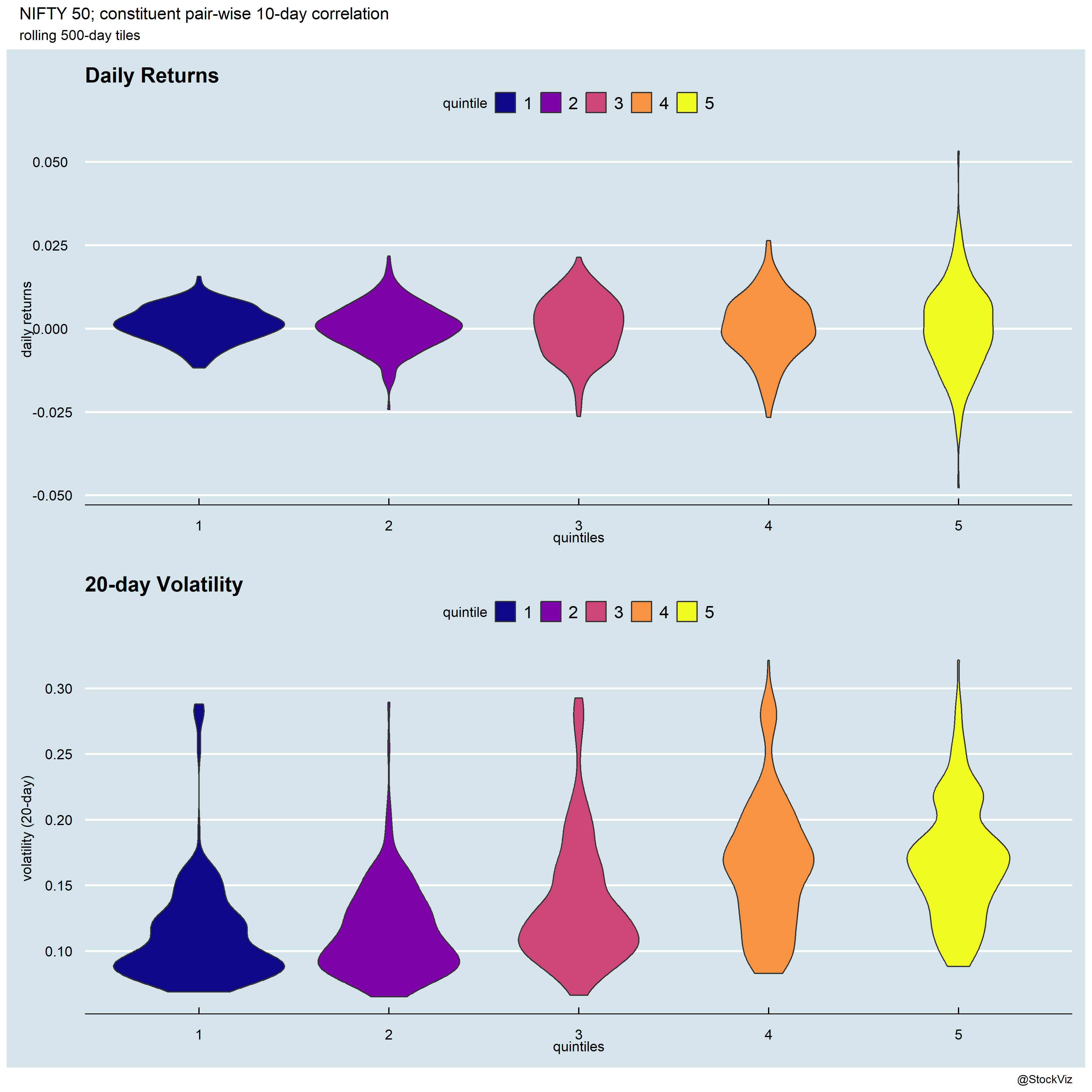

Volatility is calculated over a time period – the lookback. While developing a strategy, it is typical to try a range of lookbacks and pick one that looks reasonable for the strategy being built. However, is there an “ideal” lookback period?

This is where a volatility signature plot comes into the picture. It is typically used in high frequency trading but there is no reason not to use it on a lower frequency time series.

If you plot the distribution of volatility over different lookbacks, this is how it looks:

Ideally, you want the box to be small, the median in the middle and the wicks to be short. After all, if you are using volatility to drive a strategy, if the distribution of volatility itself is too wonky, then how do you trust the output?