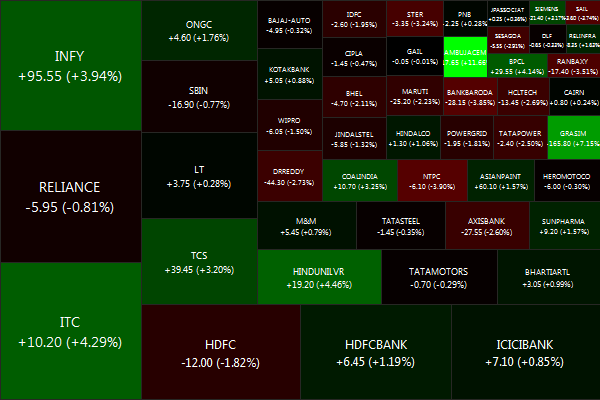

The NIFTY ended flat for the week.

Biggest losers were HINDALCO (-5.25%), TCS (-3.06%) and SAIL (-2.76%).

And the biggest winners were ONGC (+5.08%), HEROMOTOCO (+4.30%) and POWERGRID (+3.77%).

Advancers lead decliners 29 vs 20

Gold: -0.34%, Banks: +0.03%.

The week began with expectations that the RBI will cut rates – but all that the central bank did was to point a finger at the government and say “your turn.” Thursday saw the US Fed extending Operation Twist (selling short term treasuries while buying long-terms) but failing to deliver on hopes of QE3. You could say Bernanke did an RBI in that he too pointed a finger at the US government sad said “your turn.”

From an India perspective the benefits from a collapse in oil prices were negated by an almost proportional fall in the Rupee. The only thing that oil prices this low seem to be doing is laying waste to all the “alternative” energy company’s business models that require at least $100 oil.

With Europe throwing fits in the sandbox, anything can happen. Stay hedged!

Daily news summaries are here.