A yield curve is simply a term structure of interest rates – something you get when you plot rates (y-axis) against the term (x-axis.)

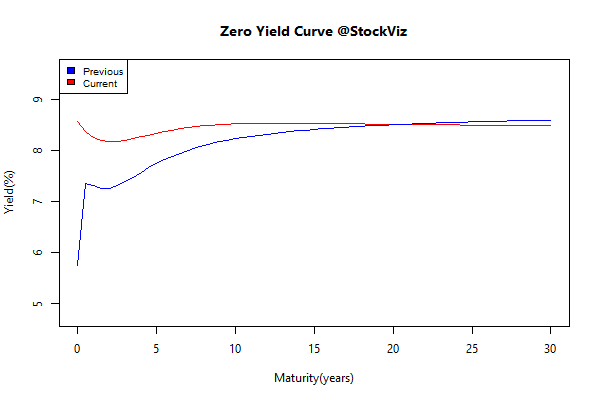

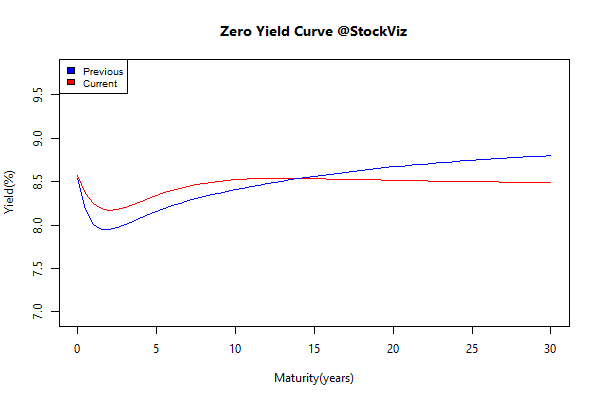

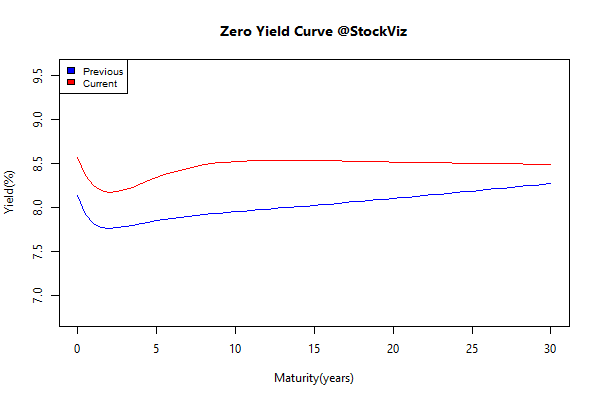

When you lend money to someone, you are taking two types of risk: rate risk and credit risk. This shows up in the chart as a curve that slopes up and two the right (to compensate for the former) and as a higher spread for riskier credit (to compensate for the latter.) But the shape is not a “universal truth” that always needs to be. For example, here are Indian zero coupon rates over the last 5 years:

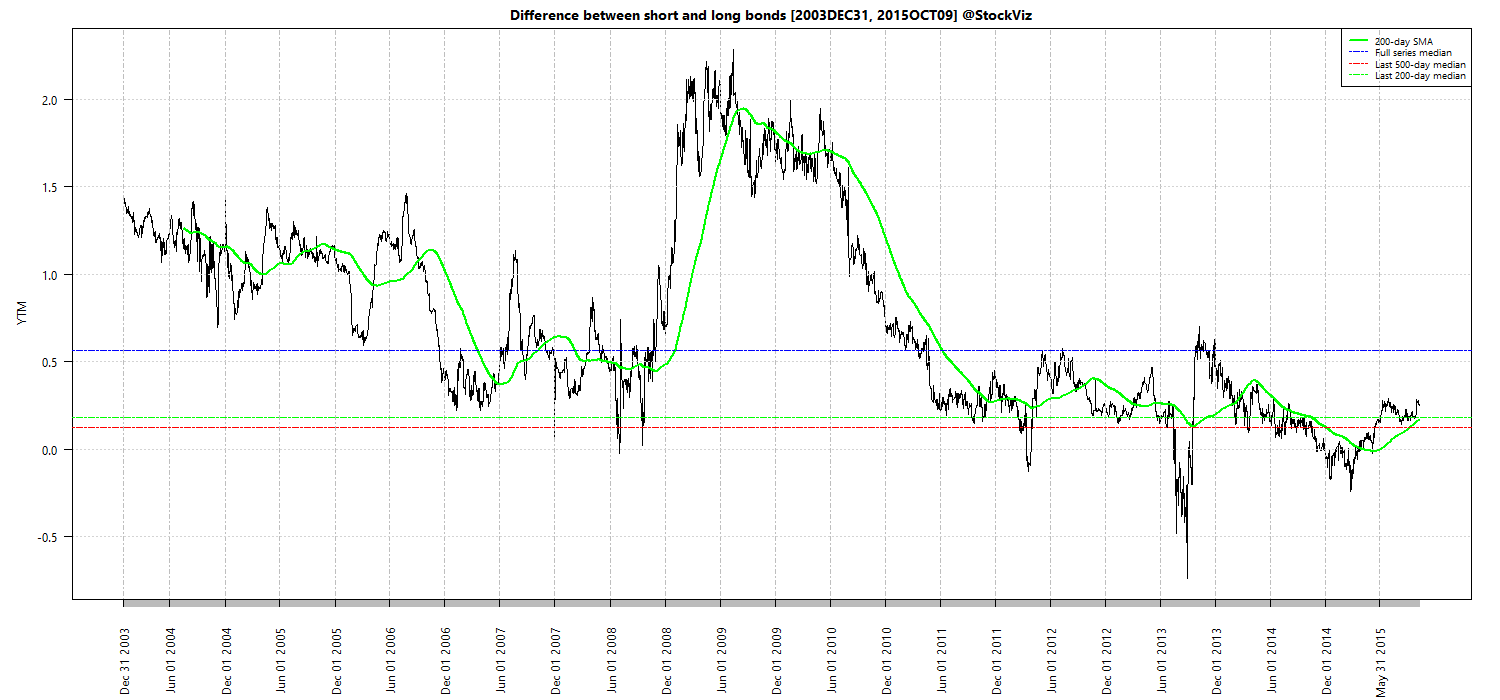

Note how in 2014, the curve was “inverted” – short-term rates were higher than long-term rates. This happens more often than one might think. One way to chart it is as a difference between the 10-year yield and the 2-year yield. If it dips below zero, you know the term-structure was inverted:

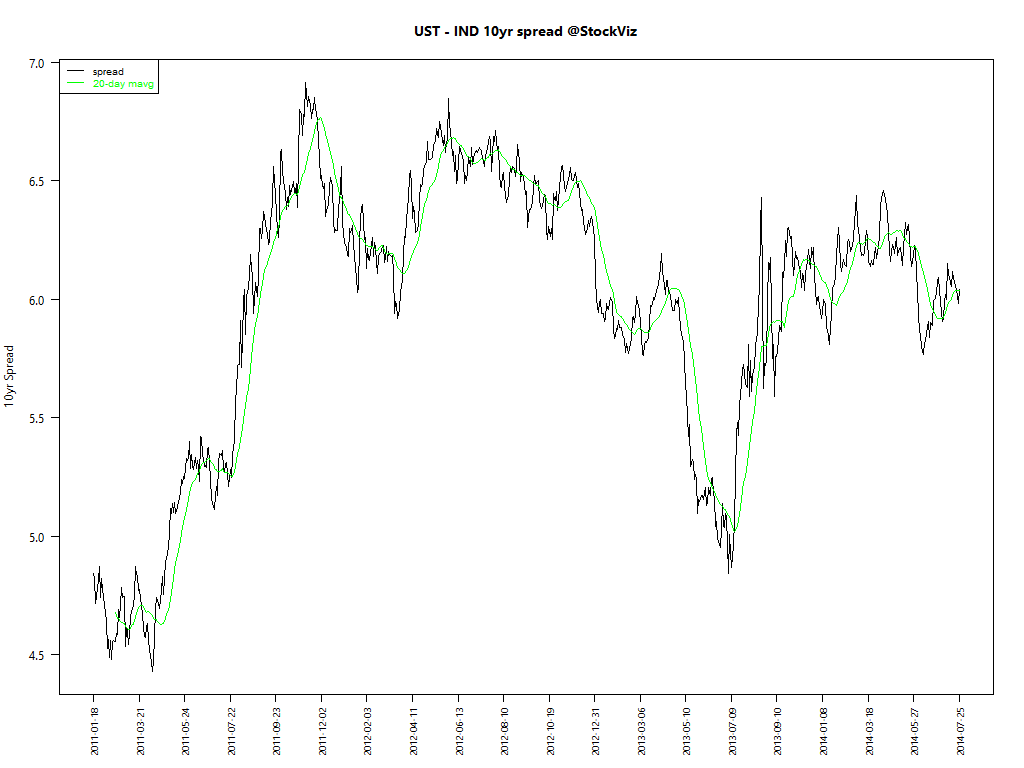

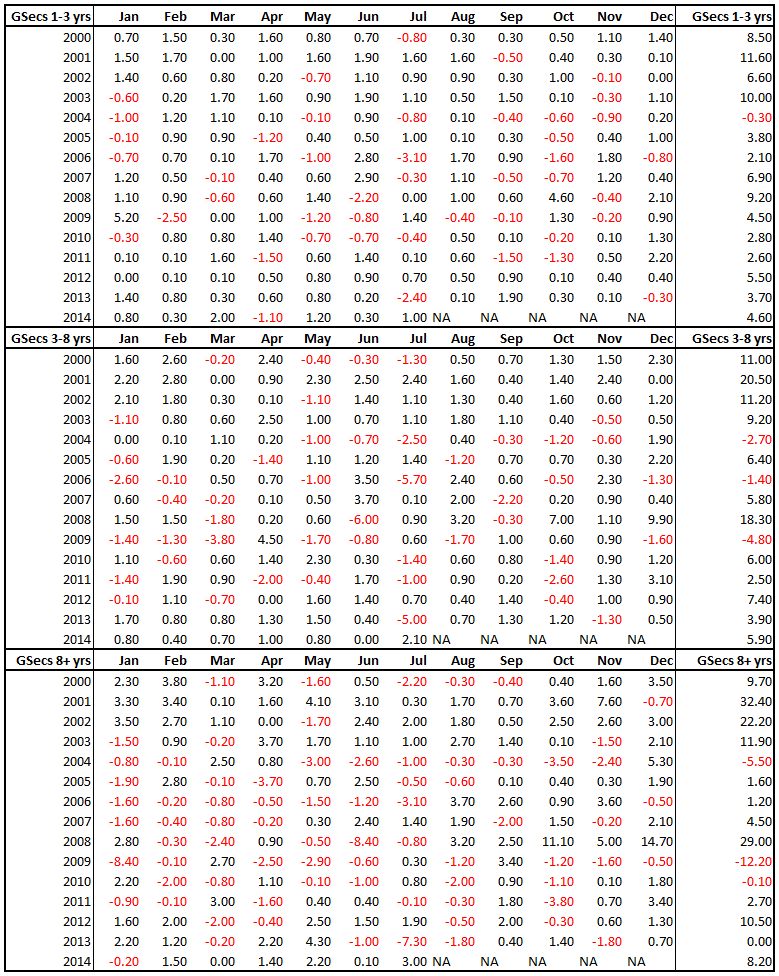

Bonds are not “boring.” Note the volatility in the 10-year yields, not just in Indian bonds but in US and Euro area as well:

Countries in the Euro area have different sovereign credit ratings. So the ECB publishes two rates: one is an aggregation of the whole Euro area and the other that is an aggregation of only the AAA country bonds. The chart above shows how right until the credit crisis hit, AAA and ALL were right on top of each other and then blew out after that point. This is the market realizing that not all Euro area countries are the same.

Although Indian rates have never been negative, the same cannot be said for others. Here is how the Euro yield curve looked like on October 15, 2018:

And until very recently, short term rates in the US were zero:

Corporate bond investors need to be compensated for the credit risk that they take (over and above rate risk.) So corporate bonds tend to trade at a spread over the govvies. They are typically broken up by their credit rating and quoted as a spread:

And the market further differentiates between “developed market” and “emerging market” corporates even within the same credit rating. Here is a chart of AAA spreads for US and EM corporate credit:

The spikes in spreads are the credit crisis rippling through the system.

We publish updated rate, credit and currency charts that all investors should track on our Macro Dashboard. Do check it out.

Code and more charts on github.