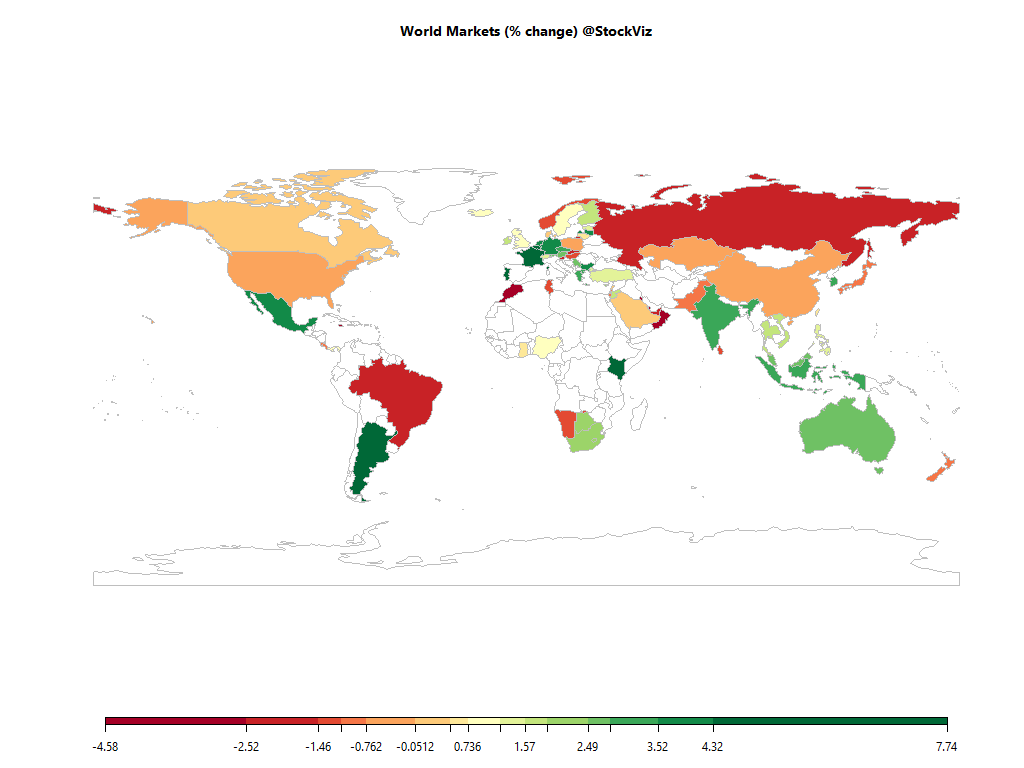

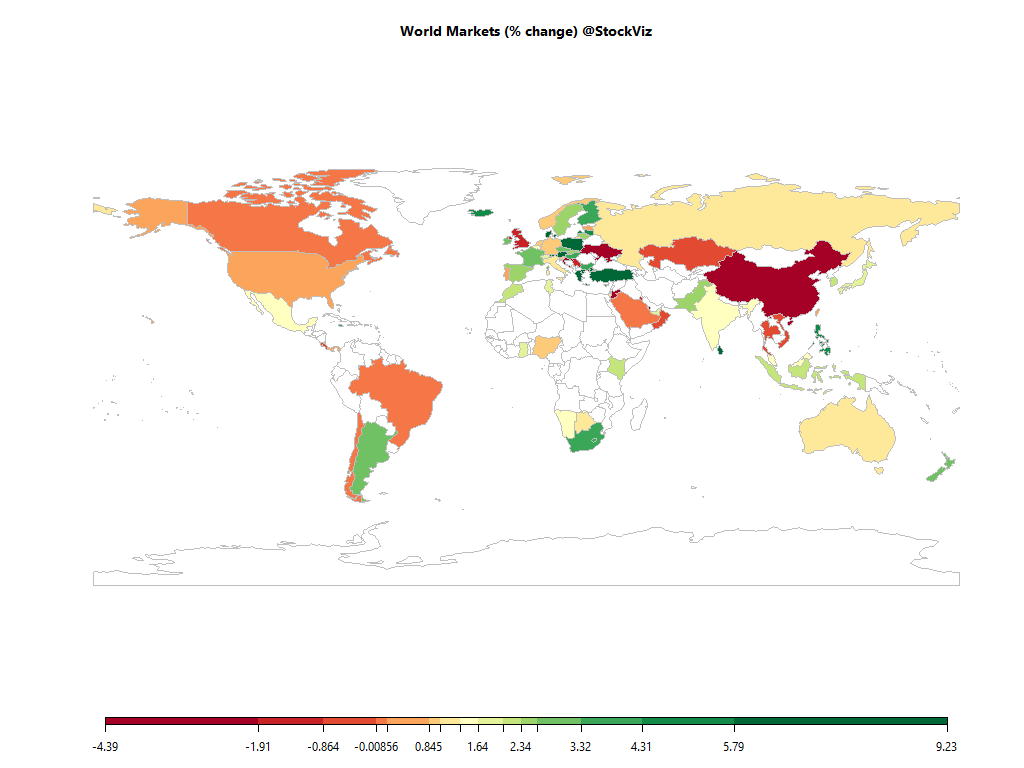

Equities

| MINTs | |

|---|---|

| JCI(IDN) | +2.10% |

| INMEX(MEX) | +1.49% |

| NGSEINDX(NGA) | +0.98% |

| XU030(TUR) | +7.02% |

| BRICS | |

|---|---|

| IBOV(BRA) | -0.01% |

| SHCOMP(CHN) | -2.11% |

| NIFTY(IND) | +1.42% |

| INDEXCF(RUS) | +1.04% |

| TOP40(ZAF) | +4.22% |

Commodities

| Energy | |

|---|---|

| Brent Crude Oil | -1.74% |

| Ethanol | -2.63% |

| WTI Crude Oil | -2.99% |

| RBOB Gasoline | -9.46% |

| Heating Oil | -4.41% |

| Natural Gas | +2.79% |

| Metals | |

|---|---|

| Platinum | -0.92% |

| Copper | -2.26% |

| Silver 5000oz | -5.52% |

| Palladium | +3.04% |

| Gold 100oz | +1.11% |

Currencies

| MINTs | |

|---|---|

| USDIDR(IDN) | +0.05% |

| USDMXN(MEX) | +0.55% |

| USDNGN(NGA) | -1.51% |

| USDTRY(TUR) | -2.06% |

| BRICS | |

|---|---|

| USDBRL(BRA) | +1.36% |

| USDCNY(CHN) | +0.09% |

| USDINR(IND) | -0.93% |

| USDRUB(RUS) | +1.21% |

| USDZAR(ZAF) | -0.66% |

| Agricultural | |

|---|---|

| Coffee (Robusta) | -10.25% |

| Feeder Cattle | +11.81% |

| Lumber | -0.68% |

| Sugar #11 | -4.27% |

| Coffee (Arabica) | -5.52% |

| Soybean Meal | +1.17% |

| White Sugar | -4.05% |

| Cattle | +3.42% |

| Cotton | +3.72% |

| Lean Hogs | +2.18% |

| Wheat | +0.18% |

| Cocoa | -16.04% |

| Corn | -0.75% |

| Orange Juice | +2.10% |

| Soybeans | +0.58% |

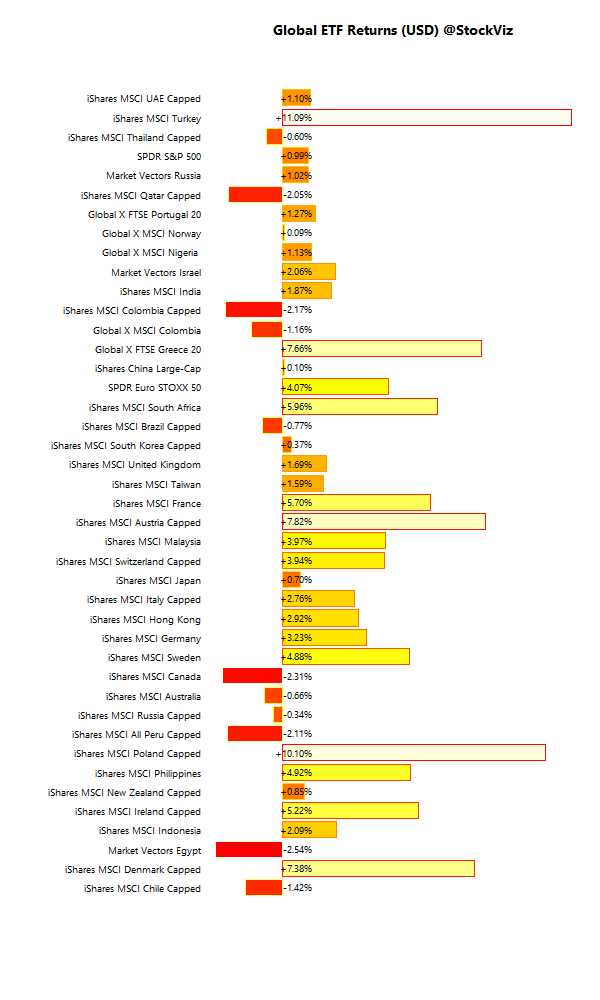

International ETFs (USD)

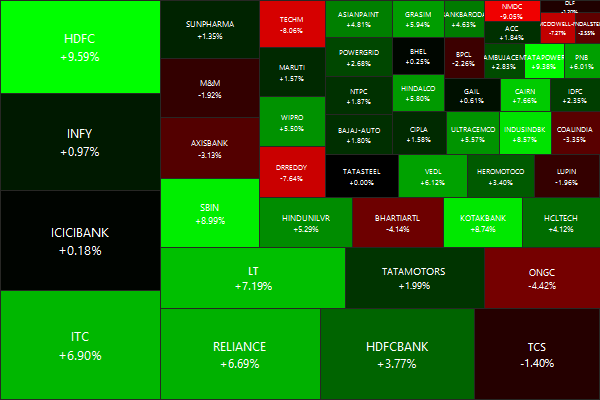

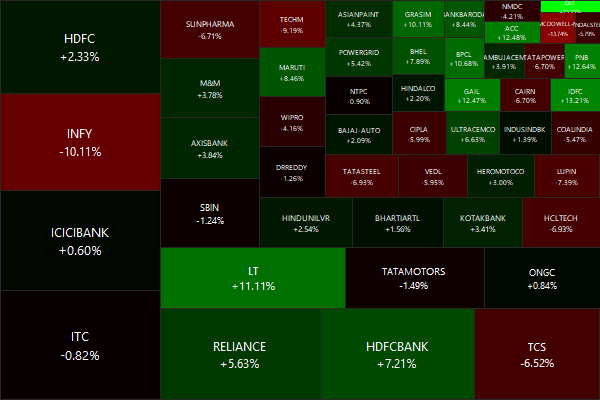

Nifty Heatmap

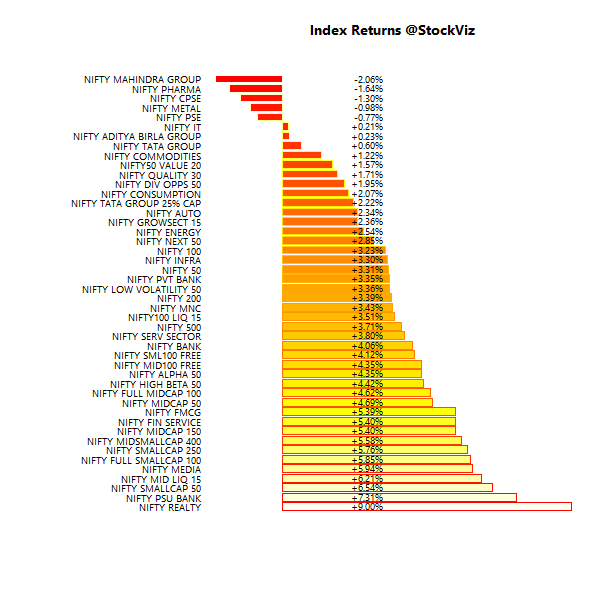

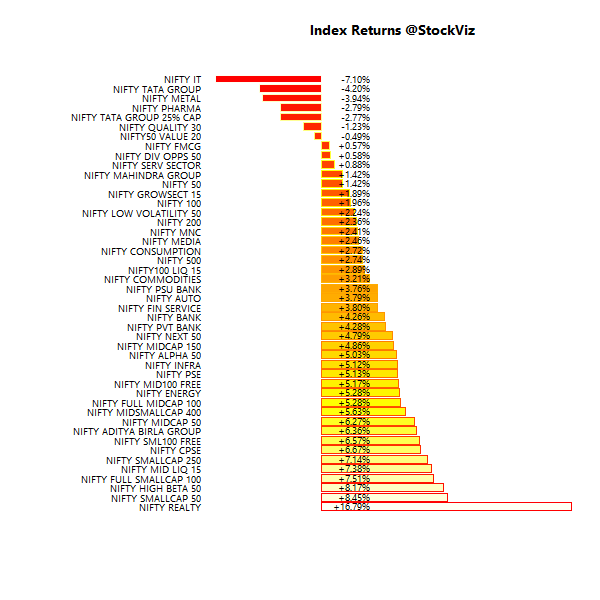

Index Returns

More: Sector Dashboard

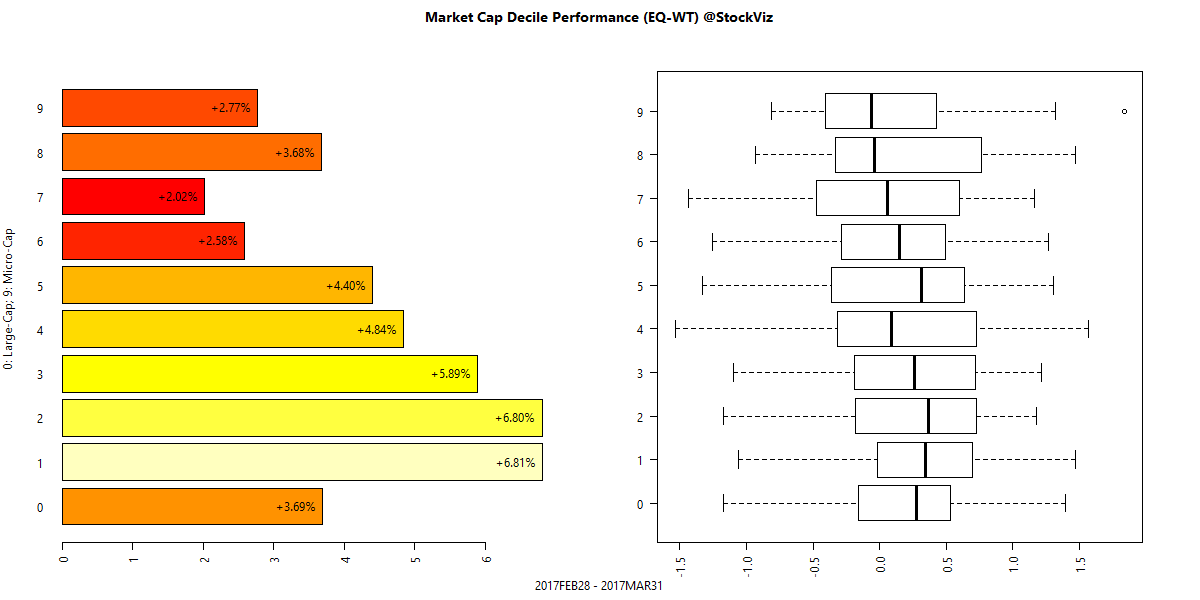

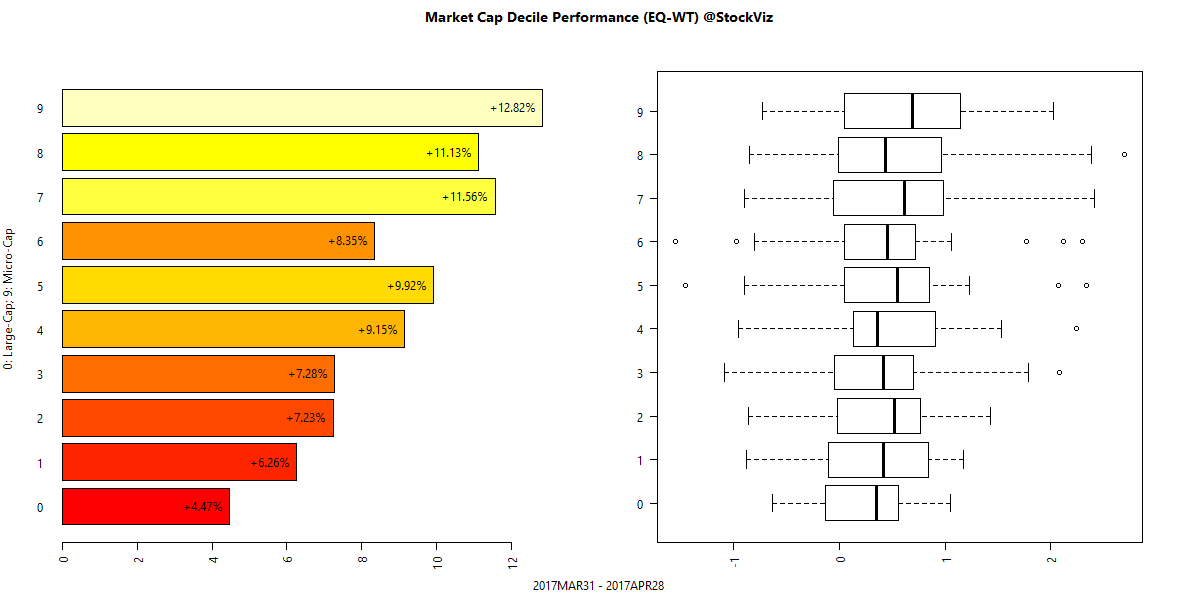

Market Cap Decile Performance

More: Equal-Weight Deciles, Cap-Weight Deciles

ETF Performance

| CPSEETF | +6.70% |

| INFRABEES | +6.18% |

| JUNIORBEES | +5.37% |

| BANKBEES | +4.10% |

| PSUBNKBEES | +3.35% |

| NIFTYBEES | +1.24% |

PSEs… because this time its different.

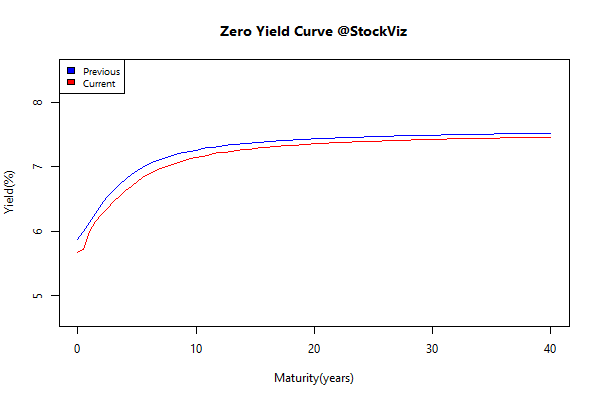

Yield Curve

Bond Indices

| Sub Index | Change in YTM | Total Return(%) |

|---|---|---|

| 0 5 | +0.23 | -0.11% |

| 5 10 | +0.16 | -0.31% |

| 10 15 | +0.11 | -0.40% |

| 15 20 | +0.06 | +0.07% |

| 20 30 | +0.10 | -0.45% |

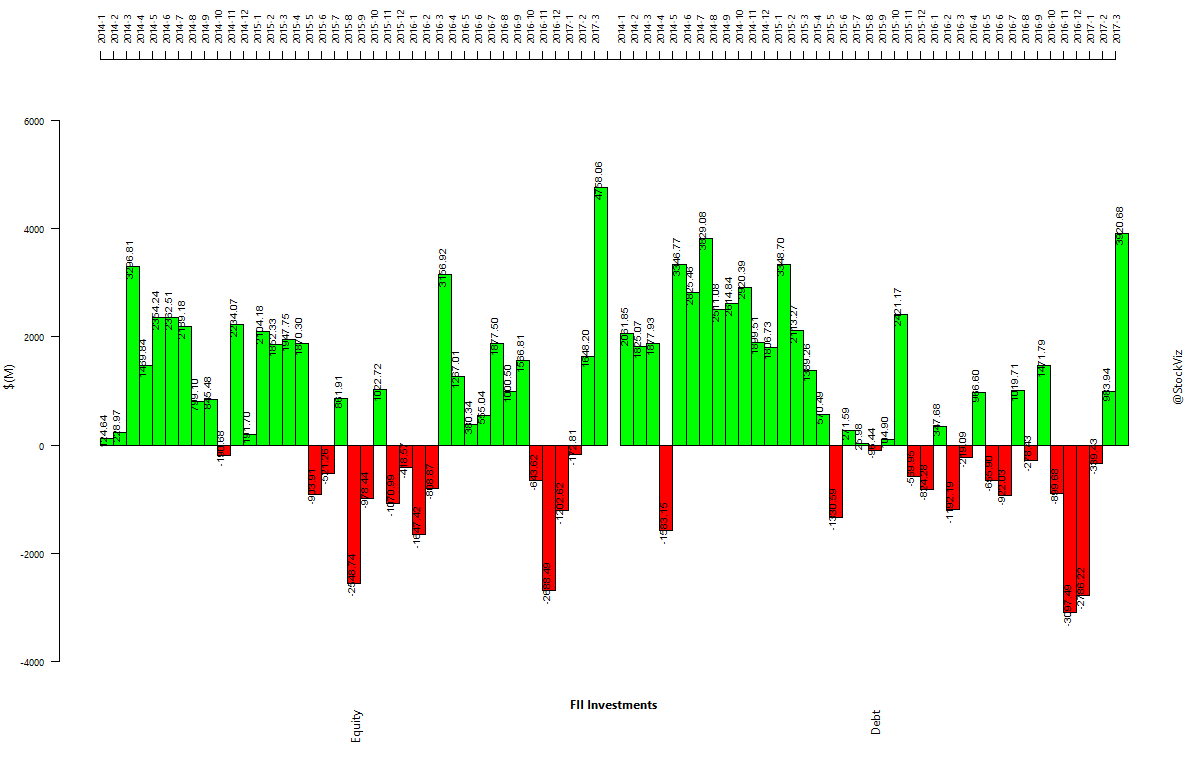

Bonds down in spite of increased FII flows…

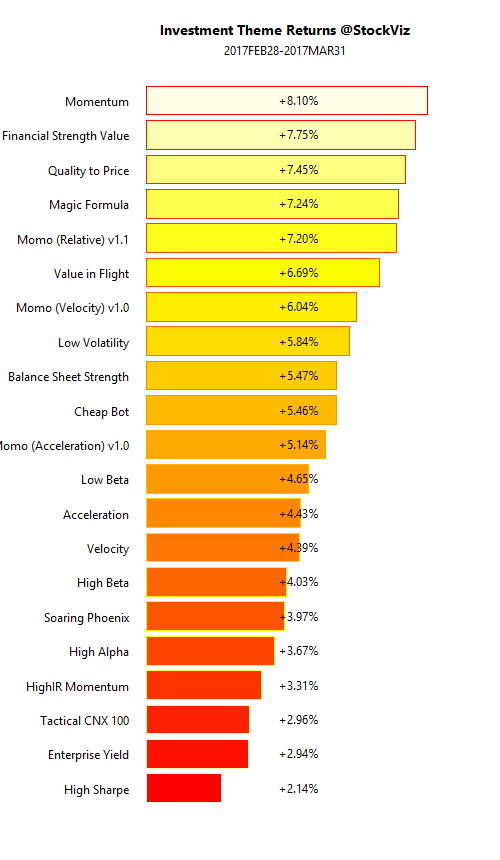

Investment Theme Performance

| Quality to Price | +10.46% |

| Value in Flight | +8.81% |

| Financial Strength Value | +8.80% |

| Momo (Relative) v1.1 | +7.68% |

| Momo (Velocity) v1.0 | +7.27% |

| HighIR Momentum | +7.21% |

| Enterprise Yield | +7.18% |

| Magic Formula | +6.93% |

| Balance Sheet Strength | +6.27% |

| Momo (Acceleration) v1.0 | +6.19% |

| Velocity | +5.89% |

| Momentum | +3.75% |

| Acceleration | -1.18% |

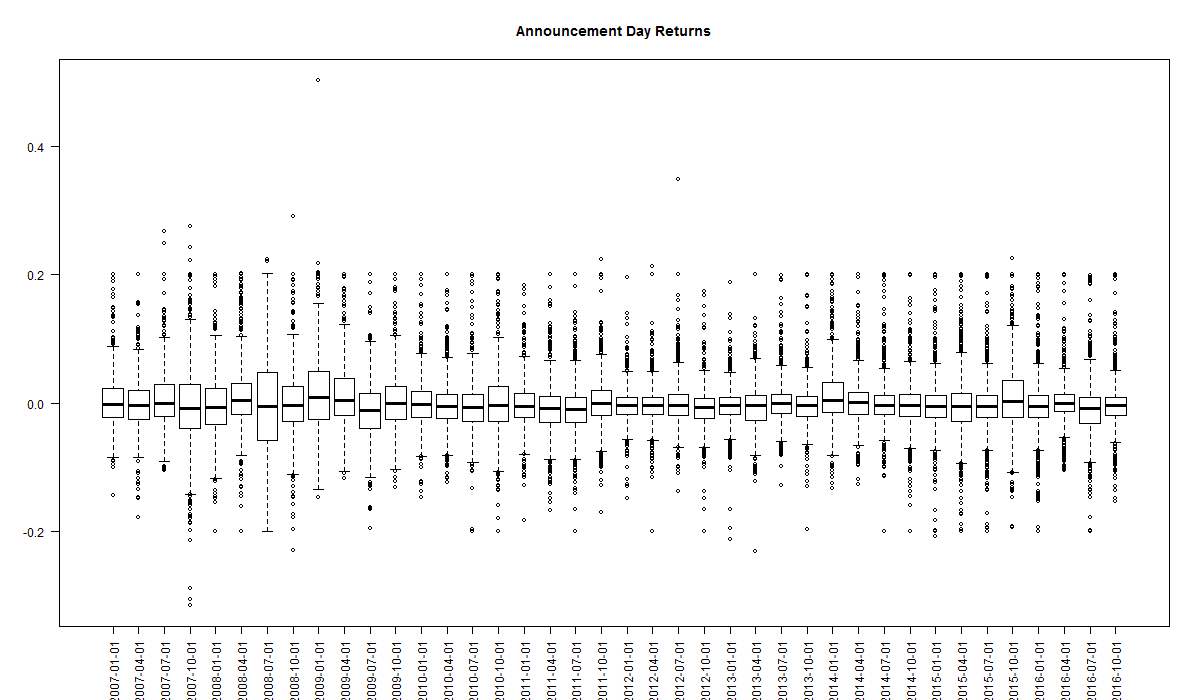

Value themes out-performed momentum…

Equity Mutual Funds

Bond Mutual Funds

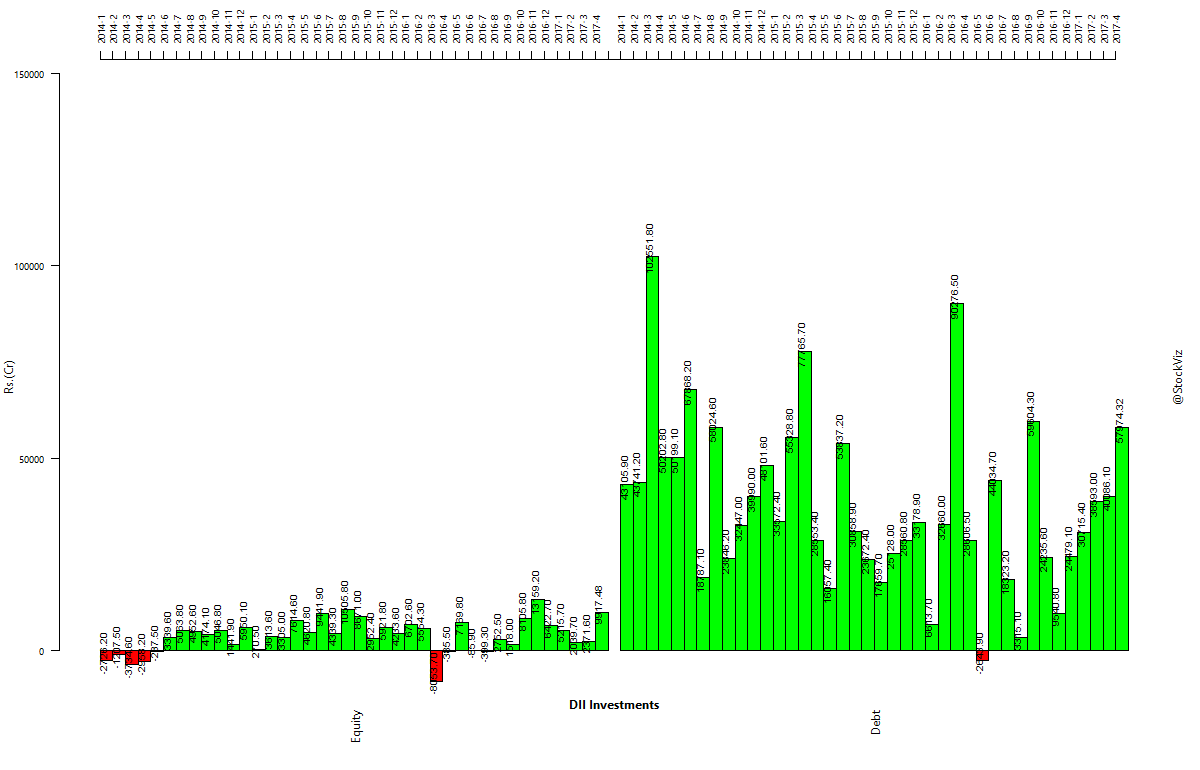

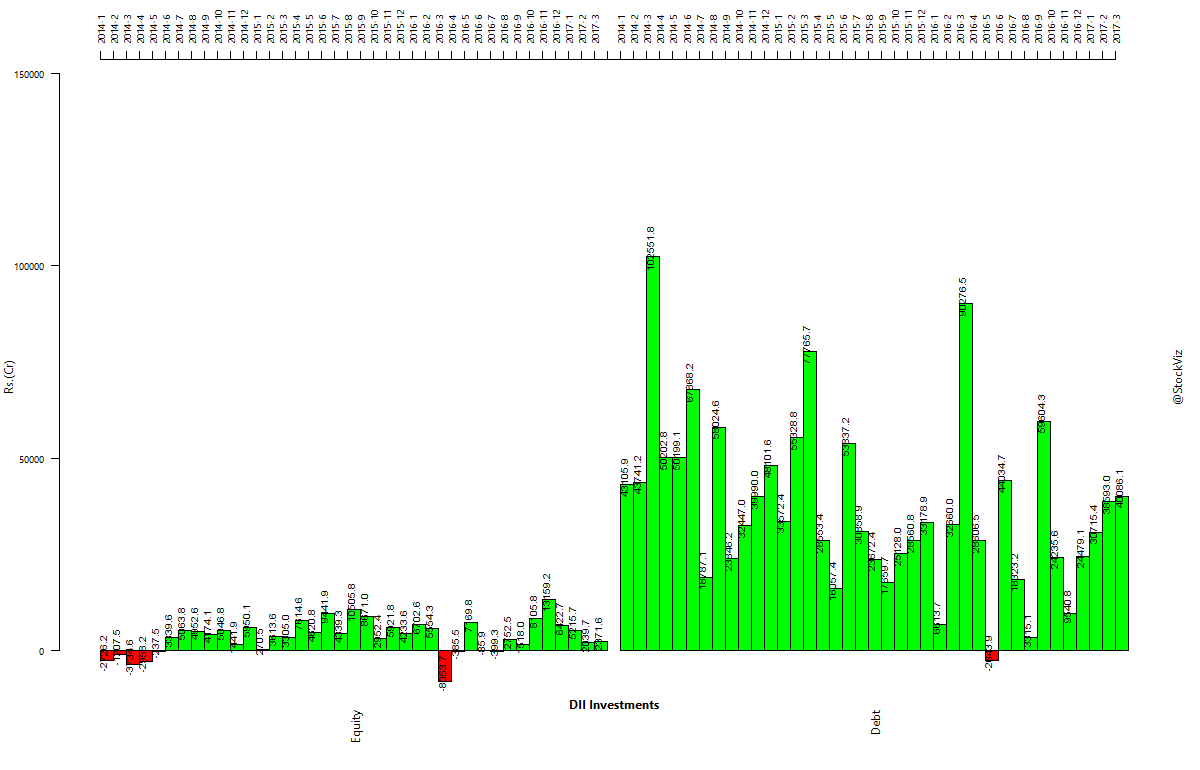

Institutional flows