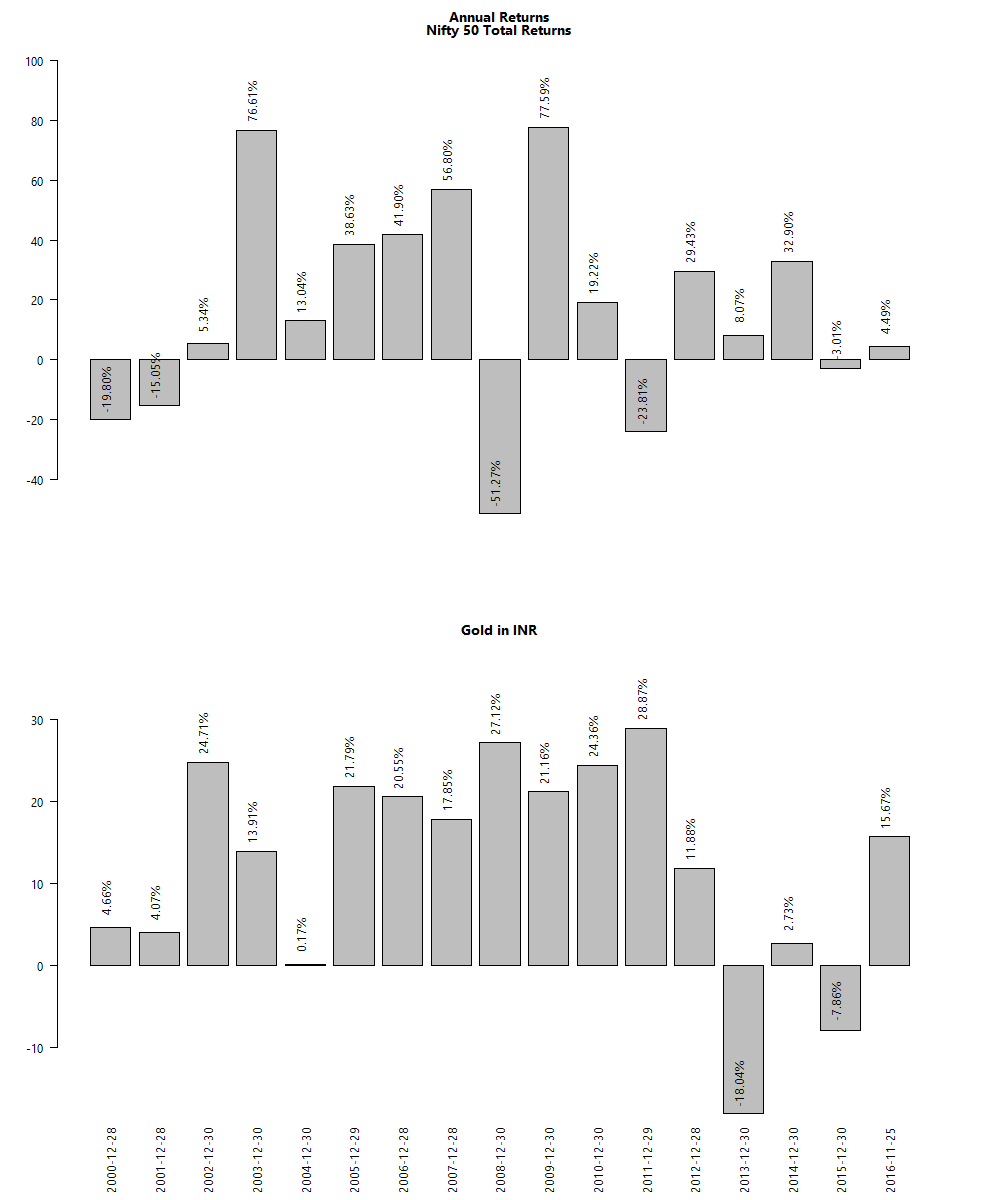

Previously: Investing in Gold

Charts and code on github.