Last Decemeber, we had presented a back-test of a factor rotation strategy that would go long the factor portfolio that performed best over a look back period. The Themes based on this backtest have finally completed 90 days in the market. Here’s a quick update on their performance.

Indian Factor Momentum

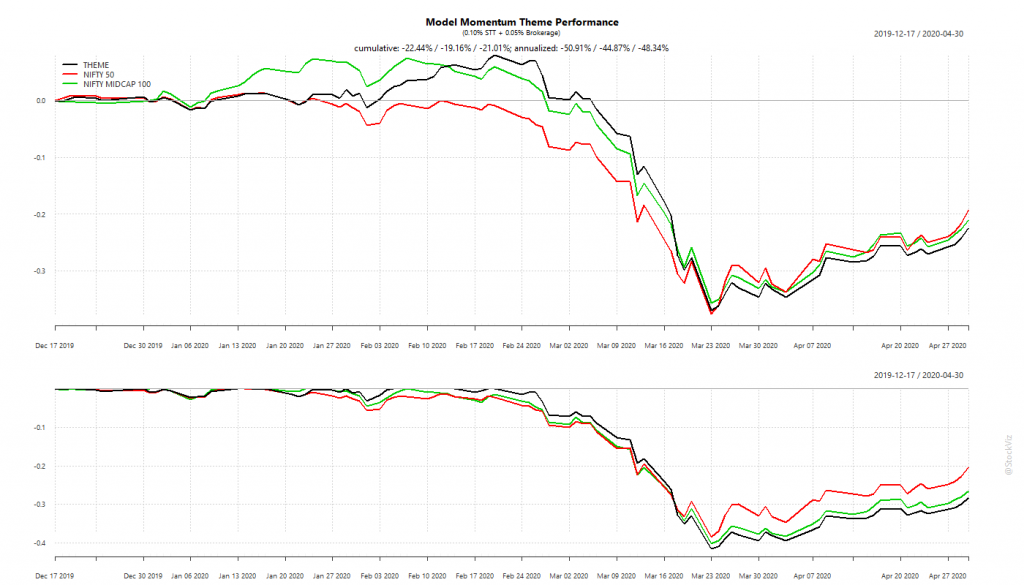

We went with two flavors here. One that went long a portfolio of stocks in NSE’s strategy indices – Factor Momentum (Indices) – and another that went long one of our factor portfolios – Factor Momentum (Themes).

Factor Momentum (Indices)

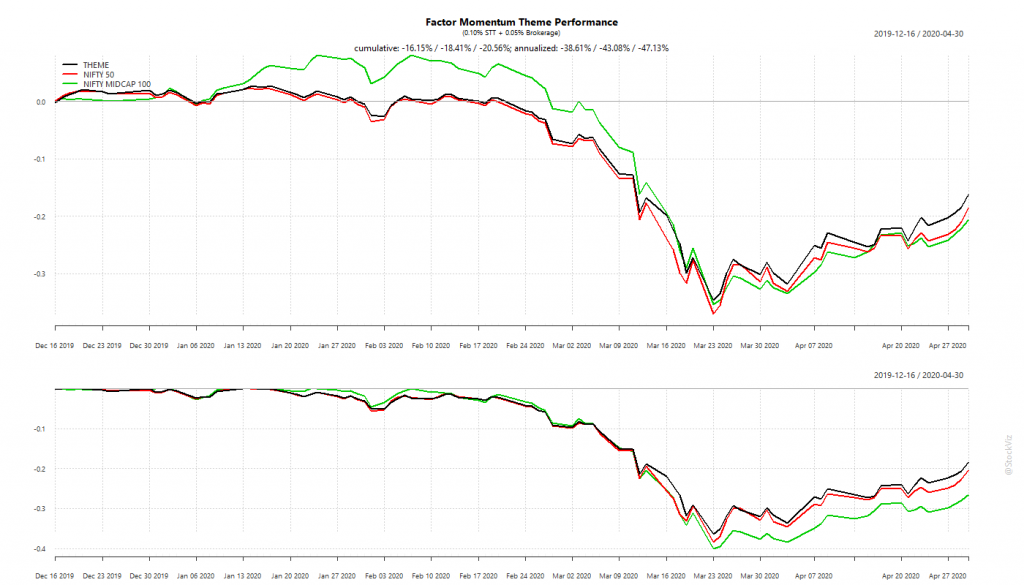

Factor Momentum (Themes)

Thoughts on Performance

Both portfolios crashed as much as the large and midcap indices during the Corona Virus Panic. However, it appears that the recovery from the crash has been lead the Index variant. For a while, it did look like the Theme variant out-performed the indices but it may have been because of the randomness introduced by the smaller number of stocks in the portfolio.

US Factor Momentum

The US context is wildly different from India. With brokerage costs at zero and with the ability to trade fractional shares, the portfolio can be efficiently rebalanced with a one-month look-back (Factor Momentum III.) Given the steepness of the fall during the Corona Virus Panic, the shorter lookback helped it quickly adjust to the market and keep drawdowns to less than 10% compared to SPY’s 30%+

WhatsApp us at +91-80-26650232 if you are interested in knowing more about these strategies.