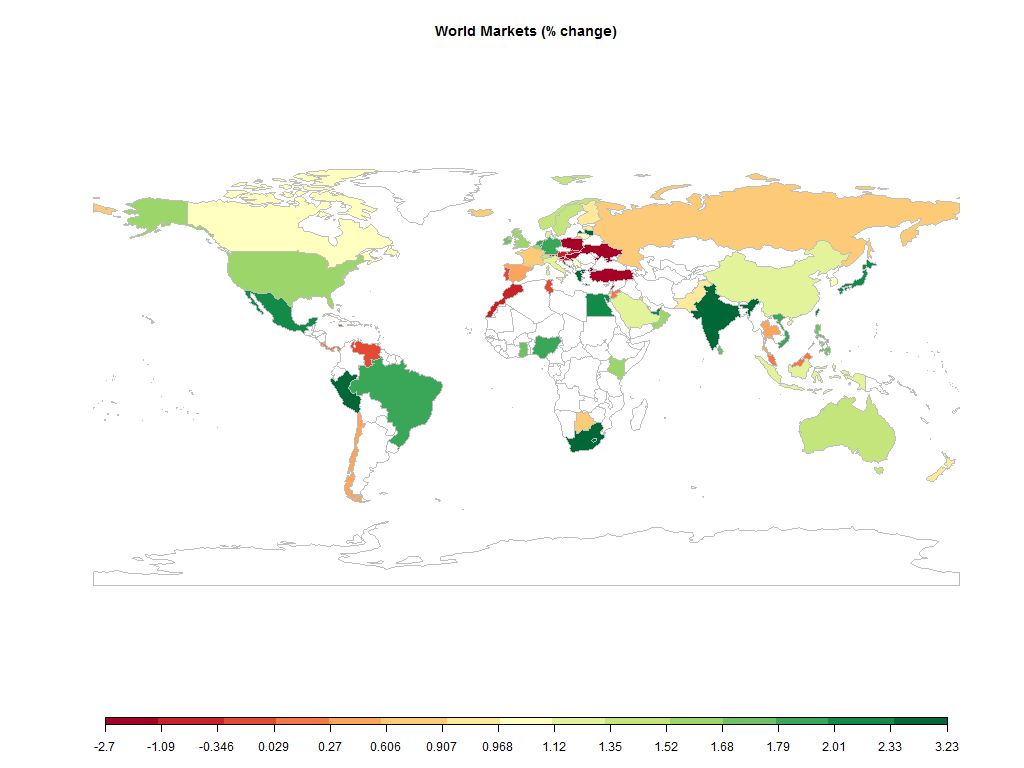

Equities

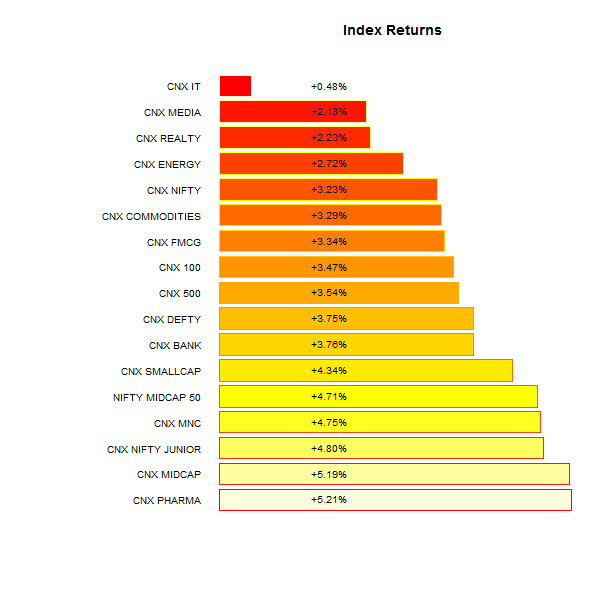

The Nifty turned out to be the best performing market this week, turning in +3.23% (+3.75% in USD.)

| MINTs | |

|---|---|

| JCI(IDN) | +1.25% |

| INMEX(MEX) | +2.05% |

| NGSEINDX(NGA) | +2.00% |

| XU030(TUR) | -1.44% |

| BRICS | |

|---|---|

| IBOV(BRA) | +1.80% |

| SHCOMP(CHN) | +1.12% |

| NIFTY(IND) | +3.23% |

| INDEXCF(RUS) | +0.84% |

| TOP40(ZAF) | +3.13% |

Commodities

| Energy | |

|---|---|

| Brent Crude Oil | -2.34% |

| Ethanol | +5.57% |

| Heating Oil | -2.73% |

| Natural Gas | -0.75% |

| RBOB Gasoline | -2.71% |

| WTI Crude Oil | -1.78% |

| Metals | |

|---|---|

| Copper | +3.49% |

| Gold 100oz | +0.17% |

| Palladium | +2.65% |

| Platinum | +1.53% |

| Silver 5000oz | +0.47% |

Currencies

| MINTs | |

|---|---|

| USDIDR(IDN) | -1.02% |

| USDMXN(MEX) | -0.12% |

| USDNGN(NGA) | -0.31% |

| USDTRY(TUR) | +0.40% |

| BRICS | |

|---|---|

| USDBRL(BRA) | +0.55% |

| USDCNY(CHN) | -0.21% |

| USDINR(IND) | -0.58% |

| USDRUB(RUS) | +2.21% |

| USDZAR(ZAF) | +1.42% |

| Agricultural | |

|---|---|

| Cattle | +1.90% |

| Cocoa | -1.81% |

| Coffee (Arabica) | +1.24% |

| Coffee (Robusta) | +2.27% |

| Corn | -5.39% |

| Cotton | -4.97% |

| Feeder Cattle | +1.72% |

| Lean Hogs | +0.50% |

| Lumber | -0.30% |

| Orange Juice | +1.36% |

| Soybean Meal | -4.91% |

| Soybeans | -3.50% |

| Sugar #11 | +4.82% |

| Wheat | -2.78% |

| White Sugar | -2.94% |

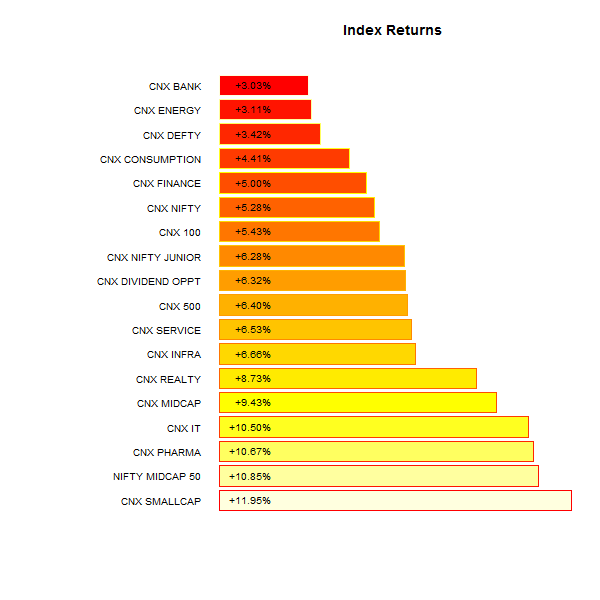

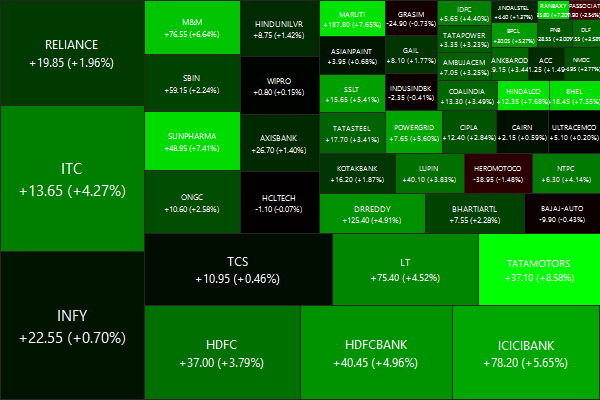

Nifty Heatmap

Index Returns

Top winners and losers

| EXIDEIND | +11.25% |

| ADANIENT | +13.99% |

| ADANIPORTS | +19.08% |

| JPASSOCIAT | -2.54% |

| TATAGLOBAL | -1.90% |

| FEDERALBNK | -1.60% |

The Adani’s are crushing it right now. Go Modi!

ETFs

| JUNIORBEES | +5.68% |

| NIFTYBEES | +3.52% |

| INFRABEES | +2.45% |

| PSUBNKBEES | +2.31% |

| BANKBEES | +0.14% |

| GOLDBEES | -0.79% |

Yellow metal turned red…

Investment Theme Performance

| Financial Strength Value | +7.34% |

| Magic Formula Investing | +5.03% |

| Growth with Moat | +4.68% |

| Consistent10* | +4.31% |

| Market Elephants | +4.27% |

| Balance-sheet Strength | +4.17% |

| Long Term Equity* | +3.85% |

| ADAG Mania | +3.77% |

| Enterprise Yield | +3.68% |

| Quality to Price | +3.58% |

| Industrial Value | +3.58% |

| Momentum 200 | +3.41% |

| Efficient Growth | +2.97% |

| Market Fliers | +2.75% |

| IT 3rd Benchers | -0.30% |

IT went out of favor again. Otherwise, pretty much all other investment strategies performed well.

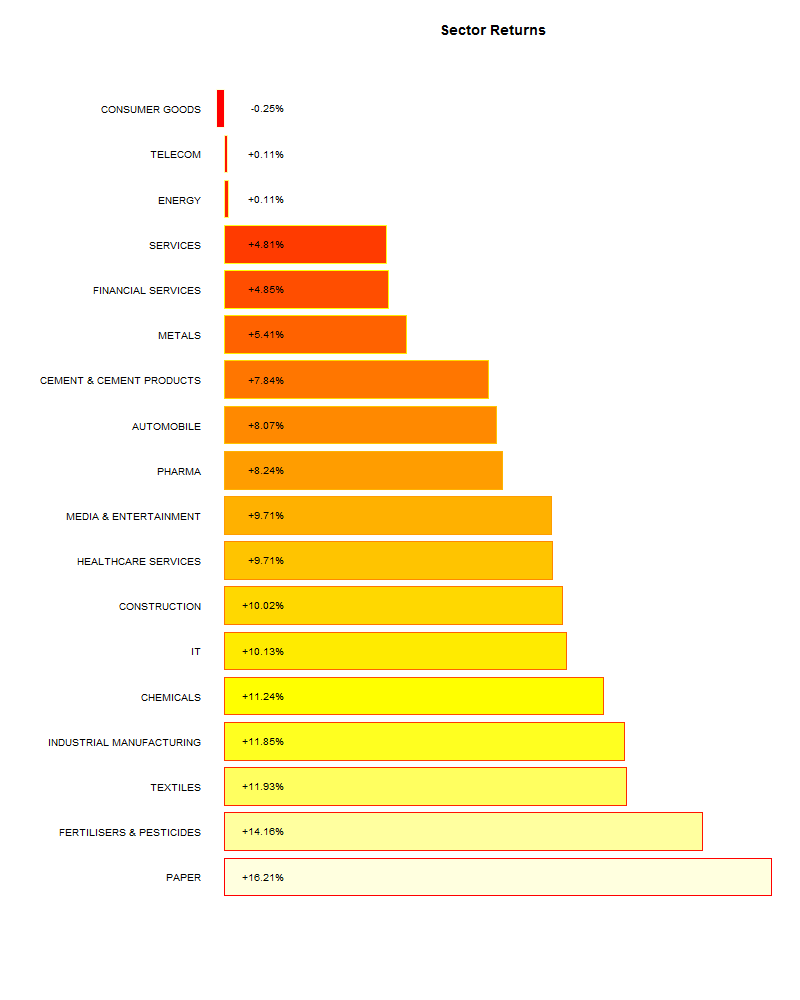

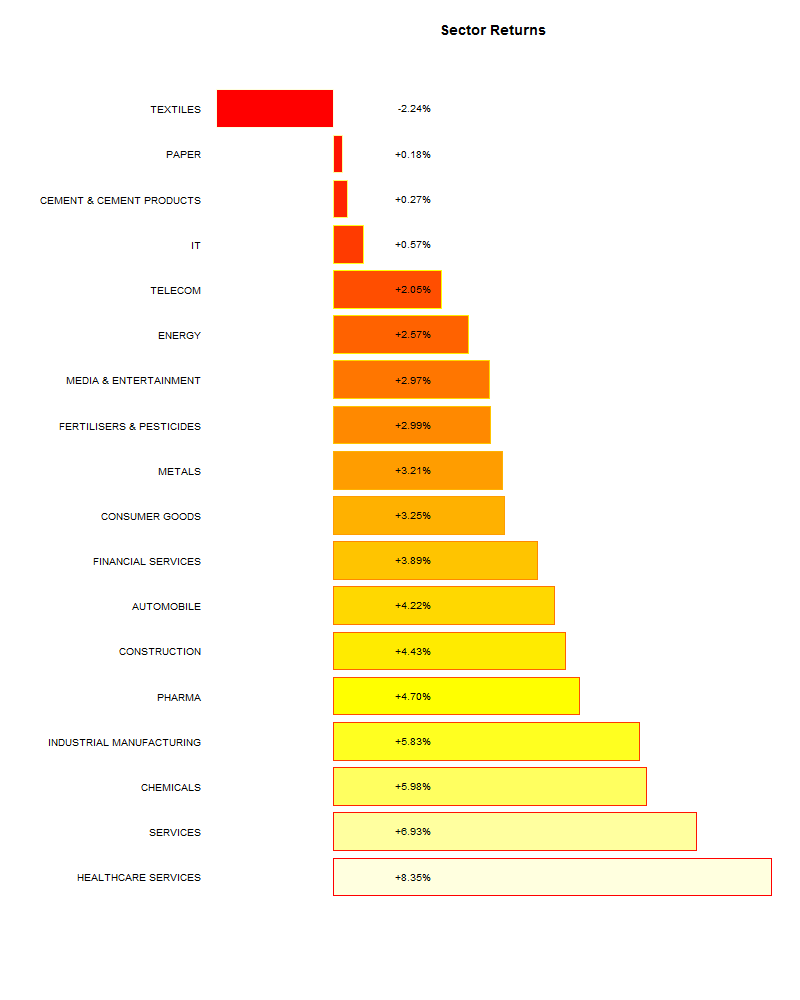

Sector Performance

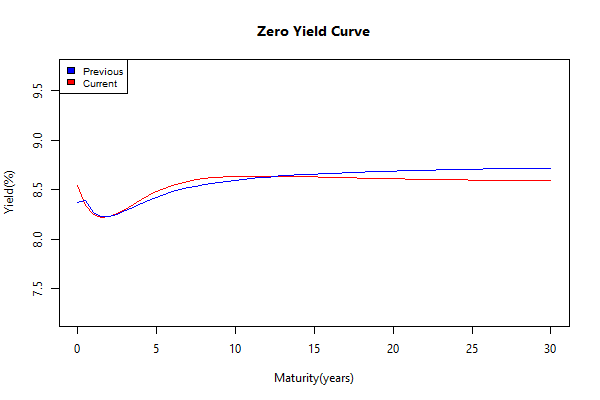

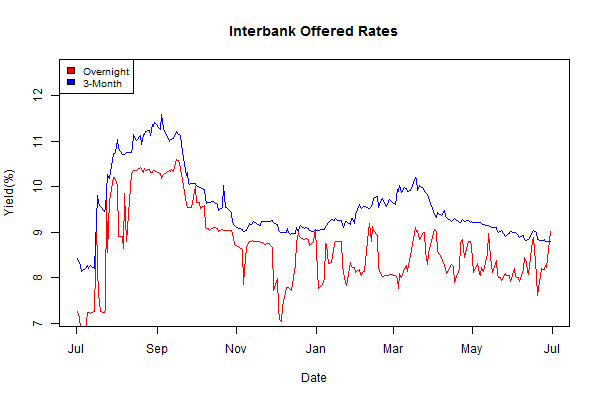

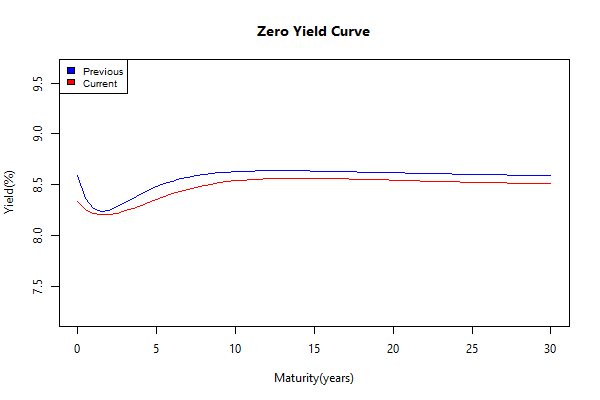

Yield curve

Yields continued to compress…

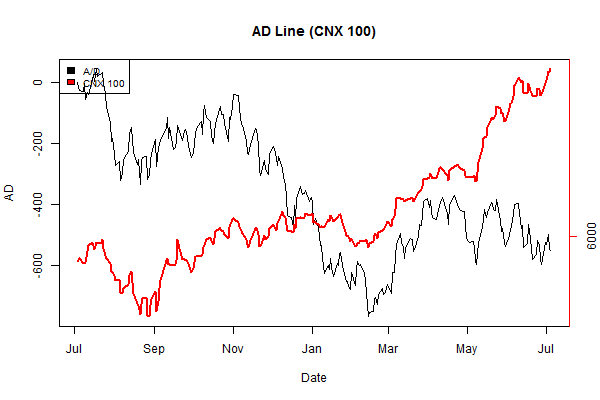

Advance Decline

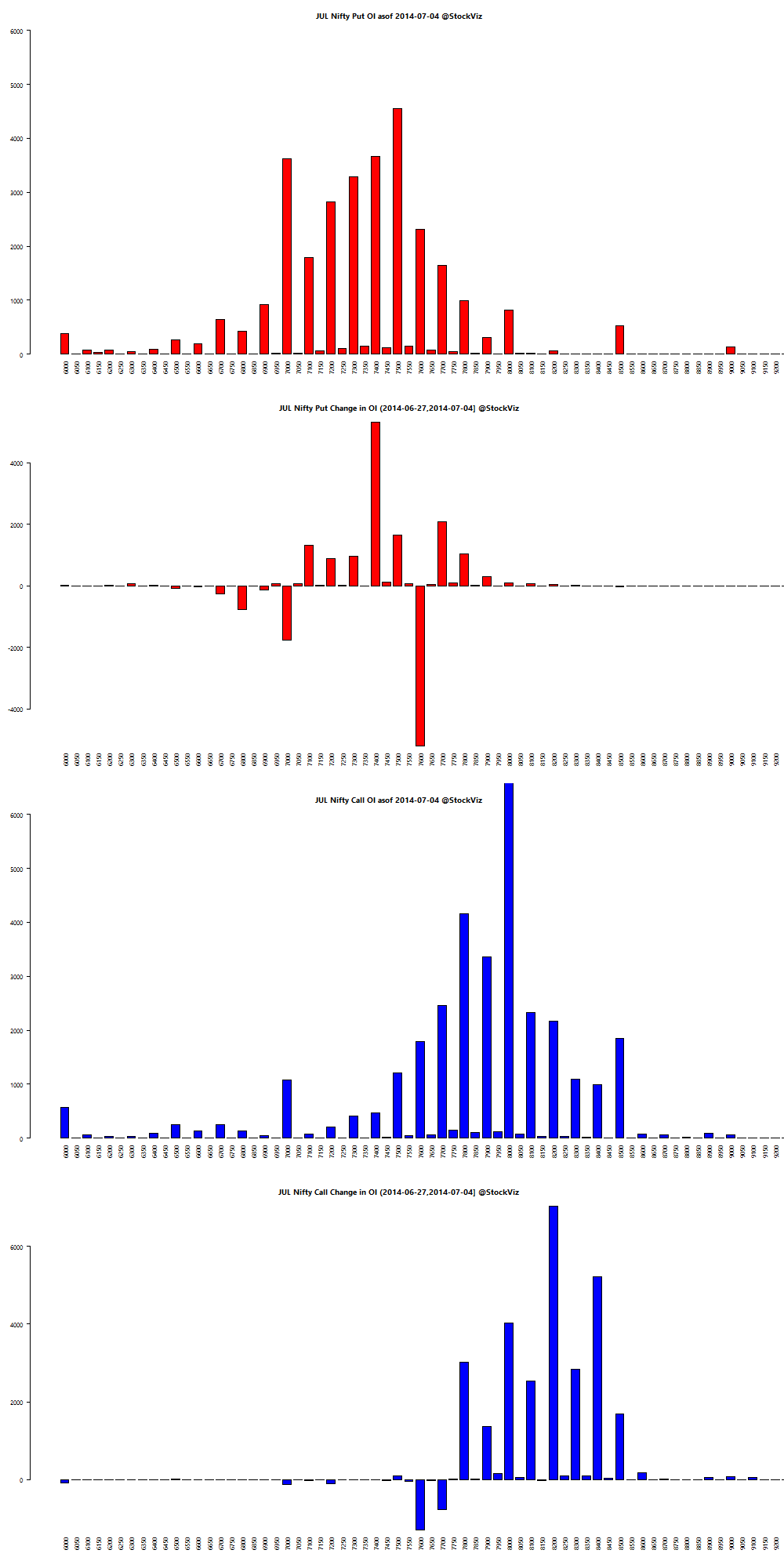

Nifty OI

A lot has been said about 8000 calls, but look at the action in 8200 and 8400 calls!

Thought for the weekend

Take a picture of this. Take a picture of that. Point the phone at this. Let the phone listen to that. The technology exists to capture anything and turn it into more. More information. A transaction. A conversation.

Say it. Take a photo of it. Type it. Scan it. Whatever. Now, it’s not just websites that give hyperlinks. Everything in the physical world is now a hyperlink too.

Say it. Take a photo of it. Type it. Scan it. Whatever. Now, it’s not just websites that give hyperlinks. Everything in the physical world is now a hyperlink too.

Source: The World Is A Hyperlink