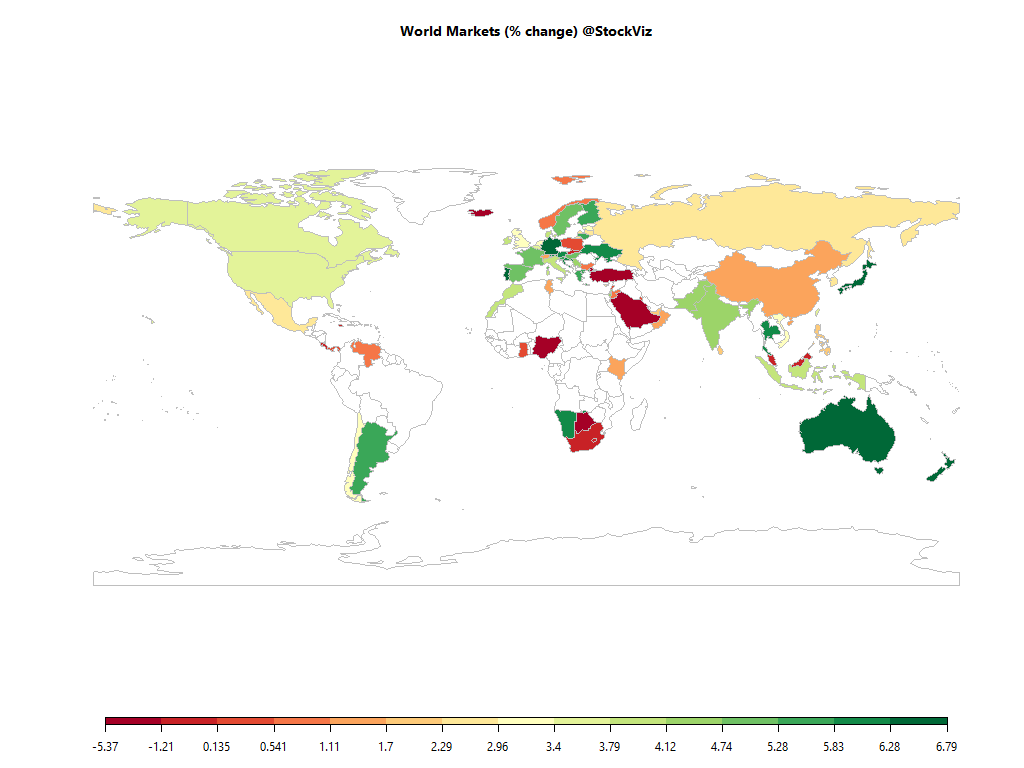

Equities

| MINTs | |

|---|---|

| JCI(IDN) | +2.27% |

| INMEX(MEX) | +2.75% |

| NGSEINDX(NGA) | -1.30% |

| XU030(TUR) | +1.00% |

| BRICS | |

|---|---|

| IBOV(BRA) | +0.94% |

| SHCOMP(CHN) | +2.82% |

| NIFTY(IND) | +1.58% |

| INDEXCF(RUS) | +1.42% |

| TOP40(ZAF) | +0.85% |

Commodities

| Energy | |

|---|---|

| Natural Gas | -0.69% |

| RBOB Gasoline | -0.19% |

| Heating Oil | +11.14% |

| Brent Crude Oil | +10.07% |

| Ethanol | -0.84% |

| WTI Crude Oil | +7.29% |

| Metals | |

|---|---|

| Copper | -6.31% |

| Palladium | -5.11% |

| Platinum | -8.49% |

| Silver 5000oz | -7.46% |

| Gold 100oz | -3.40% |

Currencies

| MINTs | |

|---|---|

| USDIDR(IDN) | +1.20% |

| USDMXN(MEX) | +0.18% |

| USDNGN(NGA) | -1.33% |

| USDTRY(TUR) | -1.05% |

| BRICS | |

|---|---|

| USDBRL(BRA) | -0.46% |

| USDCNY(CHN) | +0.68% |

| USDINR(IND) | -0.01% |

| USDRUB(RUS) | -1.05% |

| USDZAR(ZAF) | +5.87% |

| Agricultural | |

|---|---|

| Cocoa | +2.62% |

| Coffee (Robusta) | +0.66% |

| Lean Hogs | -9.28% |

| Lumber | -1.94% |

| Soybean Meal | -9.74% |

| Soybeans | -6.59% |

| Sugar #11 | +6.33% |

| Wheat | -10.45% |

| Coffee (Arabica) | +0.38% |

| Cattle | -5.85% |

| Corn | -8.47% |

| Cotton | -11.20% |

| Feeder Cattle | +0.24% |

| Orange Juice | +3.55% |

| White Sugar | +1.48% |

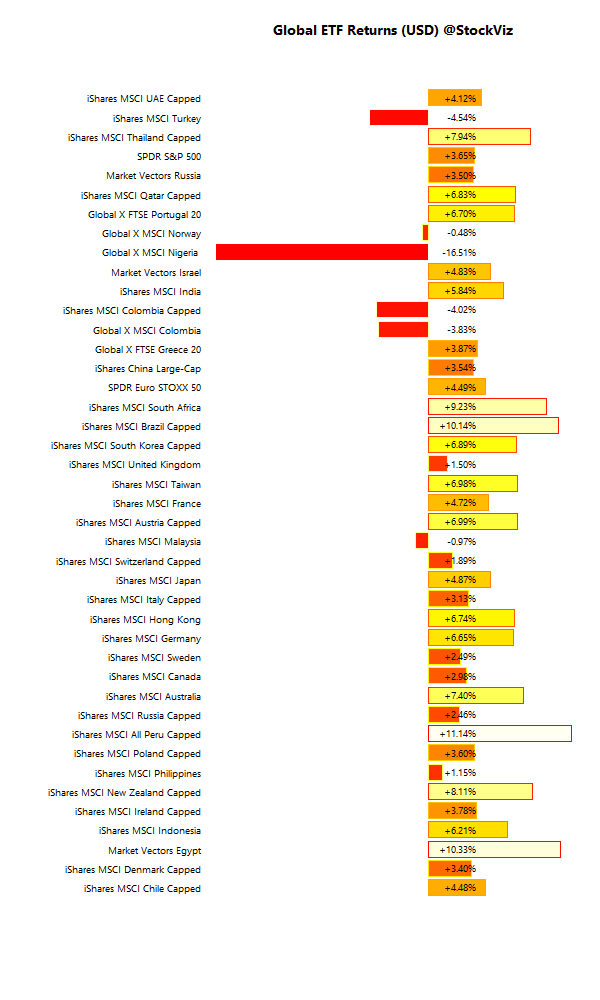

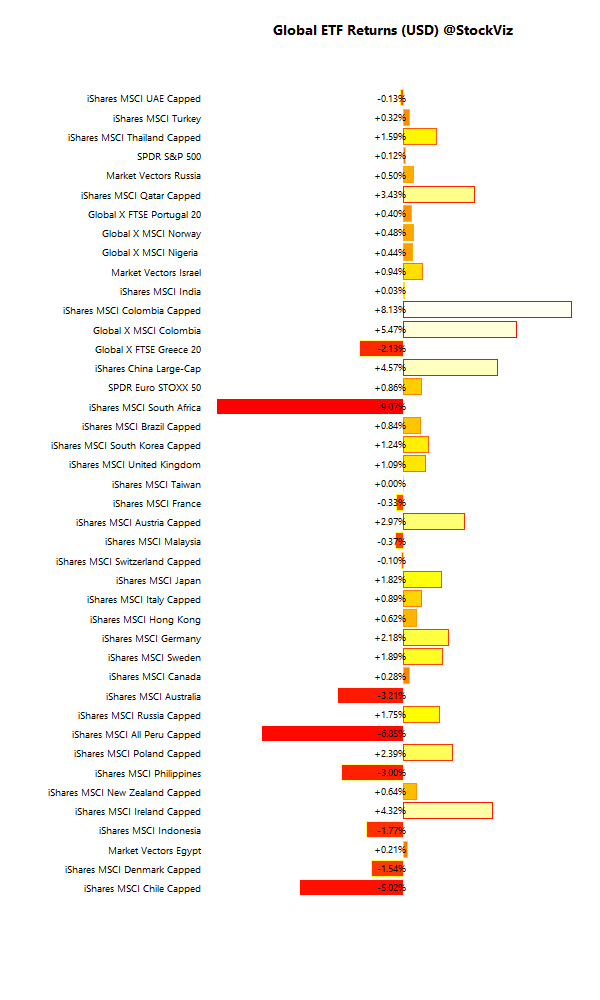

International ETFs (USD)

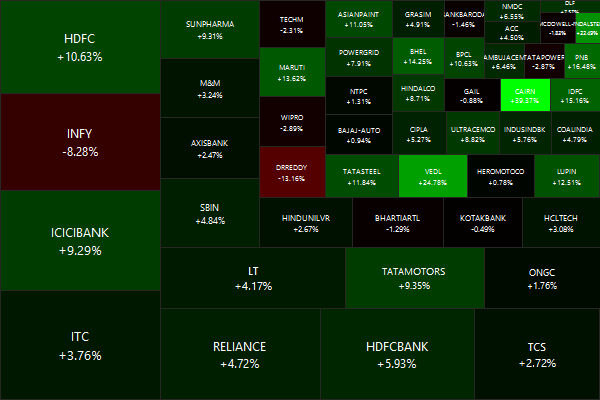

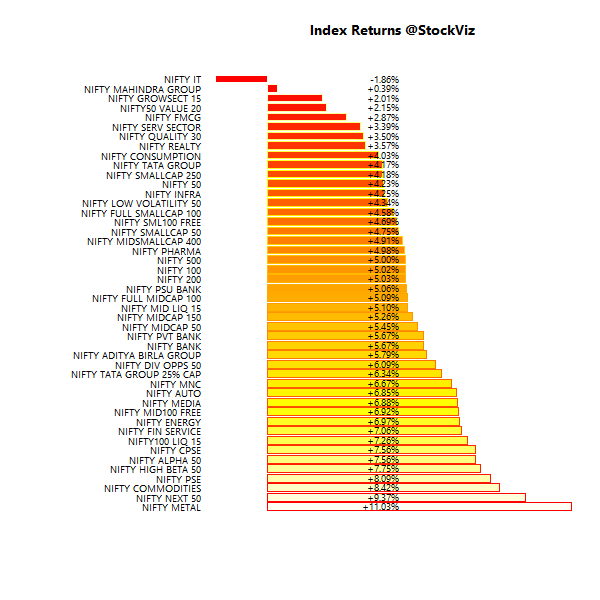

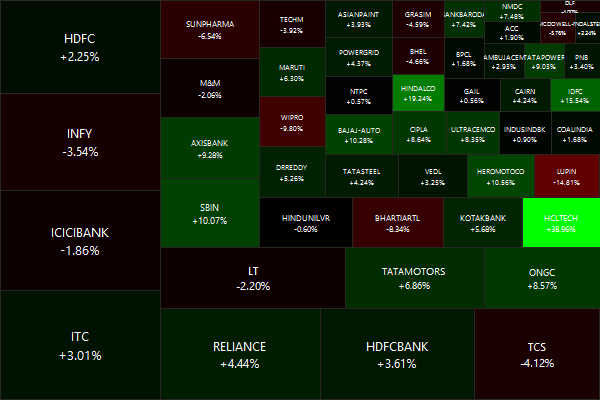

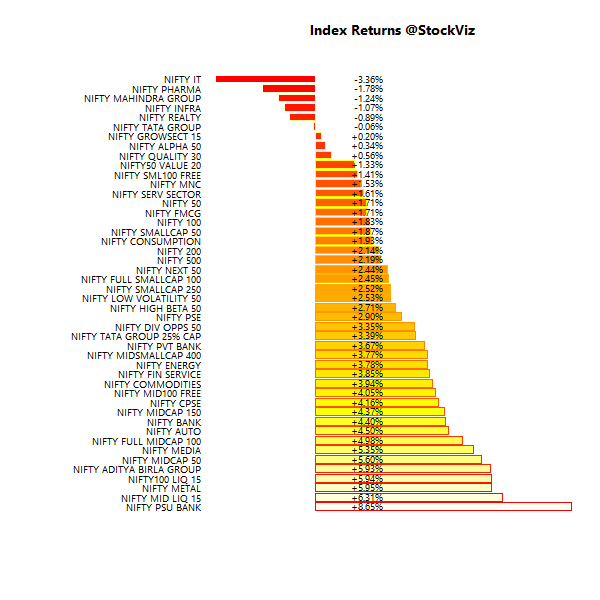

Nifty Heatmap

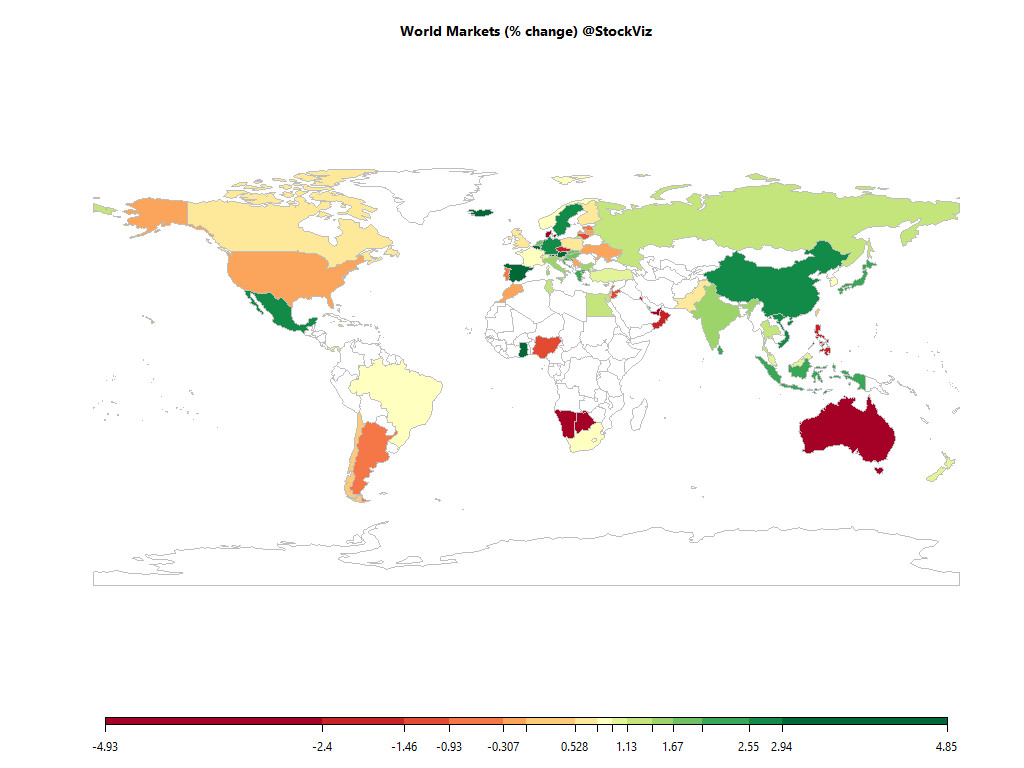

Index Returns

More: Sector Dashboard

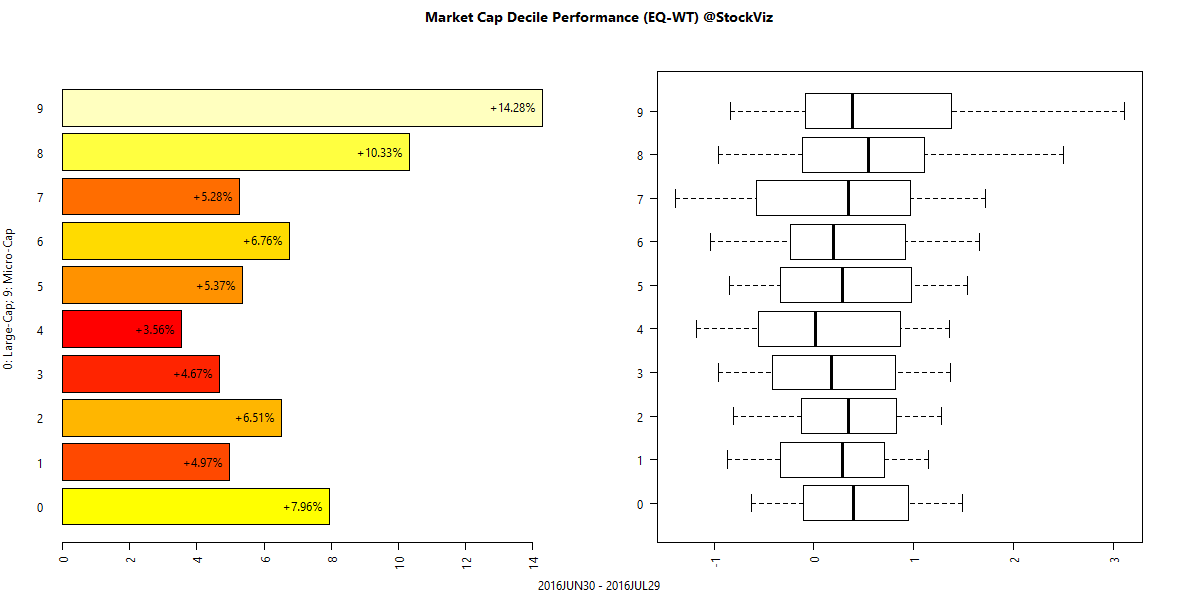

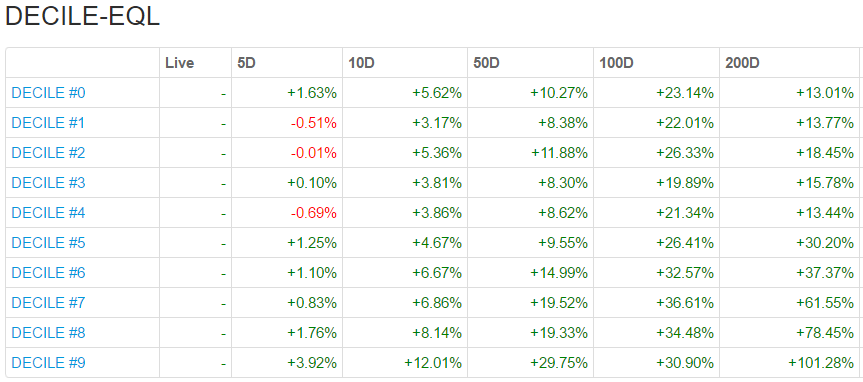

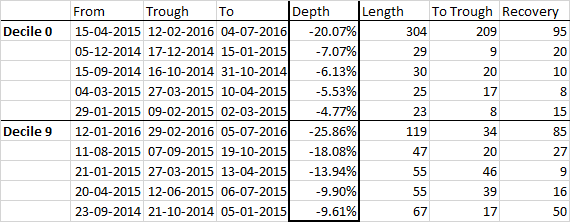

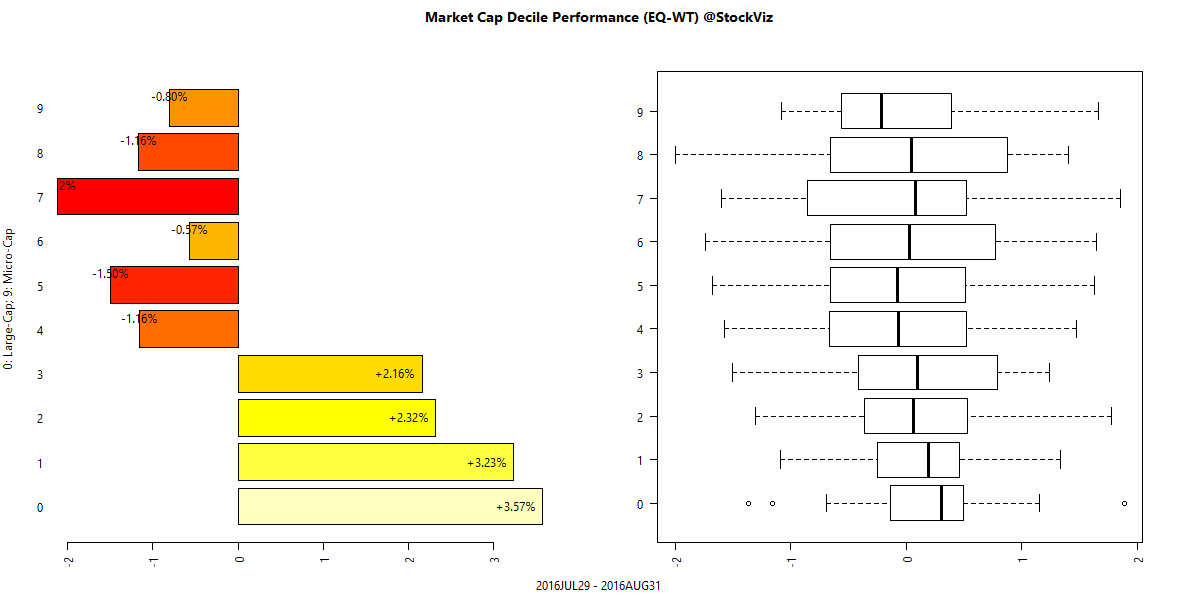

Market Cap Decile Performance

More: Equal-Weight Deciles, Cap-Weight Deciles

ETF Performance

| PSUBNKBEES | +8.23% |

| CPSEETF | +4.57% |

| BANKBEES | +4.07% |

| JUNIORBEES | +2.43% |

| NIFTYBEES | +1.71% |

| GOLDBEES | +0.56% |

| INFRABEES | +0.27% |

PSU banks – because it is a new beginning!

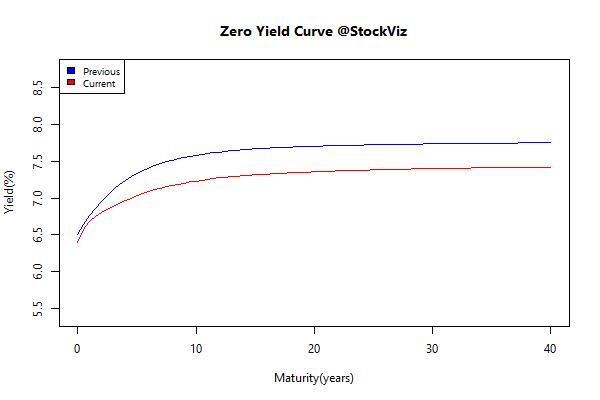

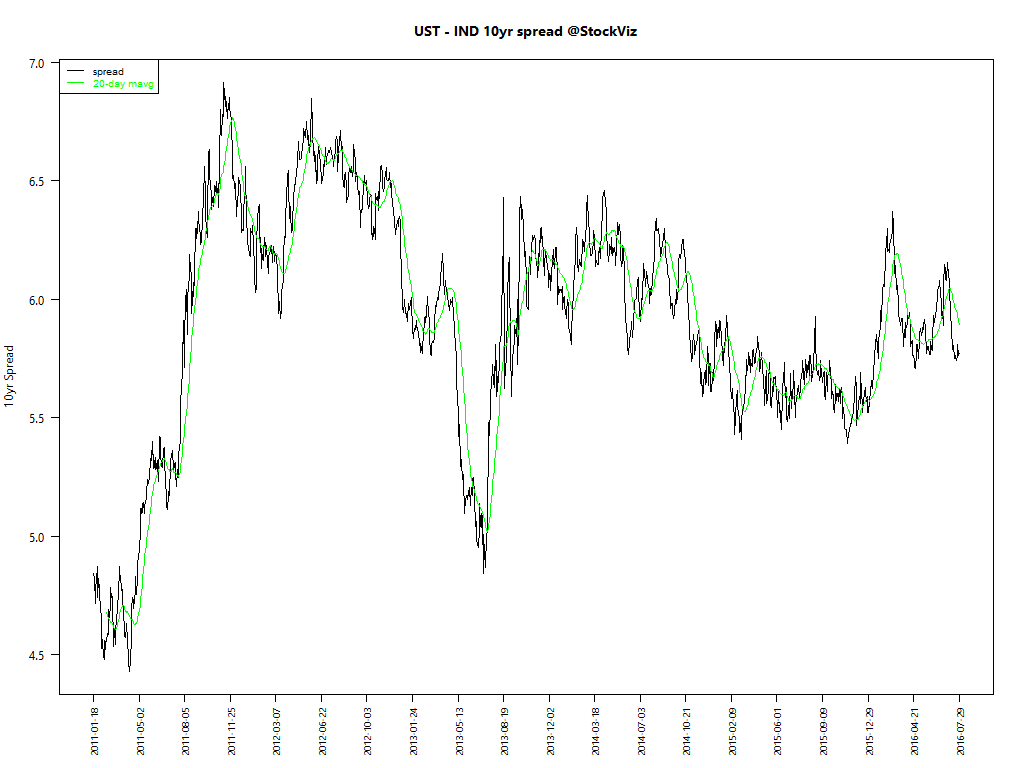

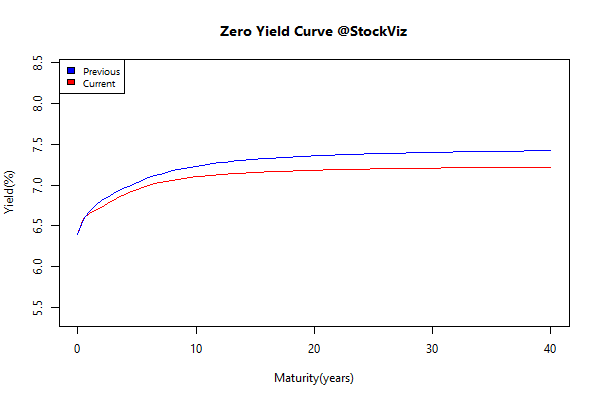

Yield Curve

Bond Indices

| Sub Index | Change in YTM | Total Return(%) |

|---|---|---|

| 0 5 | -0.03 | +0.67% |

| 5 10 | -0.10 | +1.23% |

| 10 15 | -0.18 | +1.99% |

| 15 20 | -0.16 | +2.11% |

| 20 30 | -0.16 | +2.45% |

Long bond FTW!!!

Investment Theme Performance

| Magic Formula | +9.20% |

| Quality to Price | +3.00% |

| HighIR Momentum | +2.02% |

| Momentum | +1.99% |

| Momo (Relative) v1.1 | +1.85% |

| Balance Sheet Strength | +1.77% |

| Acceleration | +0.39% |

| Momo (Acceleration) v1.0 | +0.36% |

| Enterprise Yield | -1.60% |

| Financial Strength Value | -2.87% |

| Momo (Velocity) v1.0 | -3.18% |

| Velocity | -4.67% |

Magic Formula got its mojo back…

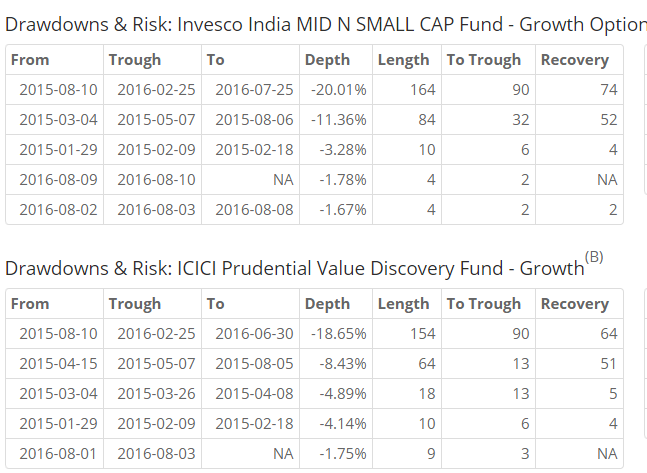

Equity Mutual Funds

Bond Mutual Funds

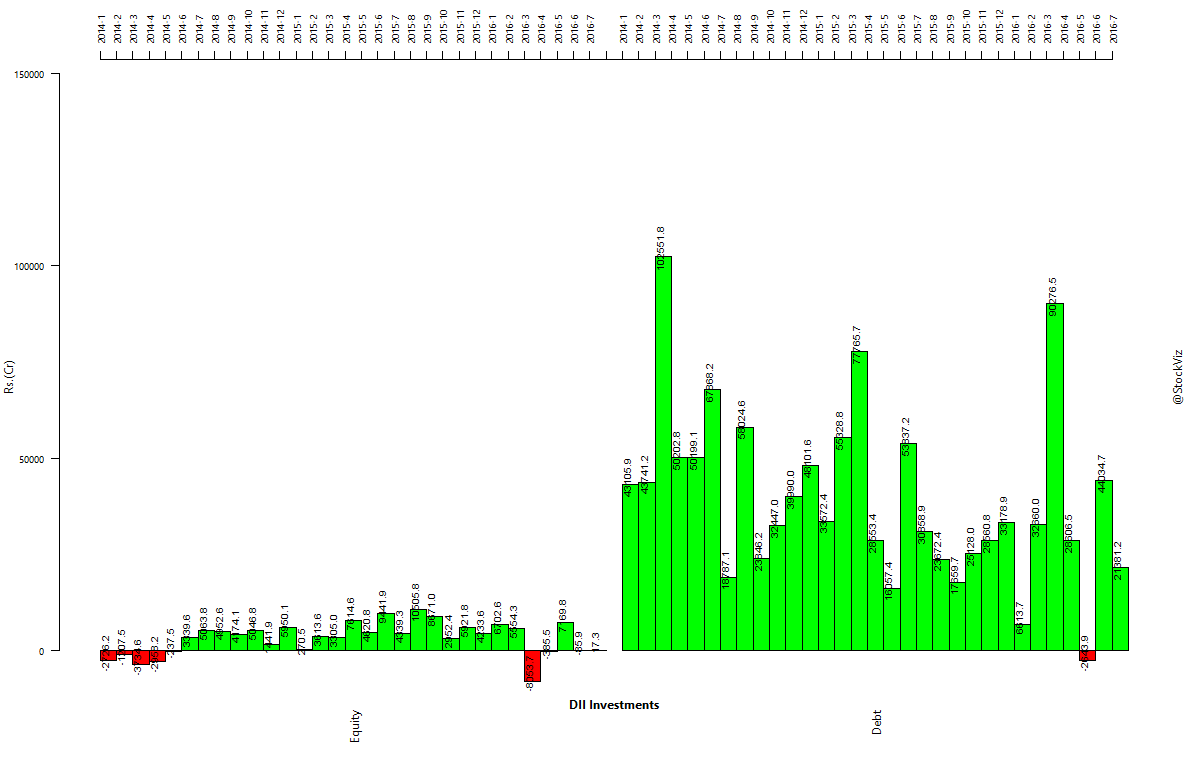

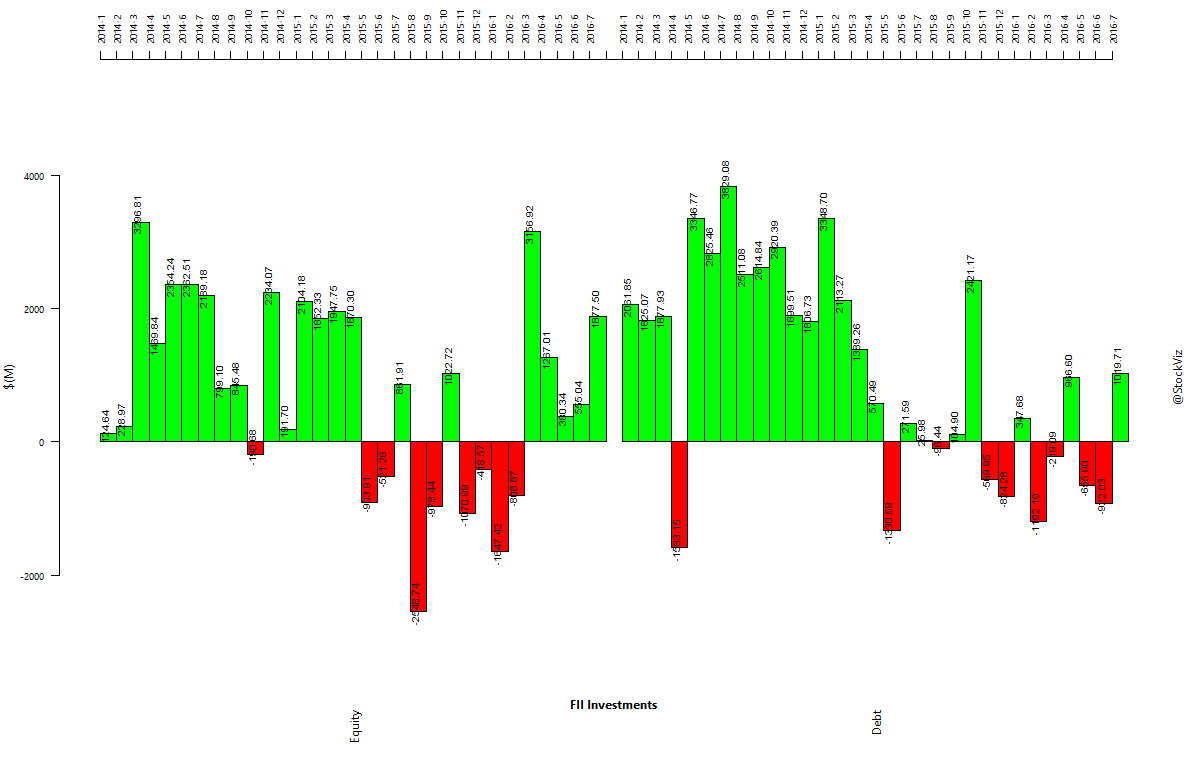

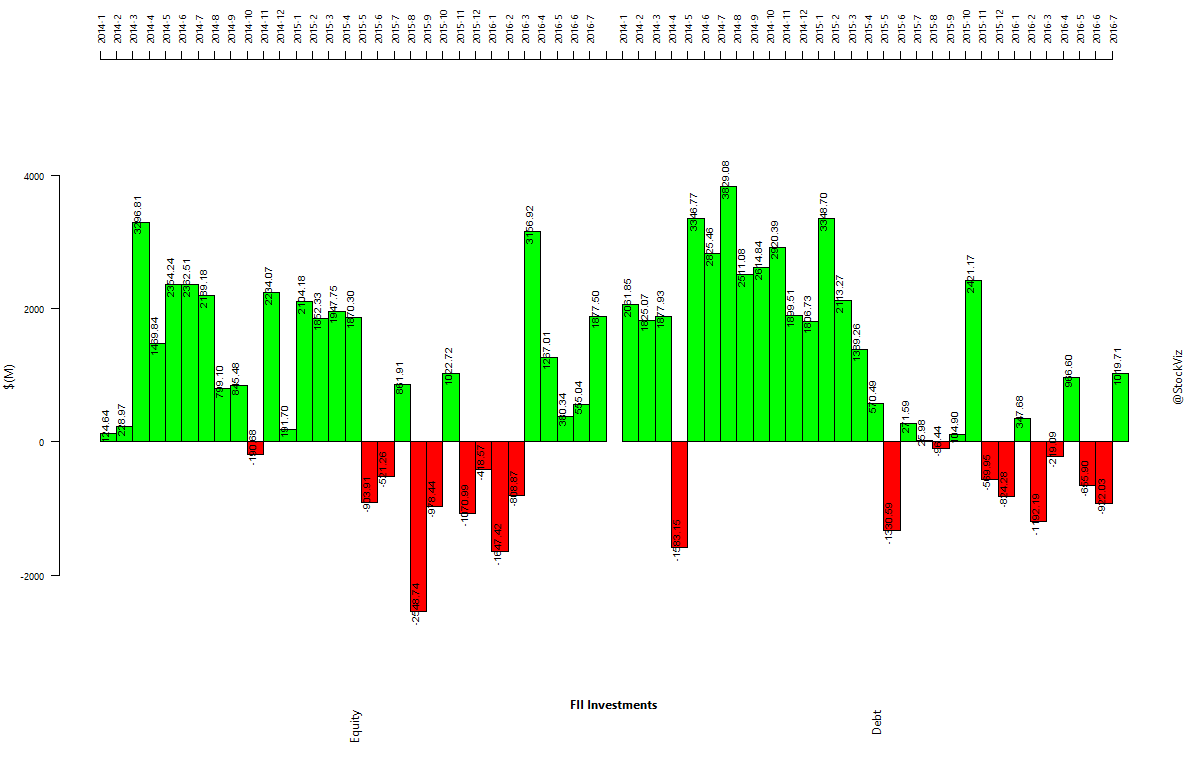

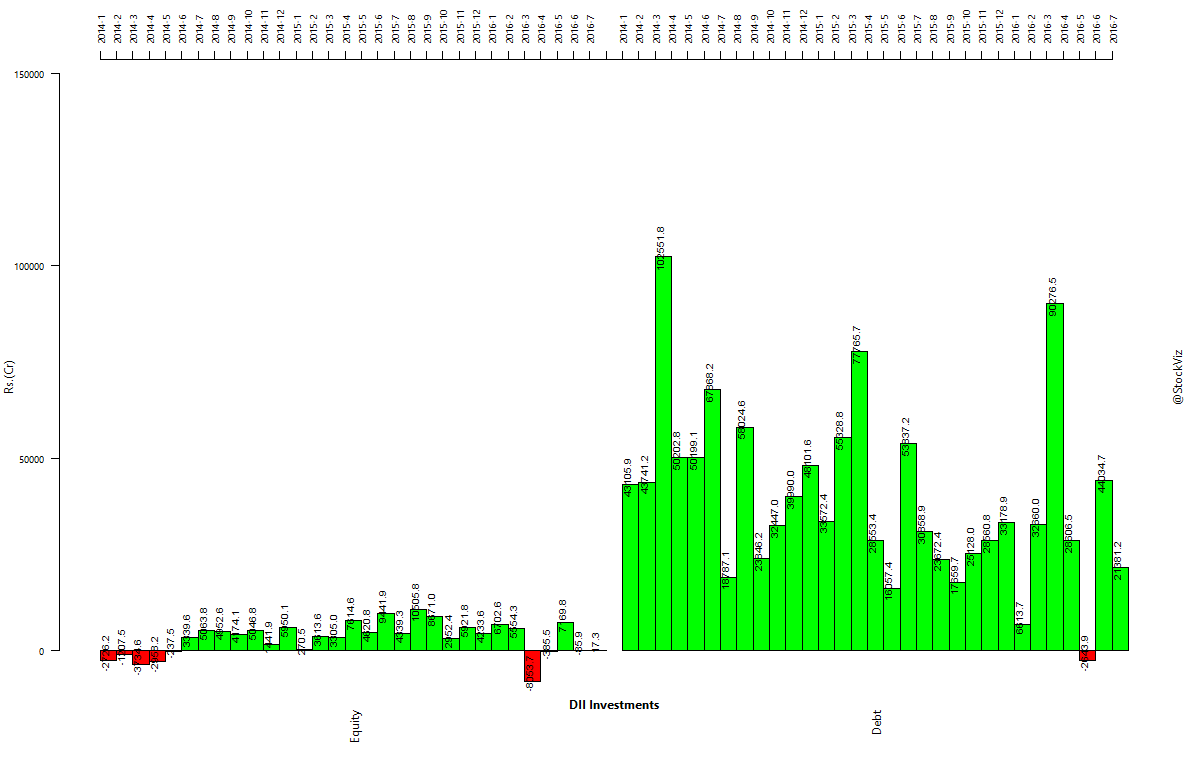

Institutional Investment Trends

FII’s binged on both debt and equity this month…

Book of the Month

The Everything Store: Jeff Bezos and the Age of Amazon (Amazon)

The book is about the rise of Amazon and how it is more or less an extension of Jeff Bezos’ brain. After reading this, I realized how difficult it is going to be for our domestic e-commerce players to win against the Bezos juggernaut. It is a well written book and is a must-read for anyone who is interested in business strategy.