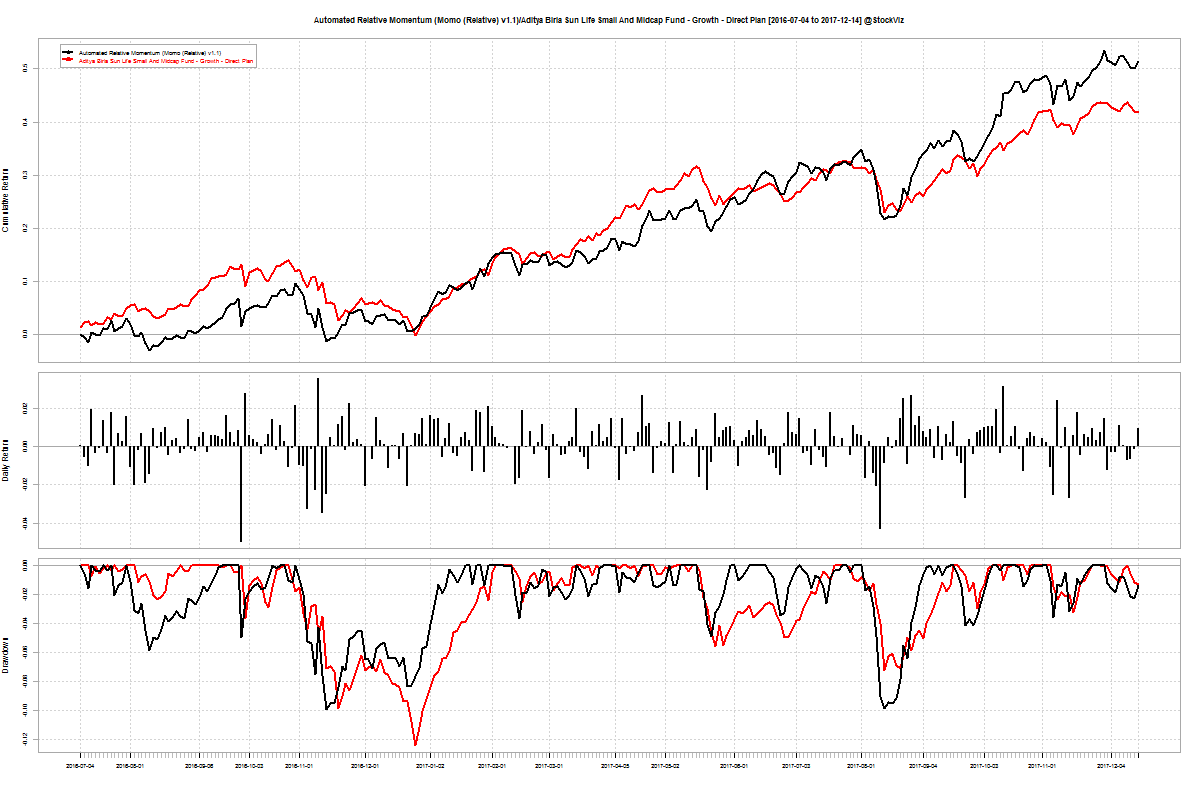

Traditional equity momentum strategies are variations of algos that try to figure out “trending” stocks so that they can be ranked to create a long/short portfolio. The key thing to remember is that these algos are following a trend, the prediction that a trending stock will continue to trend is implicit. However, using machine learning techniques, stocks can be ranked based on their predicted returns over a future time frame.

The simplest momentum strategy looks only at a price series. However, it quickly runs into problems when additional factors are overlaid on top of basic momentum. For example, you may want to filter out volatile stocks out the basket. You can do this either by setting a maximum volatility level or by weighing both momentum and volatility to arrive at a combined rank. Either approach leads to ad hoc decisions of cut off levels and the ratio with which to weigh each of those factors. Luckily, typical machine learning algorithms can work with multiple factors and weigh them based on the training set you supply.

The biggest drawback of using machine learning is that the larger the number of factors/features you use, the less explainable the resulting model becomes. As a trader, if you want to use any of these models, you should have a fairly good idea of what is going in, how the model is setup and what exactly is the model getting trained with.

As a first step in taking a crack at this, we have setup four machine learning algos. Two of them use SVRs and the other two use LR to train on data that is either return-series only or a combination of returns and volatility. You can have look at them here.

We will have more of these machine learning models out as we ramp up our understanding of these models. Stay tuned!