Equities

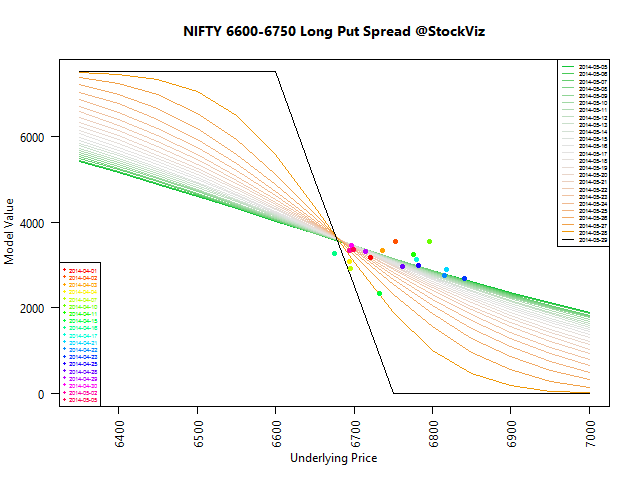

The Nifty put in a MODIfied return of +5.02% (+7.15% in USD terms) this week…

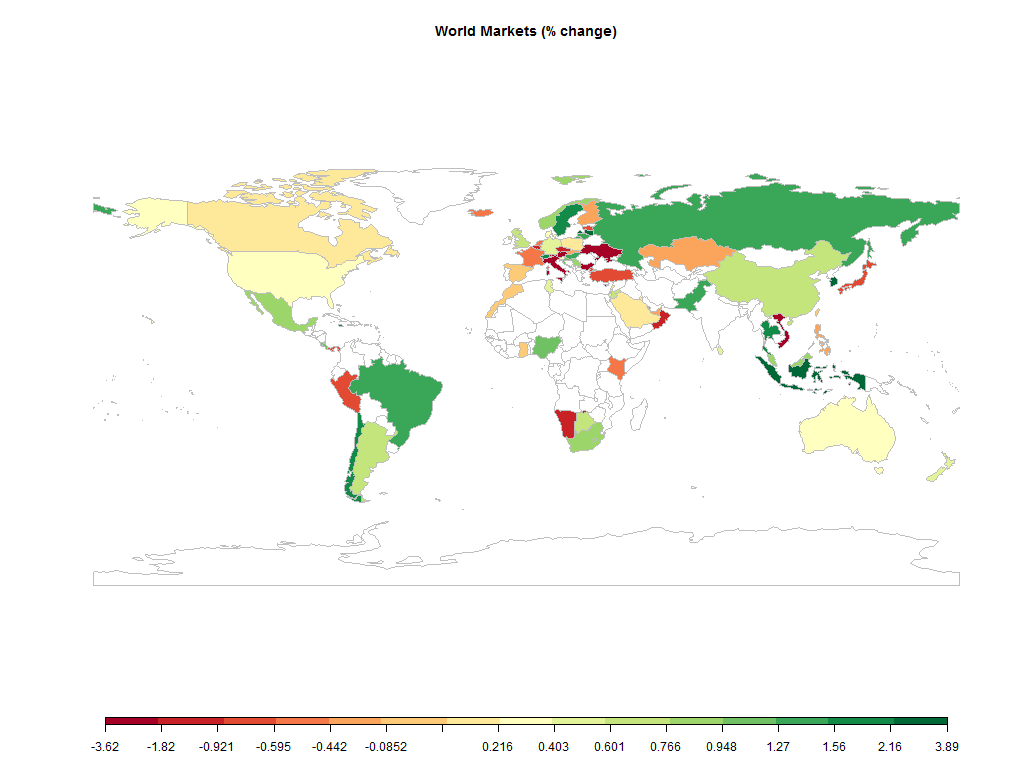

| MINTs | |

|---|---|

| JCI(IDN) | +2.72% |

| INMEX(MEX) | +0.84% |

| NGSEINDX(NGA) | +1.21% |

| XU030(TUR) | -0.76% |

| BRICS | |

|---|---|

| IBOV(BRA) | +1.31% |

| SHCOMP(CHN) | +0.76% |

| NIFTY(IND) | +5.02% |

| INDEXCF(RUS) | +1.52% |

| TOP40(ZAF) | +0.77% |

Commodities

| Energy | |

|---|---|

| Brent Crude Oil | +1.86% |

| Ethanol | +3.47% |

| Heating Oil | +1.60% |

| Natural Gas | -2.41% |

| RBOB Gasoline | +2.85% |

| WTI Crude Oil | +2.45% |

| Metals | |

|---|---|

| Copper | +1.94% |

| Gold 100oz | +0.47% |

| Palladium | +1.89% |

| Platinum | +2.51% |

| Silver 5000oz | +1.05% |

Currencies

| MINTs | |

|---|---|

| USDIDR(IDN) | -1.03% |

| USDMXN(MEX) | -0.50% |

| USDNGN(NGA) | +0.71% |

| USDTRY(TUR) | +1.06% |

| BRICS | |

|---|---|

| USDBRL(BRA) | -0.23% |

| USDCNY(CHN) | +0.09% |

| USDINR(IND) | -2.07% |

| USDRUB(RUS) | -1.34% |

| USDZAR(ZAF) | -0.16% |

| Agricultural | |

|---|---|

| Cattle | -0.35% |

| Cocoa | +2.99% |

| Coffee (Arabica) | -0.19% |

| Coffee (Robusta) | -0.81% |

| Corn | -4.16% |

| Cotton | -2.24% |

| Feeder Cattle | +1.52% |

| Lean Hogs | +4.06% |

| Lumber | -3.78% |

| Orange Juice | -2.81% |

| Soybean Meal | -3.32% |

| Soybeans | -2.50% |

| Sugar #11 | +4.08% |

| Wheat | -5.79% |

| White Sugar | +4.18% |

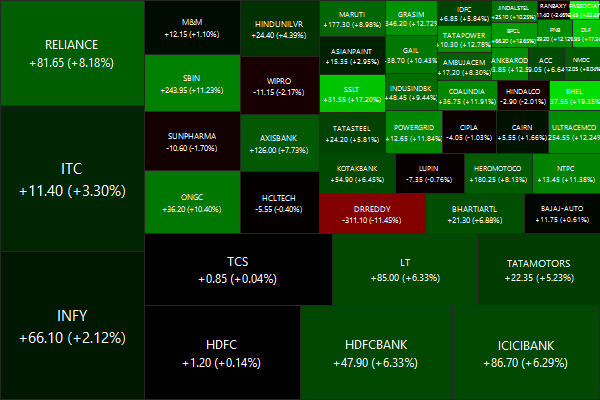

Nifty Heatmap

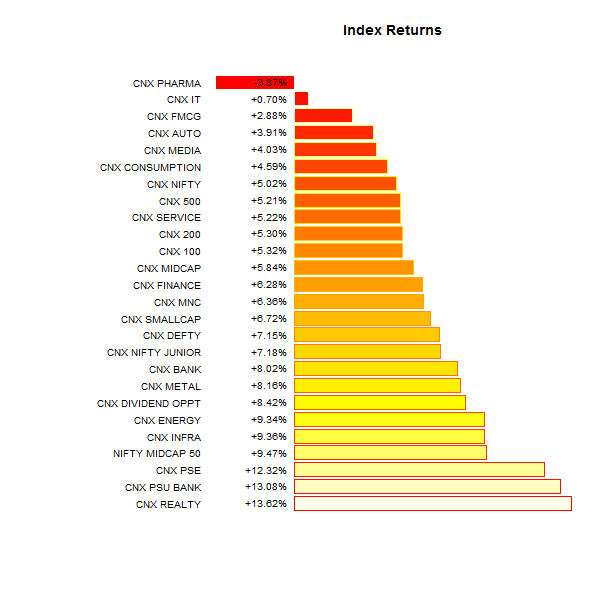

Index returns

Top winners and losers

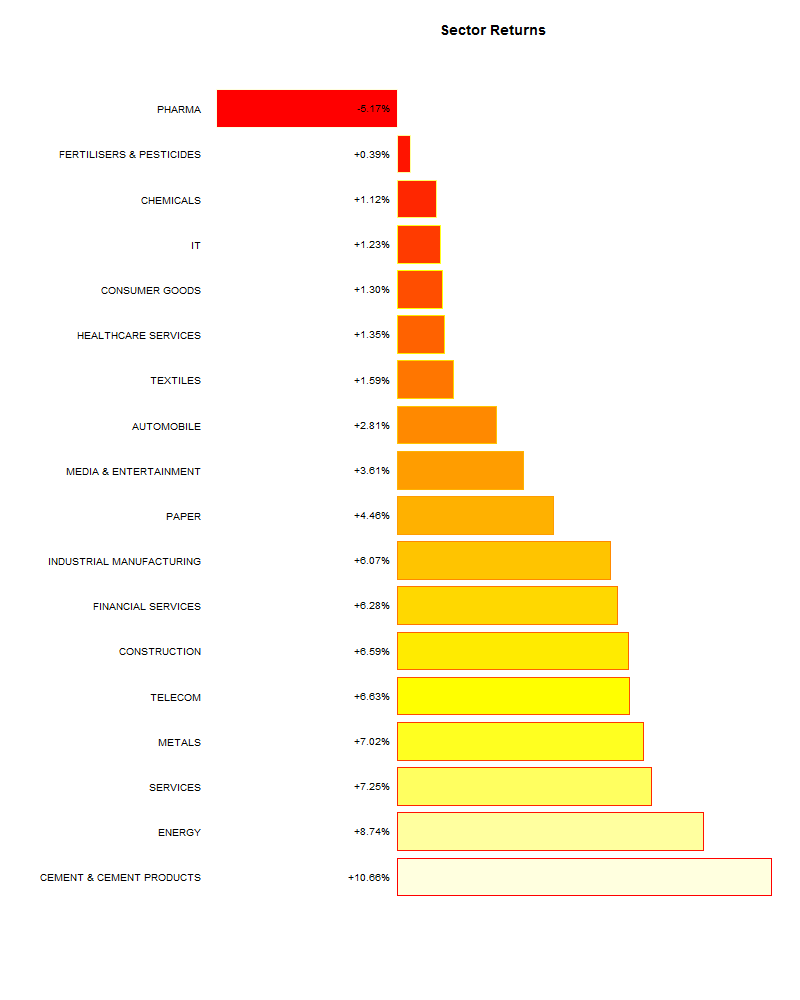

Banks in, Pharma out…

ETFs

| PSUBNKBEES | +9.50% |

| BANKBEES | +7.53% |

| JUNIORBEES | +6.61% |

| INFRABEES | +4.97% |

| NIFTYBEES | +4.48% |

| GOLDBEES | -2.25% |

We were definitely risk ON this week…

Investment Theme Performance

| Market Fliers | +17.28% |

| Enterprise Yield | +5.25% |

| Long Term Equity* | +2.91% |

| Quality to Price | +2.09% |

| Consistent10* | +1.84% |

| Magic Formula Investing | +1.75% |

| Growth with Moat | +1.48% |

| Momentum 200 | +1.25% |

| Financial Strength Value | +1.17% |

| Efficient Growth | +1.08% |

| Balance-sheet Strength | +0.66% |

| IT 3rd Benchers | +0.35% |

| Market Elephants | -0.29% |

High beta trumped every other strategy…

Sector Performance

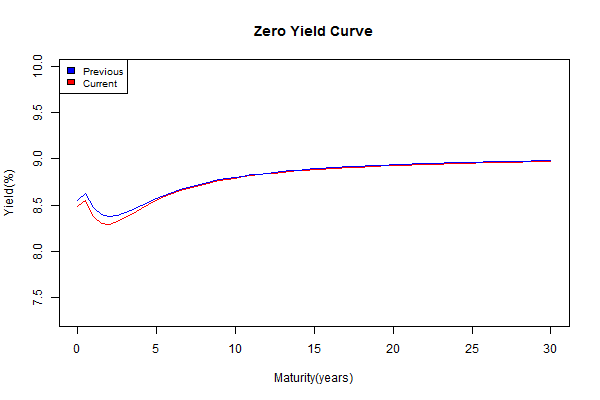

Yield Curve

Thought for the weekend

You are on a footbridge watching a trolley speeding down a track that will kill five unsuspecting people. You can push a fat man over the bridge onto the tracks to save the five. (You cannot stop the trolley by jumping yourself, only the fat man is heavy enough.) Would you do it?

If you thought the language in which a dilemma is posed should make no difference to how it is answered, think again!

Source: Gained in translation