The Research

In their paper, Intraday Momentum: The First Half-Hour Return Predicts the Last Half-Hour Return (pdf,) the authors assert that the first half-hour return on the market predicts the last half-hour return on the market.

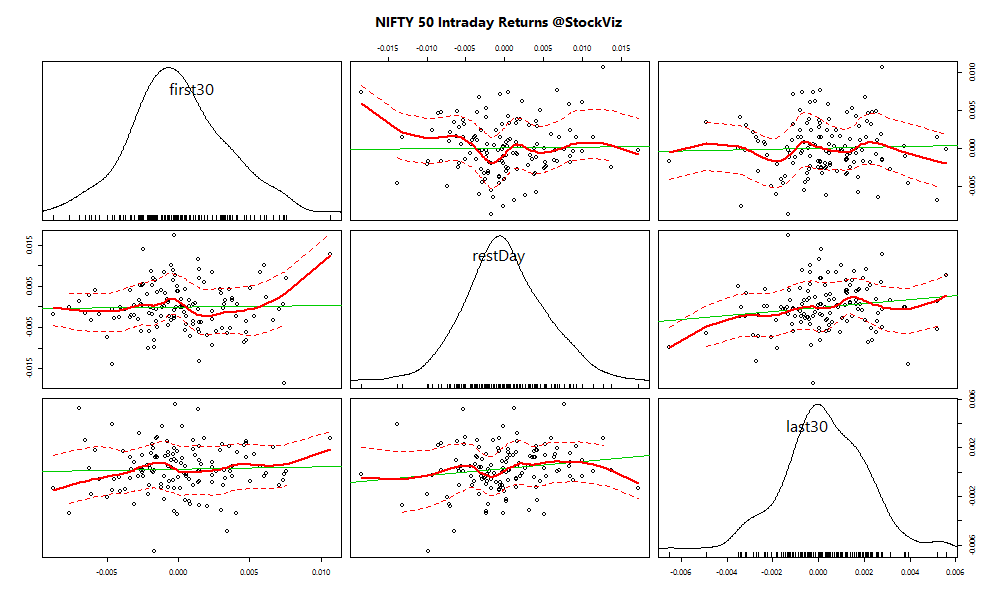

Our take

It seems to apply only to the selection of ETFs contained in their research. We ran a sniff-test on our very own NIFTY 50 index. If there was any correlation between the first half-hour and the last half-hour, it should have shown up in the top-right plot:

We admit that our sample size is small. We will continue to accumulate data and run this script a year from now to see if any relationship emerges from the data. Stay tuned!