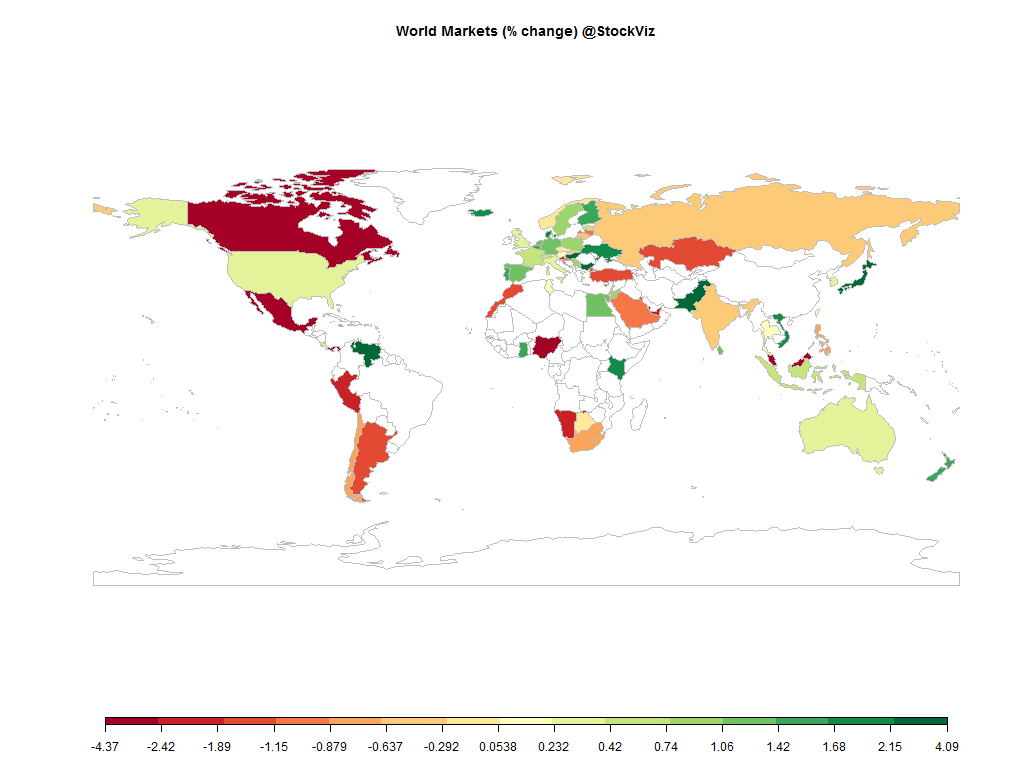

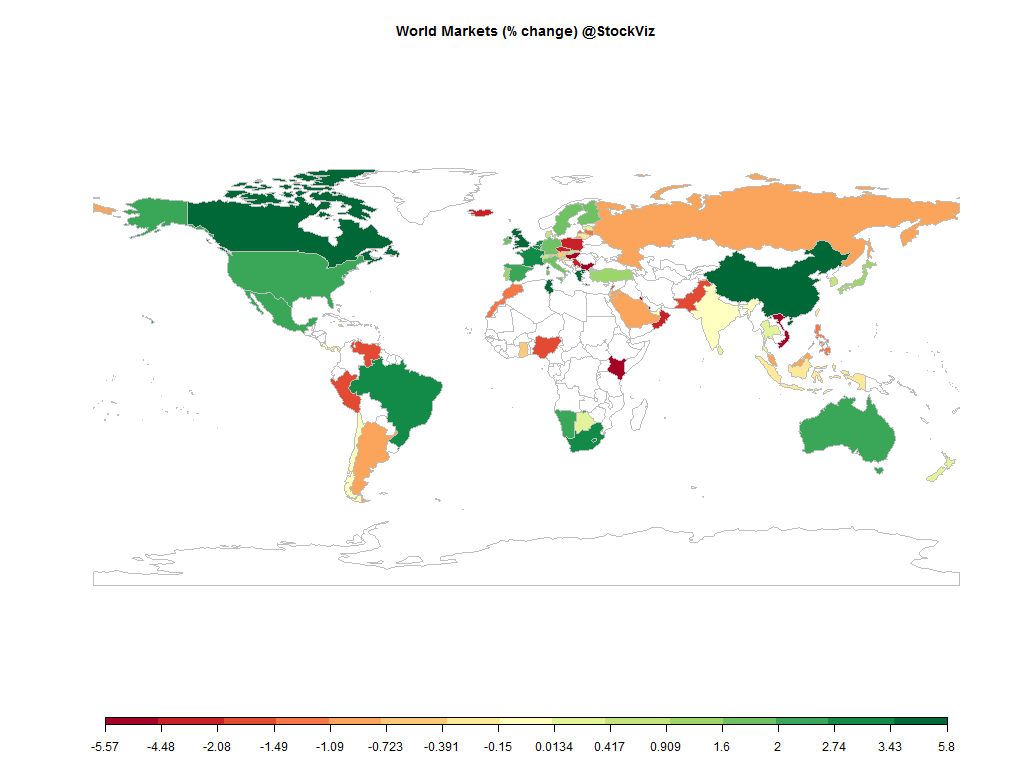

Equities

| MINTs | |

|---|---|

| JCI(IDN) | -0.31% |

| INMEX(MEX) | +2.18% |

| NGSEINDX(NGA) | -1.49% |

| XU030(TUR) | +0.92% |

| BRICS | |

|---|---|

| IBOV(BRA) | +3.43% |

| SHCOMP(CHN) | +5.80% |

| NIFTY(IND) | +0.01% |

| INDEXCF(RUS) | -0.72% |

| TOP40(ZAF) | +2.96% |

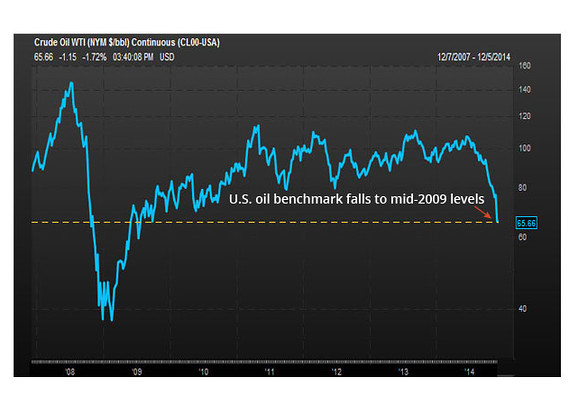

Commodities

| Energy | |

|---|---|

| Ethanol | -5.78% |

| WTI Crude Oil | -0.41% |

| RBOB Gasoline | -1.60% |

| Brent Crude Oil | -1.00% |

| Heating Oil | -2.34% |

| Natural Gas | -8.76% |

| Metals | |

|---|---|

| Gold 100oz | -2.18% |

| Palladium | -1.18% |

| Platinum | -2.83% |

| Copper | -0.68% |

| Silver 5000oz | -7.02% |

Currencies

| MINTs | |

|---|---|

| USDIDR(IDN) | +0.24% |

| USDMXN(MEX) | -0.68% |

| USDNGN(NGA) | +0.83% |

| USDTRY(TUR) | +0.75% |

| BRICS | |

|---|---|

| USDBRL(BRA) | +0.32% |

| USDCNY(CHN) | +0.53% |

| USDINR(IND) | +1.61% |

| USDRUB(RUS) | +2.29% |

| USDZAR(ZAF) | -0.08% |

| Agricultural | |

|---|---|

| Cocoa | +3.59% |

| Corn | +3.53% |

| Soybean Meal | -3.96% |

| Soybeans | -1.39% |

| Coffee (Arabica) | +0.57% |

| Cotton | +0.12% |

| Feeder Cattle | -2.39% |

| Orange Juice | -5.25% |

| Sugar #11 | -0.40% |

| Wheat | +0.88% |

| Cattle | -0.34% |

| Coffee (Robusta) | -2.21% |

| Lean Hogs | -6.49% |

| Lumber | +0.29% |

| White Sugar | +0.10% |

Credit Indices

| Index | Change |

|---|---|

| Markit CDX EM | -0.30% |

| Markit CDX NA HY | +0.52% |

| Markit CDX NA IG | +0.73% |

| Markit iTraxx Asia ex-Japan IG | +8.59% |

| Markit iTraxx Australia | +7.20% |

| Markit iTraxx Europe | +4.16% |

| Markit iTraxx Europe Crossover | +16.58% |

| Markit iTraxx Japan | +2.11% |

| Markit iTraxx SovX Western Europe | +2.94% |

| Markit LCDX (Loan CDS) | -0.18% |

| Markit MCDX (Municipal CDS) | +2.46% |

All I can say about this week is that I am glad that its over.

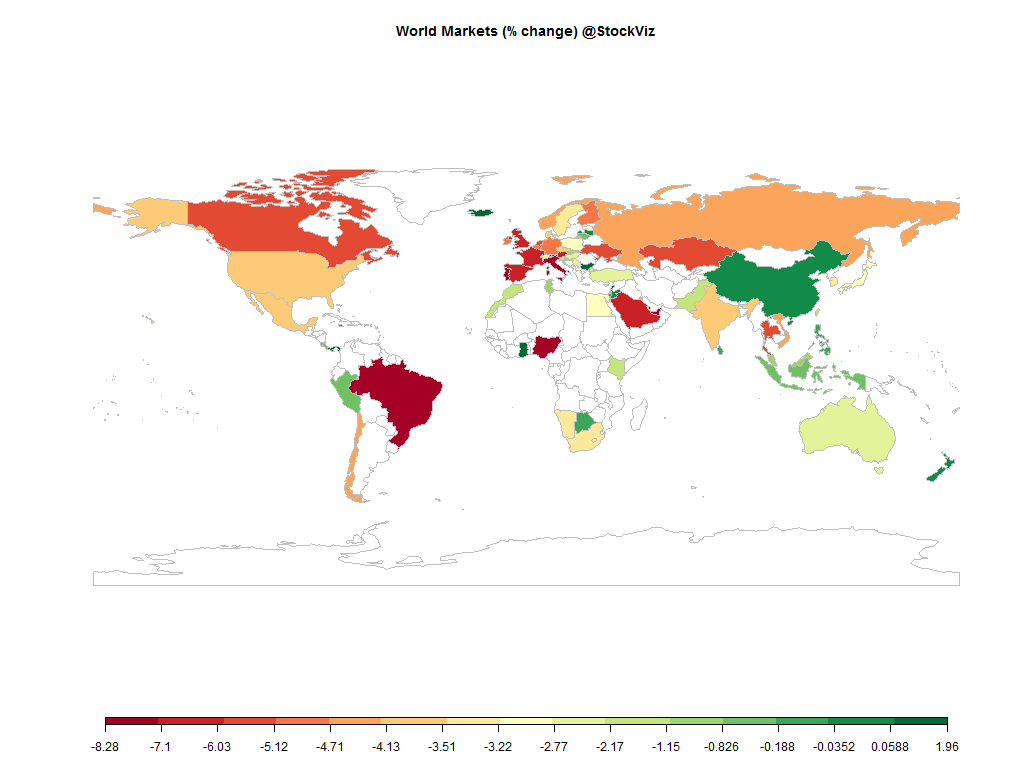

The NIFTY ended flat for the week but that hides the roller-coaster ride it put investors through. After all the oil-related panic, the S&P ended up more than 2% for the week.

Oil ended down, dollar up.

Hopefully Santa visits before expiry.

The NIFTY ended flat for the week but that hides the roller-coaster ride it put investors through. After all the oil-related panic, the S&P ended up more than 2% for the week.

Oil ended down, dollar up.

Hopefully Santa visits before expiry.

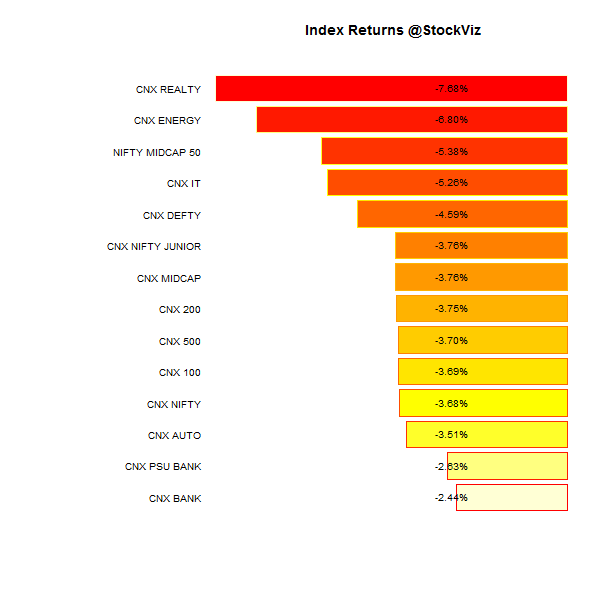

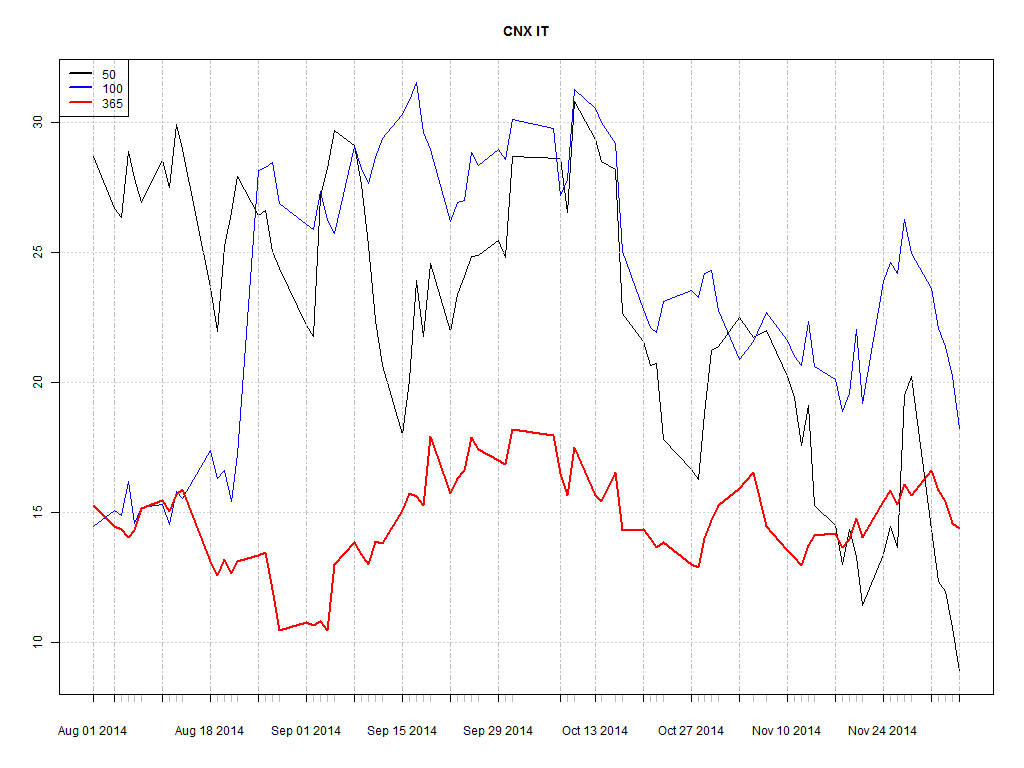

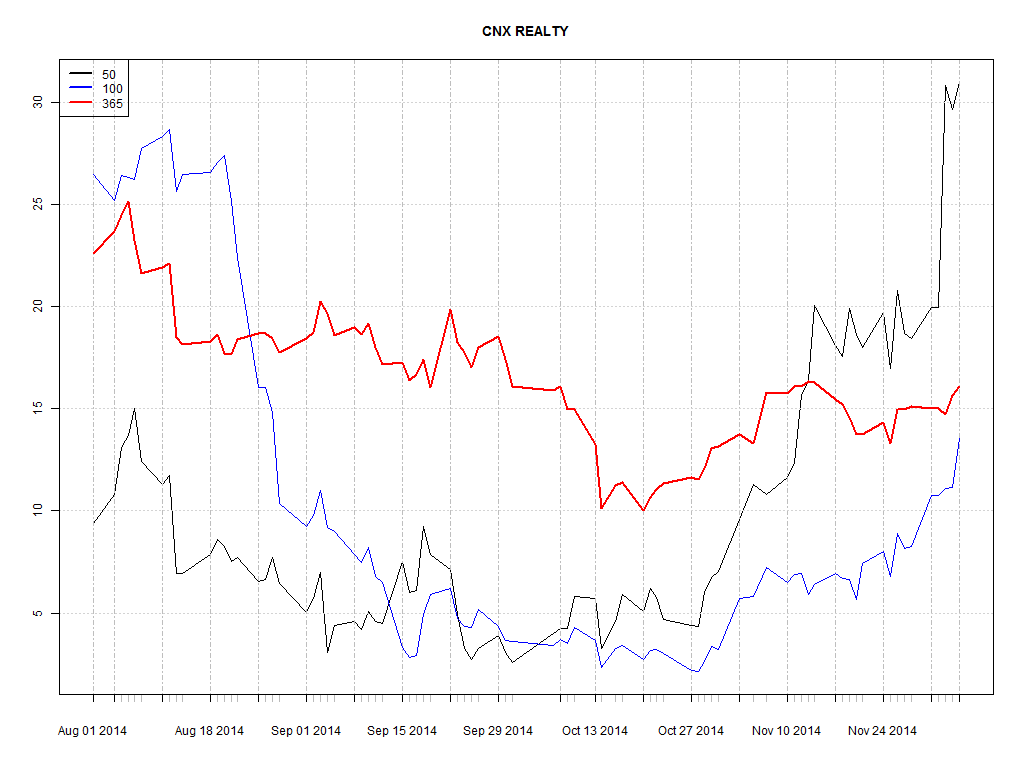

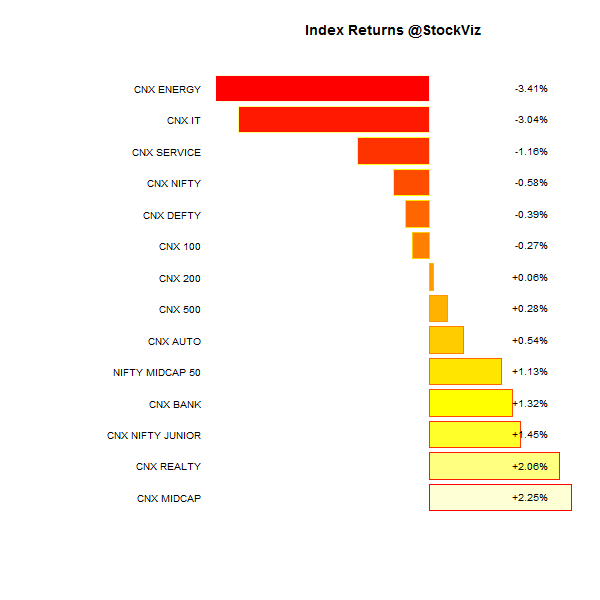

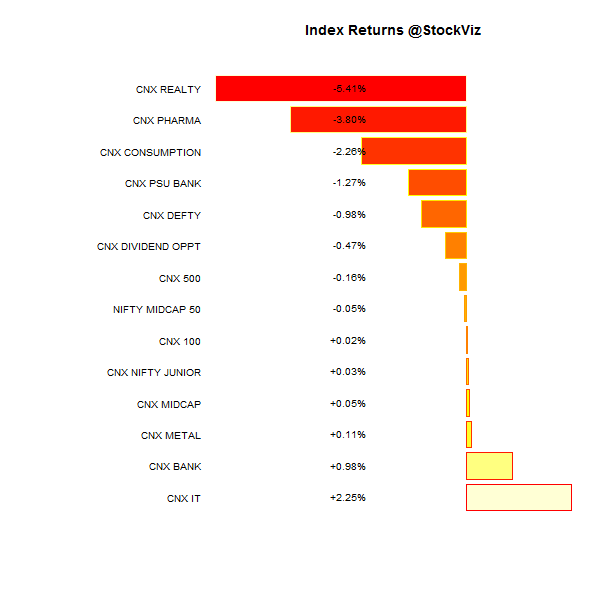

Index Returns

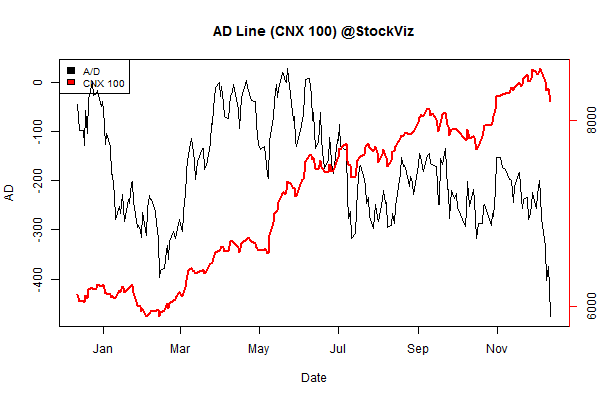

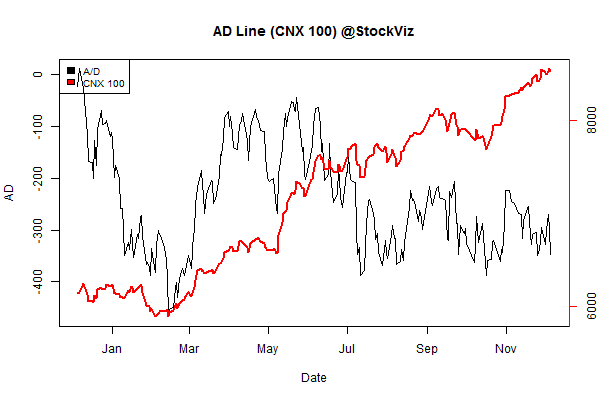

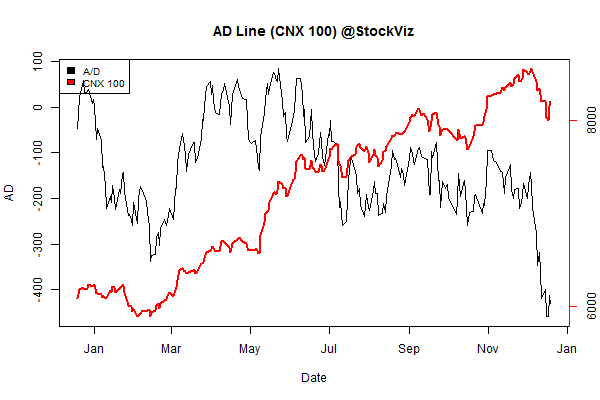

Advance Decline

Market Cap Decile Performance

| Decile | Mkt. Cap. | Adv/Decl |

|---|---|---|

| 1 (micro) | -6.25% | 63/74 |

| 2 | -3.65% | 63/73 |

| 3 | -2.93% | 64/73 |

| 4 | -2.21% | 61/75 |

| 5 | -3.07% | 63/73 |

| 6 | -1.98% | 65/72 |

| 7 | -2.00% | 56/80 |

| 8 | -1.38% | 64/73 |

| 9 | -1.17% | 64/72 |

| 10 (mega) | -0.01% | 68/69 |

The sell-off was brutal below the mega-caps…

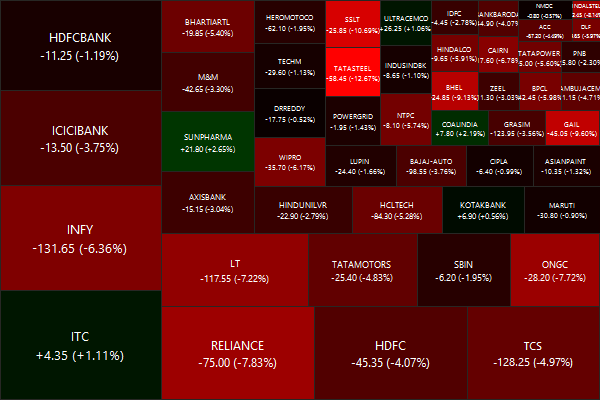

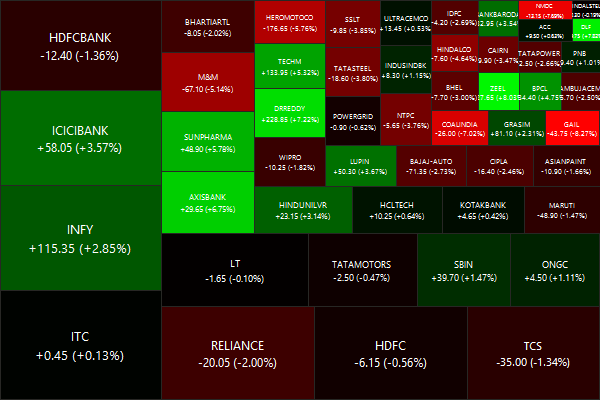

Top Winners and Losers

Broad based action saw a mix of winners and losers…

ETF Performance

| CPSEETF | +3.32% |

| BANKBEES | +0.98% |

| INFRABEES | +0.54% |

| NIFTYBEES | -0.03% |

| JUNIORBEES | -0.22% |

| GOLDBEES | -0.99% |

| PSUBNKBEES | -1.93% |

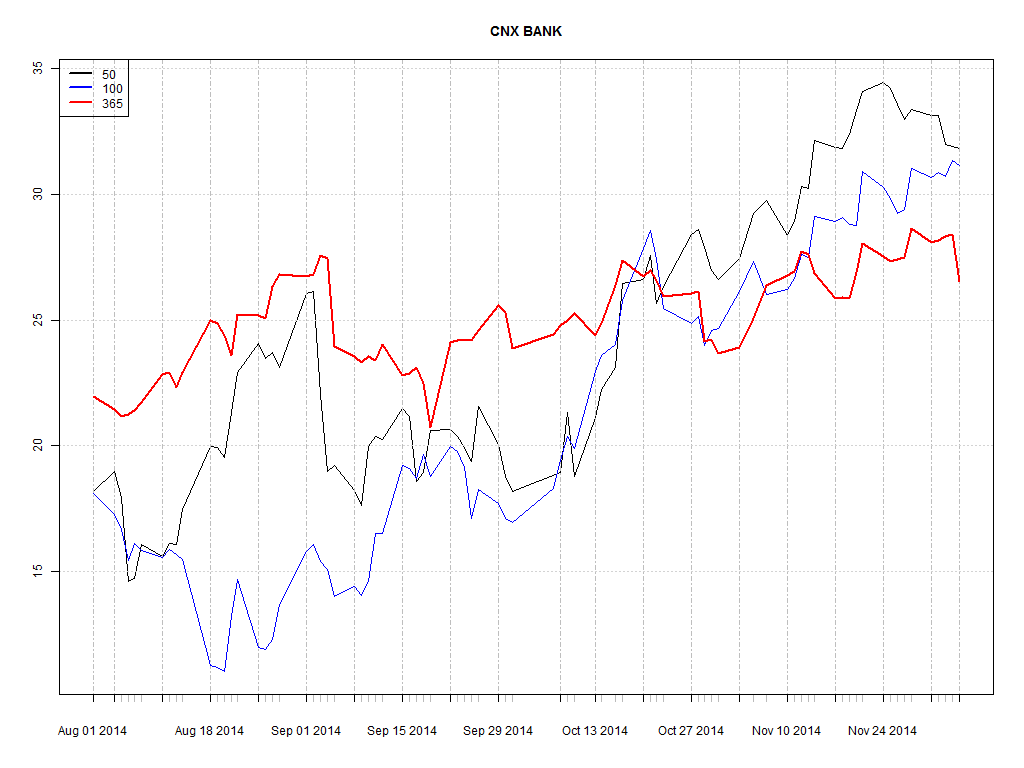

Banks withstood the onslaught well…

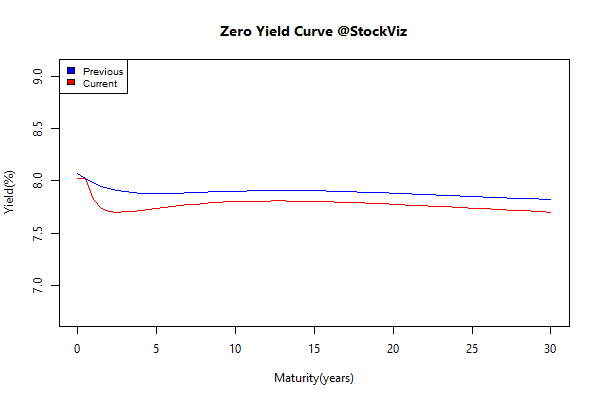

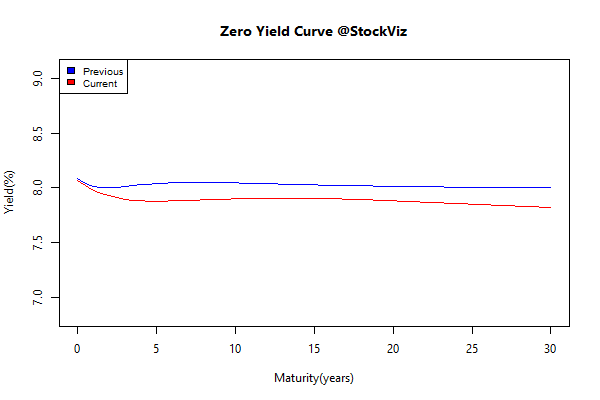

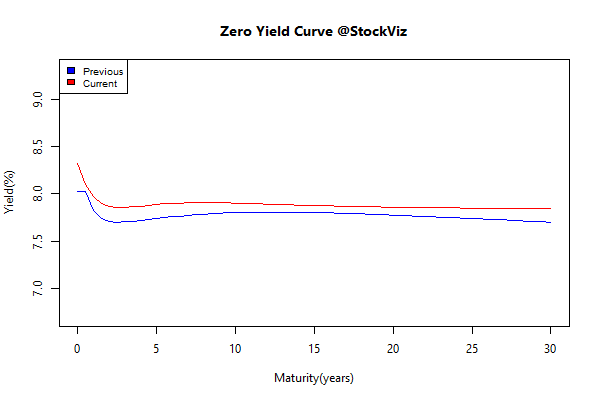

Yield Curve

Bond Indices

| Sub Index | Change in YTM | Total Return(%) |

|---|---|---|

| GSEC TB | +0.44 | +0.04% |

| GSEC SUB 1-3 | +0.43 | -0.43% |

| GSEC SUB 3-8 | +0.19 | -0.53% |

| GSEC SUB 8 | +0.08 | -0.34% |

Yields went up – breaking a long streak of falling rates.

Investment Theme Performance

| Auto | +1.48% |

| Market Fliers | +0.53% |

| Quality to Price | +0.49% |

| Refract: PPFAS Long Term Value Fund | +0.48% |

| Enterprise Yield | +0.18% |

| Momentum 200 | +0.09% |

| Momentum Long-Short | +0.00% |

| The Other Value | -0.03% |

| Financial Strength Value | -0.05% |

| Old Economy Value | -0.18% |

| Magic Formula Investing | -0.27% |

| Balance-sheet Strength | -0.32% |

| Piotroski ROC Small Caps | -0.72% |

| Industrial Value | -0.89% |

| Growth with Moat | -1.04% |

| Efficient Growth | -2.02% |

| CNX 100 50-Day Tactical | -2.28% |

| Market Elephants | -2.30% |

| IT 3rd Benchers | -2.31% |

| ADAG Mania | -5.78% |

Time to average in?

Thought for the weekend

Asset managers and asset owners have a relationship beset with natural conflicts.

- Asset owners want fees below 10 bps; asset managers prefer “2% + 20%.”

- Asset owners want transparency; asset managers favor black-box opacity.

- Asset owners want simplicity; asset managers hire rocket scientists to create complex optimized solutions for sex appeal.

- Asset owners want “future” outperformance after they fund a manager; asset managers would be satisfied with strong past outperformance to facilitate future asset gathering.

- Asset owners want a bigger alpha; asset managers would happily sell them the possibility of alpha and charge handsomely for the service of selling hope.

Source: The Promise of Smart Beta