Open sourced by Meta back in 2017, Prophet is a procedure for forecasting time series data. Here, we give it two years of monthly returns and use it to forecast returns one month forward. The forecasts are ranked and a portfolio is constructed for the forward month.

The results are not as bad as fitting a simple linear model but not that great either.

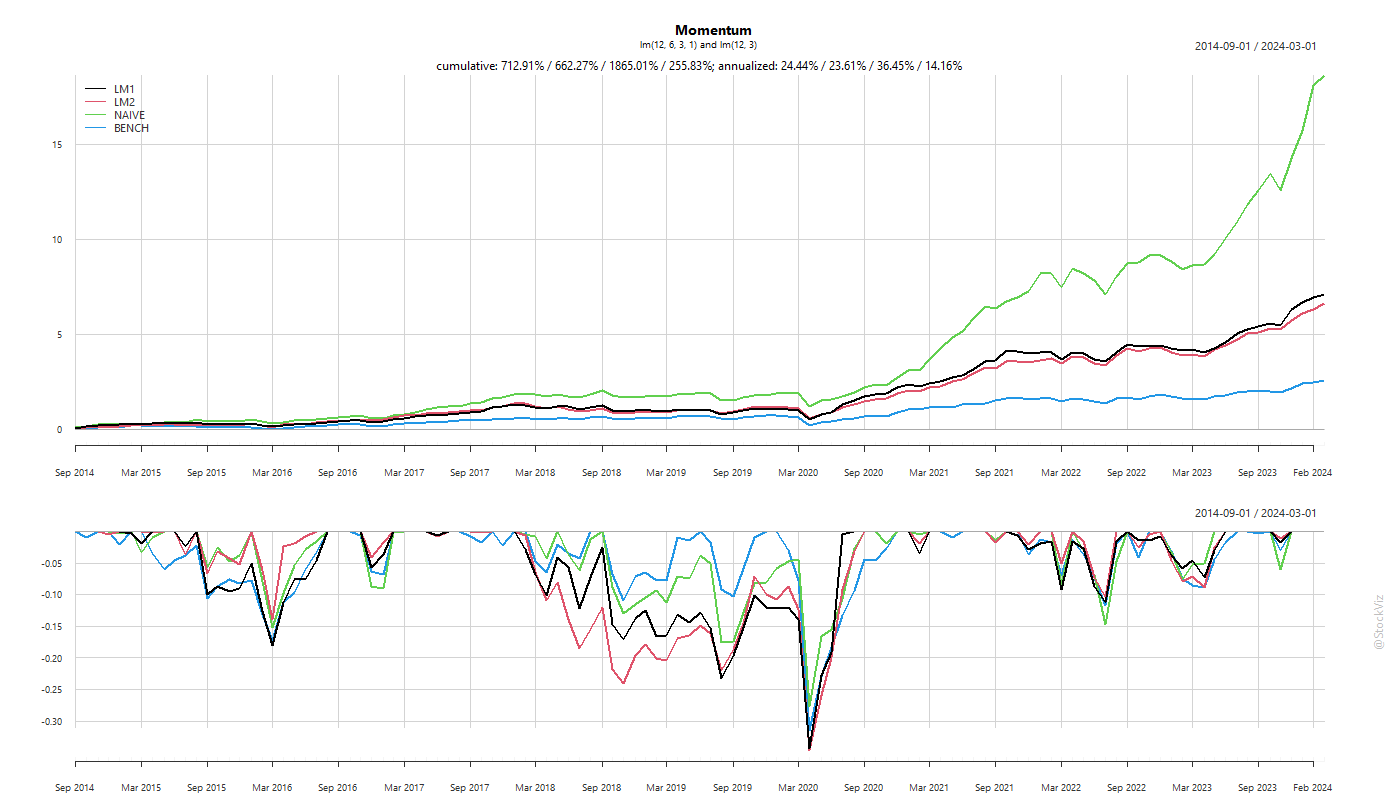

More often than not, simple models outperform complicated ones. Inspired by some recent academic research that showed that linear regressions yielded better momentum performance, we did a quick backtest to check if building a linear model through recent 12 and 1/3/6-month performance and creating a portfolio using its next-month predictions made sense.

Counter-intuitively, a naïve momentum strategy outperformed linear models.

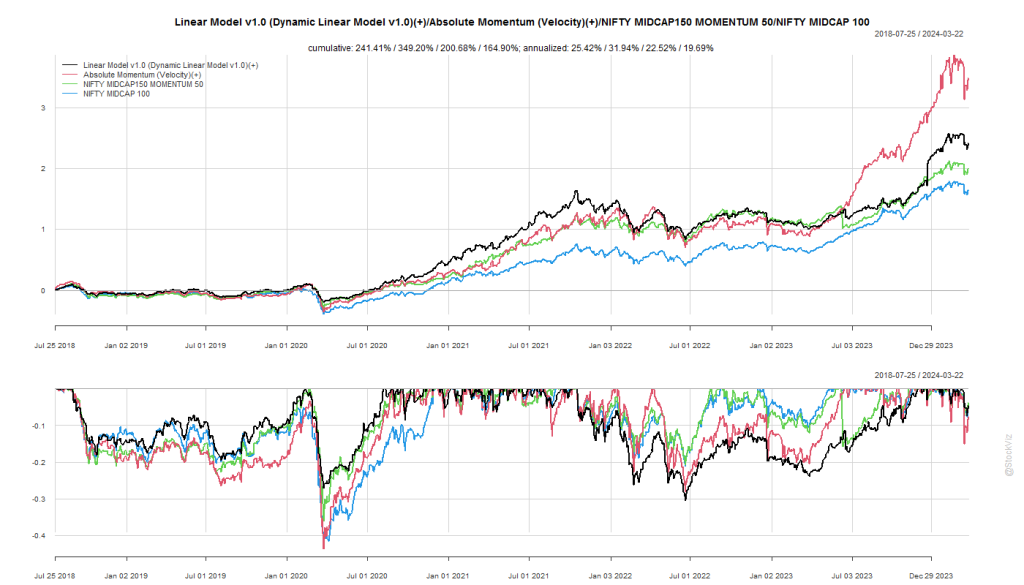

This is not our first run-in with linear regressions. Our Dynamic Linear Model strategy simply regresses prices to a 45* line and ranks them based on goodness of fit.

Most of the time, of all the different ways to skin the cat, the simplest is the best one.

Typically, trend-following systems span multiple asset classes in order to reduce correlations. There could be a case for applying a trend-following system over equities and commodities in India. However, not all commodities trade and activity profiles can be vastly different.

It appears that most of the trading activity at the MCX occurs between 6pm and 9pm.

Not all listed commodities trade…

… and most of the activity centers around silver and natural gas – two of the most volatile commodities.

It maybe worthwhile to add at least some of these tickers into the mix and measure their effect on trend-following portfolios.

Our previous post discussed how liquidity drops exponentially as the market cap gets smaller. This illiquidity also means that a lot of micro-cap stocks spend their time out of the market.

This is a problem for direct equity investors in micro-caps if they actually try to bank the price appreciation they might have seen in the stocks that they own. And a bigger problem for momentum algorithms in the small-cap space.

Index funds in the micro-cap space have yet to go through a test of the liquidity mismatch between allowing redemptions at daily NAV vs. not being able to trade the underlying stocks for days on end.

Bull markets allow us the luxury of coming up with a plan for something that has plenty of historical precedent.

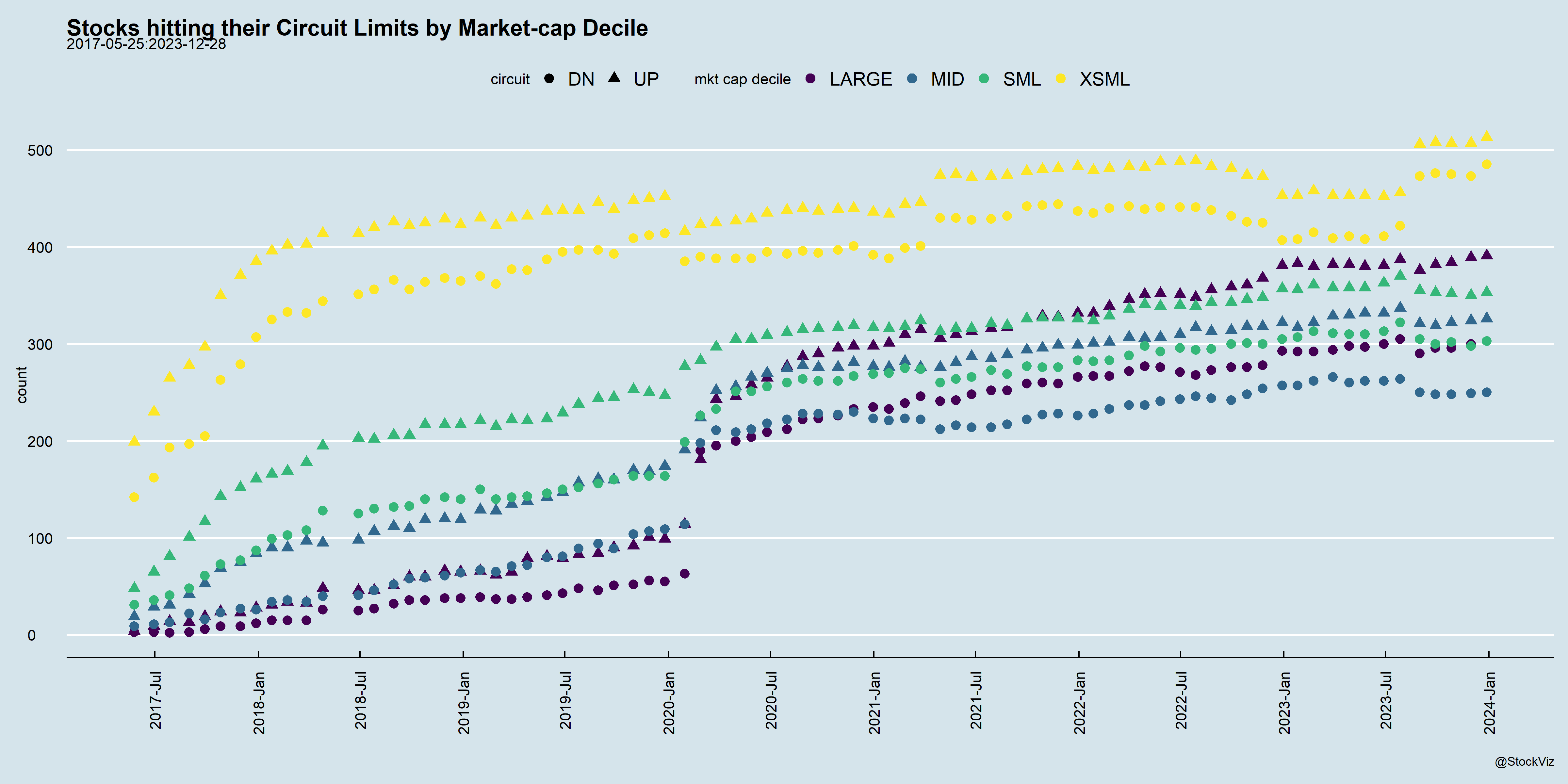

Our previous post used AMFI’s classification of stocks by market-cap to analyze liquidity dynamics. What if we broke down the universe of stocks into their market-cap deciles and then applied the same illiquidity metric to them?

If you look at the full sample, median liquidity tracks market-cap.

Mid/small caps have an embedded illiquidity premium. While index/mutual funds are obligated to honor their NAVs on redemption, there is no guarantee that direct equity investors can exit without taking a direct hit. Liquidity flees during market stress.

During bull markets, the taps are open. December 2017 was the absolute zenith of the mid/small cap mania. Liquidity was ample.

A month later, the hangover began. Erstwhile small-cap momentum stocks would hit their lower-circuits within a few seconds of the open. The market-clearing price for some of them were a cool 40%-50% away from where they finished 2017. It was weeks of watching the portfolio slowly bleed away.

All this to say, understanding liquidity dynamics is as important as understanding the fundamental and technical aspects of the stocks you own.